Export turnover is forecast to continue to increase in 2017, with Japan and the US being the key markets. With positive developments in the first 9 months of the year, we forecast that plastic product exports will continue to maintain their growth momentum next year. Meanwhile, the European market is likely to make it difficult for domestic enterprises. The unfavorable development of the EUR will cause losses in the number of orders and domestic enterprises will also face competition from goods produced in this region due to the decrease in raw material costs.

Export turnover is forecast to continue to increase in 2017, with Japan and the US as key markets . With positive developments in the first 9 months of the year, we forecast that plastic product exports will continue to maintain their growth momentum next year. Meanwhile, the European market is likely to make it difficult for domestic enterprises. The unfavorable developments of the EUR will cause losses in the number of orders and domestic enterprises will also face competition from goods produced in this region due to the reduction in raw material costs when the EUR is low. Japan and the US are still very potential markets for the plastic export industry with large consumption demand.

Plastic packaging: growth potential depends on end-product industries such as food and beverage . As analyzed above, the plastic packaging industry, especially flexible packaging and food PET packaging, are supporting industries for the consumer goods industry, including packaged food, canned and bottled drinks. We assess that the food industry will have many opportunities for development in the future. The improving economic situation will increase the middle class and the urbanization rate, according to estimates, the middle class in Vietnam is expected to double in the next 5 years. This is a positive factor for the development of the food industry, especially packaged food. According to BMI Research, the food industry is forecast to grow strongly, specifically food sales increased by 10.2% in 2016 and the compound annual growth for the period 2015 - 2020 is 10.9%. With about 6.1 million households out of poverty in the period 2015 - 2050 and in the group with income of 5,000 - 10,000 USD/year, consumer demand will shift to high-value food products. For the beverage industry, according to the Vietnam Alcohol - Beer - Beverage Association, one of the products contributing greatly to the growth of the Vietnamese beverage market is bottled green tea, herbal tea, and energy drinks, which are forecast to have CAGRs of 17.8%, 27.6% and 24.7% in the period 2015 - 2019, respectively. Domestic enterprises are also stepping up investment in infrastructure and product innovation with a total investment of about 6,000 billion VND, led by Tan Hiep Phat Group with two large projects of Number One factories in Ha Nam and Chu Lai, followed by Masan Group and Hoa Binh Group. Thus, it can be seen that the prospects of the bottled food and beverage industry are very positive in the future, creating a premise for the development of the plastic packaging industry. Although according to the Plan for the development of the plastic industry until 2020, the proportion of plastic packaging will decrease, but we believe that, with the current growth of the food industry, the plastic packaging sector still has a lot of room for development.

Household plastics – great potential but facing competitive pressure from foreign competitors . The outlook for the household plastics industry remains positive due to (1) population growth leading to a large demand for household goods (the working-age population accounts for 50%), (2) per capita income increases, about 6.1 million households will be out of poverty in the period 2015 – 2050 and will be in the group with income of 5,000 – 10,000 USD/year (according to BMI Research), (3) the rate of consumers using Vietnamese products is increasing, according to statistics, in the supermarket system of Vietnam, 85 – 95% are Vietnamese brands. However, low technology leads to uneven product quality as well as limited financial potential, household plastics businesses are currently facing competitive pressure from foreign competitors, typically the household plastic brand Lock&Lock. High-end products of foreign enterprises with good quality will have better profit margins than average quality Vietnamese products. Therefore, the current problem of domestic plastic enterprises is to improve product quality by improving production technology, in addition, advertising capacity as well as services must be improved, only then can domestic products compete well with foreign products.

Construction plastics - Real estate and construction are warming up, greatly supporting the growth of the industry . The market share of the construction plastics segment only accounts for 18.2% of the total plastics industry but is growing quite rapidly, up to 15 - 20%/year. Currently, the whole country has 180 enterprises operating in 2 segments: construction plastic pipes and construction plastic materials. According to the classification system of the Ho Chi Minh City Stock Exchange, the construction plastics industry belongs to the materials industry with the industry group index increasing by 45% in the first 9 months of the year, partly proving that this is an industry that investors are very interested in. The international research organization BMI forecasts that in 2016, the growth of Vietnam's infrastructure construction industry will be 9.85%, the average real growth rate is about 6%/year in the period 2016 - 2024. The demand for construction plastic pipes and profile bars is increasing. According to the national housing development strategy to 2020, with a vision to 2030 approved by the Prime Minister in 2011, it has provided synchronous solutions to overcome difficulties and develop the real estate market. The target by 2020 is that the average national housing area will reach about 25 m2 of floor/person, of which in urban areas it will reach 29 m2 of floor/person and in rural areas it will reach 22 m2 of floor/person, striving to achieve the target of minimum housing area of 8 m2 of floor/person. By 2030, strive to achieve the target of average national housing area of about 30 m2 of floor/person, minimum housing area of 12 m2 of floor/person. The development of the construction and real estate market will create momentum for the construction plastics industry to grow in the future.

