For about a month and a half now, the trend of increasing deposit interest rates has been taking place at a series of commercial banks. According to economic experts, deposit interest rates have increased but lending interest rates will have to remain stable to support business and economic growth.

Interest rates on many terms increased simultaneously.

On November 13, Cake by VPBank (Cake) announced that it is implementing a preferential interest rate program. Customers who deposit savings will not only receive additional interest but also have the chance to win an iPhone and receive lucky money directly into their account. Those who open a savings account for the first time with a term of 6 months or more will immediately receive an additional interest rate of 0.6%. For existing customers, when opening a new deposit, they will receive an additional interest rate of 0.2 - 0.6%.

According to the latest interest rate schedule, Cake applies 6.3%/year when customers deposit savings for 6 months or more. The highest interest rate at this bank is 6.5%/year for terms of 12 months or more.

A report by MBS Securities Company shows that in October 2025, 6 commercial banks increased their deposit interest rates. In November, a series of banks continued to join the wave of increasing deposit interest rates. Of which, the 2 latest banks to adjust deposit interest rates are LPBank and Kienlongbank. The banks adjusted their interest rates to increase by 0.1 - 0.3 percentage points compared to before.

Not only increasing the interest rate of savings deposits at the counter and online, some banks also promote capital mobilization through the deposit certificate channel with higher interest rates than the normal savings channel. In particular, Ban Viet Bank (BVBank) is issuing online deposit certificates with high interest rates and flexible terms from 6 to 15 months. The final interest rate for a 6-month term is 5.8%/year, the highest is up to 6.3%/year when customers buy a 15-month deposit certificate.

Asia Commercial Bank (ACB) also issued deposit certificates from the end of October 2025, with a fixed interest rate of up to 6%/year, calculated based on the actual holding period. Customers who buy certificates can sell them before maturity if needed and still enjoy the corresponding yield. According to ACB General Director Tu Tien Phat, the purpose of issuing deposit certificates is to diversify investment solutions for customers.

The increase in deposit interest rates for many terms at the end of the year has made many people worry that lending interest rates will increase accordingly, especially for corporate customers who need to borrow capital for production and business, to meet consumption and export needs at the end of the year.

Talking to a reporter from the Lao Dong Newspaper, Dr. Can Van Luc, an economic expert, said that the move to increase deposit interest rates by commercial banks is completely normal and cyclical. At the end of the year, businesses' capital needs increase, so banks also increase their input mobilization. When banks want to attract more deposits, they will increase interest rates.

From another perspective, Associate Professor Dr. Pham The Anh, National Economics University, assessed that the current interest rate hike of domestic banks is consistent with the context of high global interest rates and upward pressure on exchange rates. The current increase in deposit interest rates is still good for the economy, thereby helping to stabilize the macro economy, avoiding capital flows into speculative asset sectors, and also helping to stabilize exchange rates. However, it is necessary to control the increase in deposit interest rates so that they are not too high.

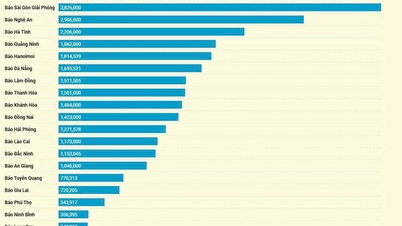

Latest interest rate table at some commercial banks. Photo: DUY PHU - THAI PHUONG

No worries about loan interest rates increasing

According to Mr. Vu Minh Truong, Director of Capital Resources and Financial Markets of VPBank, the rate of increase in mobilization interest rates is lower than the credit growth rate of the banking system. In the first 9 months of 2025, capital mobilization growth was about 16%, while credit growth was up to 19%. Capital demand for the end of the year will continue to increase, so increasing mobilization interest rates is understandable.

Mr. Nguyen Hung, General Director of Tien Phong Bank (TPBank), also explained similarly when he said that the end of the year is usually the sprint period, the capital demand of the economy increases sharply. This requires banks to supplement mobilized capital to meet credit growth targets. The mobilization interest rate level tends to increase but the increase is still very slight. At TPBank, deposit interest rates only increased by about 0.1 percentage points.

"Input interest rates are increasing, but lending interest rates must remain stable according to the requirements of the Government and the State Bank to support businesses and the economy. Therefore, banks will have to calculate how to diversify revenue from service fees, in addition to pure interest from credit. Net profit margins of banks will also have to be narrower than before," Mr. Hung commented.

Dr. Can Van Luc believes that from now until the end of the year, lending interest rates are unlikely to increase further because the Prime Minister and the State Bank have asked credit institutions to keep output interest rates stable. If the mobilization interest rate continues to increase, banks' profit margins may be slightly narrowed.

Looking at the broader international context, Associate Professor Dr. Pham The Anh analyzed that with global interest rates still at high levels, especially government bond interest rates and interbank interest rates in the US, the ability to maintain low interest rates in Vietnam is not easy. Although the average inflation in the first 9 months of 2025 was only 3.27%, the actual cost of living is on an upward trend, especially in the group of essential goods and services, putting pressure on people's lives, especially low-income people.

"High exchange rates have a negative impact on inflation. Housing prices in Vietnam are also increasing, so maintaining low interest rates is not appropriate. In this context, monetary policy management needs to have a long-term vision, meaning that credit growth should not be promoted too quickly to avoid potential risks for the economy in the future," Associate Professor, Dr. Pham The Anh analyzed.

Previously, at the regular Government meeting in September 2025, Deputy Governor of the State Bank Doan Thai Son said that in order to achieve the credit target set for 2025 of about 16% and contribute to supporting the economy, the State Bank will continue to implement synchronous solutions. Credit institutions are required to increase credit growth safely and effectively; focus on priority production and business sectors and economic growth drivers; and strictly control credit in potentially risky sectors.

The Prime Minister has just requested the State Bank to submit to the Government a decree guiding the policy of supporting 2% interest rate for businesses borrowing capital to implement green, circular projects, applying the environmental, social, and governance (ESG) standards framework through commercial banks in November 2025.

This is the content of the announcement of the conclusion of the Prime Minister, Head of the National Steering Committee for the implementation of Resolution 68/2025 of the Politburo on private economic development, at the second meeting of the steering committee.

Source: https://nld.com.vn/giu-on-dinh-lai-suat-cho-vay-196251113214249132.htm

![[Photo] Deep sea sand deposits, ancient wooden ship An Bang faces the risk of being buried again](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/13/1763033175715_ndo_br_thuyen-1-jpg.webp)

![[Photo] Unique art of painting Tuong masks](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/14/1763094089301_ndo_br_1-jpg.webp)

![[Photo] Special class in Tra Linh](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/14/1763078485441_ndo_br_lop-hoc-7-jpg.webp)

![Dong Nai OCOP transition: [Article 3] Linking tourism with OCOP product consumption](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/11/10/1762739199309_1324-2740-7_n-162543_981.jpeg)

Comment (0)