The draft Law on Personal Income Tax (amended) has been submitted by the Government to the National Assembly. Based on the review opinions of the National Assembly's Economic and Financial Committee and the discussion opinions of National Assembly deputies, the Ministry of Finance plans to report to the Government a plan to complete the draft law with some adjusted contents, especially the tax schedule.

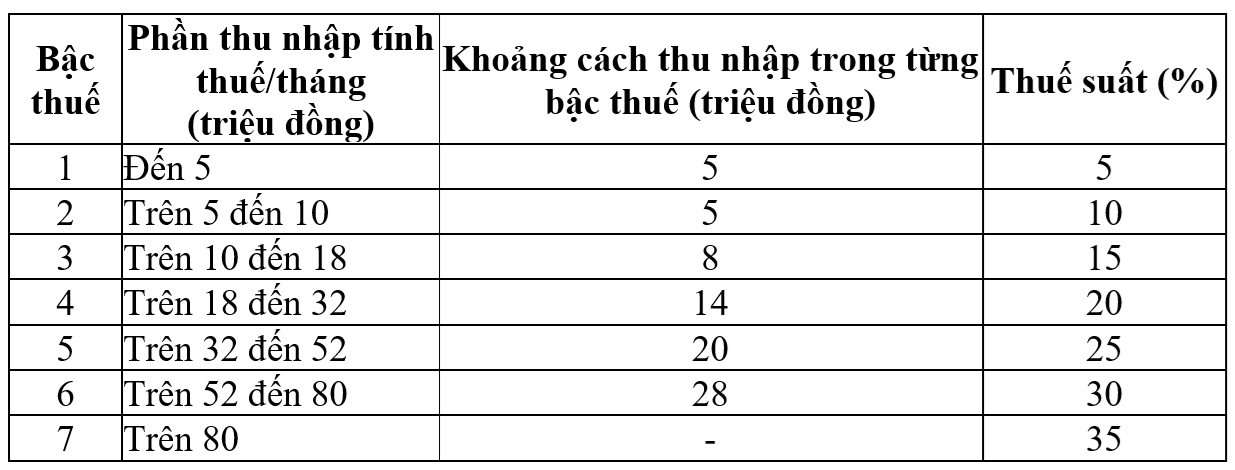

The progressive tax schedule applies to resident individuals with income from salaries and wages according to current regulations as follows:

Current tax schedule. Screenshot

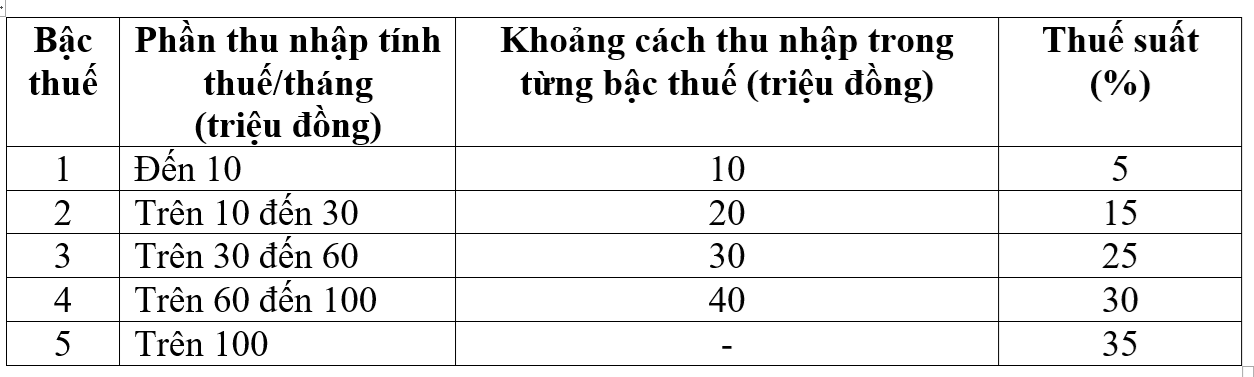

The Government has proposed and reported to the National Assembly in the draft Law on adjusting the progressive tax schedule applicable to resident individuals with income from salaries and wages in the direction of reducing the number of tax rates from 7 to 5 and widening the gap between the rates as follows:

The Government's proposed tax schedule. Screenshot

Based on the opinions of National Assembly deputies, the drafting agency plans to report to the Government to accept and complete the progressive tax schedule in the direction of being able to study and consider the option of adjusting the tax rates from 15% and 25% to 10% and 20% to equalize the tax rates of the schedule.

According to the Ministry of Finance, with this new tax schedule, all individuals currently paying taxes at all levels will have their tax obligations reduced compared to the current tax schedule. In addition, the new tax schedule also overcomes the sudden increase at some levels (level 2, level 3) as proposed in the previous draft law, ensuring more reasonableness.

In addition, the draft law adds a number of provisions on tax exemption and reduction of personal income tax. Specifically, amending and perfecting the provisions on a number of tax-exempt incomes, such as: income supplemented by pension insurance funds, voluntary pension funds, wages for night work, overtime, wages paid for days not taken off, severance pay, unemployment benefits paid by enterprises, interest on local government bonds...

At the same time, supplement the regulation that taxpayers are allowed to deduct certain expenses during the year at an appropriate level such as medical and educational expenses before calculating taxes and assign the Government to provide detailed regulations to ensure flexibility and suitability with the socio-economic situation.

Regarding the adjustment of family deductions, on October 17, the National Assembly Standing Committee passed a Resolution on adjusting the family deductions of personal income tax. Accordingly, the deduction for the taxpayer himself/herself was increased to 15.5 million VND/month, and for each dependent to 6.2 million VND/month.

With this new family deduction, individuals do not have to pay tax with an income of 17 million VND/month (if no dependents) or 24 million VND/month (if 1 dependent) or 31 million VND/month (if 2 dependents).

Personal income tax revenue has been increasing continuously for more than a decade, with only one year of decline. Data from the Ministry of Finance shows that in the period 2011-2024, personal income tax revenue has been higher year after year (except for 2023). Notably, tax revenue in 2024 is nearly 5 times higher than in 2011.

Source: https://vietnamnet.vn/de-xuat-giam-manh-thue-suat-thu-nhap-ca-nhan-tat-ca-nguoi-nop-thue-deu-duoc-loi-2466326.html

Comment (0)