Recycled plastic - a new trend in the future. Recycled plastic products are currently popular in developed countries due to environmental pollution caused by plastic waste released into the environment and causing many serious problems due to their long-term persistence and difficulty in decomposing. The Vietnam Plastics Association believes that if recycled plastic materials can be used at a rate of 35-50% per year, businesses can reduce production costs by more than 15%. Meanwhile, according to the Ho Chi Minh City Waste Recycling Fund, plastic waste accounts for a high proportion, second only to food waste in urban solid waste. However, the total amount of plastic scrap purchased is only about 10% of the total plastic waste remaining each year, which is released into the environment. Recyclable plastic products are currently mainly products of the plastic packaging sub-sector such as PET plastic bottles and food packaging. The prospect of recycled plastic products is very large, especially food packaging and PET plastic bottles. The demand for plastic recycling is increasing partly due to the incentive policies of governments in the process of reducing environmental pollution caused by plastic products. However, although there are many prospects in the future, in the actual development process, it still faces many problems. Firstly, because the origin of recycled plastic is widespread, the quality is different, the difference in performance is also large, leading to poor quality and stability of recycled plastic. Secondly, this product has a relatively high cost, in which the price is 30-50% higher than the price of virgin plastic. Thirdly, the recycled plastic industry requires relatively high technology, while the majority of businesses operating in this field are small and scattered. However, although it still faces many problems, this is still the development of the future and if Vietnamese businesses take advantage of their advantages, the potential for development is very large in the context of the shortage of supply for this item.

Plastic pellet prices are forecasted to increase slightly in the last months of the year, but will maintain a sideways trend . Regarding the trend of plastic pellet prices in the coming time, we have the following comments:

- Oil prices in 2017 are expected to remain flat in the range of 50-55 USD. In the context that member countries of the Organization of the Petroleum Exporting Countries (OPEC) have agreed to cut production for the first time in 8 years, oil prices have recently recovered strongly to over 50 USD/barrel. The production cut will take effect in early 2017, according to which OPEC countries will reduce production by 1.2 million barrels per day from the current official level of 33.6 million barrels/day. However, this could also be a double-edged sword for the market when the possibility of shale oil producers in the US will increase production. Meanwhile, China's demand for crude oil imports increased sharply in the last months of the year, but perhaps the sharp increase in imports was due to the decrease in crude oil prices rather than an increase in actual consumption demand. Therefore, if crude oil supply decreases in line with the decrease in import demand from key importing countries such as China, the efforts of producers will not be very effective.

- US market: PPIJPRAM Index, the US market reference index of raw materials and plastic resins, started to increase slightly in September and October.

PE

PE supplies have tightened recently as a result of scheduled plant maintenance and unexpected power outages in the region. Companies experiencing problems with PE or feedstock ethylene production in the Gulf Coast include LyondellBasell Industries, ExxonMobil Chemical Co and Westlake Chemical Corp, all major players in the North American plastics industry. Lower PE inventories have also played a role in the recent price increase. The increase in PE demand in the U.S. and Canada is a combination of factors, according to the American Chemistry Council in Washington, with regional high-density PE sales up more than 4%, while low-density PE sales rose more than 1% and LDPE fell nearly 1%. Domestic HDPE sales also rose nearly 2%, driven by a nearly 15% increase in eight-month export sales. For LLDPE, sales fell more than 2%, driven by a nearly 2% decline in export markets. LDPE in the region lost 2% due to a nearly 10% drop in export revenue.

PP

PP prices in the US market continued to increase, mainly due to the previous tight supply of PP resin, but allowing more raw materials to be imported from all over the world into the market, causing prices to fall. Currently, although imported raw materials into the region are still available, they have decreased, allowing PP prices to increase again. PP resin sales also increased by 1.3% in the first 8 months of 2016, with the above growth rate contributed by the boom in export sales with 31%.

PVC

PVC prices continue to maintain a stable trend and are forecast to remain flat. PVC sales continue to maintain a good level in the market, partly due to the recovery of the US housing market as demand for hard materials in the plumbing and pipe industry increased by 7.5%. In the Asian market, PVC prices are likely to be stable and even stronger in the first half of 2017 due to supply constraints from China following inspections of PVC production from carbide (an important raw material for the chemical industry, especially PVC manufacturing).

Other markets: PE and PP resin prices in Turkey in November increased compared to previous months due to pressure from lower profits than other markets. The price increase ranged from 10-40 USD/ton. Supply decreased due to many factories closing in Saudi Arabia, Oman, India and Egypt. Another reason contributing to this price increase was that the Chinese market recovered and pushed up prices. At the same time, the increase in import tax on PP resin to 3% in 2017 also affected the price trend, suppliers will increase PP resin prices corresponding to the adjusted tax rate.

With the above comments, we believe that plastic resin prices will increase in the last months of the year along with the upward trend of oil prices and will likely remain flat in 2017 or increase slightly . Plastic prices will fluctuate according to world oil prices, however, most Vietnamese plastic enterprises have stockpiled enough raw materials to produce for 2 to 6 months, especially during peak seasons. Therefore, there will be a certain delay and enterprises must be flexible to avoid being strongly affected by fluctuations in raw material costs.

Tax policies affect Vietnamese plastic enterprises . The Government has just issued Decree 122/2016/ND-CP on Export Tariff, Preferential Import Tariff, List of goods and absolute tax rates, mixed tax, import tax outside tariff quota, effective from September 1, 2016. It provides detailed regulations on import tax rates for PP raw materials (HS 3902) as follows:

- From September 1st to December 31st, 2016: PP import tax is 1%

- From 01/01/2017: PP import tax is 3%

Currently, the domestic supply capacity of PP plastic materials can only meet 100,000 - 150,000 tons/year for plastic manufacturing enterprises, while the demand for use is up to 1.2 million tons/year, not to mention the growth demand for this material determined by the Vietnam Plastics Association to increase by an average of 15%/year.

According to the Ministry of Finance's calculations, with the current preferential import tax rate of 1%, although still higher than the 0% rate of some FTAs, to apply the 0% tax rate, enterprises also need to incur additional costs of nearly or equal to 1% (such as the cost of issuing C/O), while imported goods require transportation time and often have to be purchased in large quantities, with more capital than domestic purchases. Thus, the purchase and sale of these products by domestic enterprises at the import price + 1% import tax is acceptable. By mid-2017, the Nghi Son oil refinery project is expected to come into operation. According to the investment certificate, this project can produce 380,330 tons of PP resin, 158,775 tons of benzene, and 525,600 tons of p-xylene per year. Considering the reality when Nghi Son project comes into operation, the Ministry of Finance has decided to impose an import tax rate of 3% on PP plastic resins from January 1, 2017.

We believe that increasing the import tax on PP to 3% will create many difficulties in terms of raw material sources for businesses in the industry, especially those producing food packaging and construction packaging. According to VPA's preliminary calculations, with the current import price, if the import tax is increased to 3%, the cost arising from the increase in import prices that domestic businesses have to pay to exporting businesses in the FTA region in 2017 will be 1,870 billion VND. Therefore, in addition to the pressure on plastic resin prices to increase slightly, Vietnamese plastic businesses are also under pressure from the cost of import tax on raw materials. Meanwhile, PP resin manufacturers in countries in the region such as ASEAN, Korea, and China will benefit. Specifically, businesses from ASEAN countries may increase the selling price of PP resin corresponding to the adjusted import tax rate. Accordingly, domestic businesses will be strongly affected by this new pricing policy.

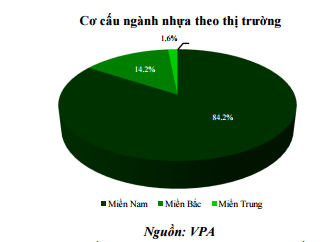

Fierce competition right at home. Currently, there are more than 2,000 enterprises operating in the plastics industry, of which about 84% are concentrated in the South, the North with about 14% of enterprises operating. Therefore, the strongest competition is in the South. Plastic packaging is still the segment with the highest proportion in the plastics industry, with a rate of up to 37.4% in 2015. With four smaller segments, plastic packaging products are very diverse, so competition does not take place directly. However, we note that with the regulation of imposing a 3% import tax on PP plastic resin starting from 2017, enterprises in the construction packaging and food packaging sub-sectors will likely face competitive pressure from foreign competitors as we have analyzed above. It can be seen that while domestic enterprises are still struggling with the problem of input material costs, plastic enterprises from other countries have been bringing finished products to compete right in Vietnam.

Construction plastics with a mainly domestic market are under more intense competitive pressure. The two largest enterprises in the construction plastics industry are Tien Phong Plastics, which dominates the Northern market with a 60% market share and a national market share of about 29%, and Binh Minh Plastics, which leads the Southern market with a market share of nearly 50%. However, recently, the two giants in the plastic industry have begun to expand their market share by penetrating their competitors' playing fields as well as expanding to the Central region, where the plastic pipe market has not yet had a king. The acquisition of Five Star Plastics by NTP and the desire to merge with Da Nang Plastics by BMP have clearly demonstrated this strategy. In addition, enterprises also maintain market share by increasing the discount rate for agents. NTP always maintains a high discount rate of about 11-17%, while BMP maintains it at 11-17% and other policies for agents, typically the Distribution System Conference with 1,400 guests will take place in Malaysia at the end of November. In addition to the two giants in the plastic industry, the remaining market share belongs to other small competitors such as Hoa Sen, Europipe and Tan A Dai Thanh...

- Hoa Sen Binh Dinh Plastic Pipe Factory was established in April 2016 and consists of 2 phases: Phase 1 includes 6 uPVC pipe production lines and 1 central mixing system with a capacity of 12,000 tons/year, which has been completed, put into production and produced the first products since January 2016. Phase 2 includes 6 uPVC pipe production lines and 1 module for the central mixing system with a capacity of 12,000 tons/year. Both phases are expected to be completed in December 2016 and have a total capacity of 24,000 tons/year.

- In addition, Stroman Vietnam Plastic JSC (a member of Tan A Dai Thanh Group) has also inaugurated the Stroman Hung Yen plastic pipe factory with an investment capital of 70 million USD divided into two phases. Of which, 35 million USD of the first phase will be invested in machinery and equipment. The goal is to build 20 warehouses in the North and Central regions, with an expected output of 20,000 tons, generating revenue of 1,000 billion VND. Phase II, by 2017, will complete the factory with items including machinery systems, operating the entire capacity of the Stroman Hung Yen factory. This unit will build 18 more warehouses, completing the construction of 36 warehouses in 36 provinces in the North and Central regions with an expected output of 70,000 tons of products, generating revenue of 3,000 billion VND.

- EuroPipe is a private enterprise with a large scale of investment in the production of HDPE plastic pipes, PPR heat-resistant plastic pipes, uPVC plastic pipes and accessories in Vietnam with a total investment of more than 400 billion VND.

As can be seen, competition in the construction plastic pipe market is gradually becoming much more fierce and the market share may have to be divided among these new businesses. Domestic plastic businesses still have the advantage thanks to their large scale and strong brand, however, we believe that if there are no reasonable policies to adapt to the competitive market, the market share of businesses will be affected.

Acquisitions by foreign enterprises - opportunities and challenges . The Vietnamese plastics industry with its rapid growth is receiving great attention from foreign corporations. Enterprises from Thailand, Japan and Korea have created a wave of acquisitions of plastic enterprises in Vietnam. Notably, the SCG Group from Thailand is expanding its reach in the Vietnamese market through a series of mergers and acquisitions. For the plastic packaging segment, SCG spent 44 million to acquire Tin Thanh Packaging (Batico), one of the five largest enterprises in the plastic packaging industry. Tin Thanh Plastic Company also unexpectedly sold 80% of its shares to SCG Group for 44.4 million USD. Not only that, SCG has also deeply penetrated the Vietnamese construction plastics industry when owning 23.8% of shares in Tien Phong Plastic and 20.4% in Binh Minh Plastic.

Up to now, SCG has spent about 121 million USD investing in 7 Vietnamese plastic enterprises. In addition, SCG also holds shares in a number of other companies specializing in the production of household plastics and packaging such as the Vietnam - Thai Plastchem Joint Venture, TPC Vina Plastic and Chemical Company, Chemtech Company and Minh Thai Plastic Materials Company. Not only Thai people, Korean and Japanese investors also like the Vietnamese plastic market. Typically, Japan's Oji Holding Corporation bought United Packaging Company, or Sagasiki Vietnam bought Goldsun Printing and Packaging Joint Stock Company. Recently, a Japanese investment organization, RISA Partners, also expressed its intention to invest in Dong A Civil Plastic Company. Korean Dongwon Systems Group also acquired two large enterprises at the same time, Tan Tien Plastic Packaging and Minh Viet Plastic Packaging - which are packaging companies belonging to Masan Group.

It can be seen that these foreign enterprises often choose the form of joint ventures to contribute capital and create influence on the market instead of having to build a brand from scratch. The acquisition of entire manufacturing and processing enterprises from buying capital from SCIC after divestment, or buying out small enterprises is expected to continue to appear with benefits from saving costs of market research, taking advantage of domestic resources, and at the same time exploiting the consumption needs of the domestic market. This wave will take place strongly to anticipate FTAs, preparing for export.

For the two plastics giants BMP and NTP, with the SCIC divestment plan approved by the government, it is highly likely that SCG will increase its ownership in these two companies. At the 2016 Annual General Meeting of Shareholders, BMP was approved to increase the room for foreign investors to 100% and the Board of Directors agreed to increase the room this year. However, BMP's charter still includes a number of conditional business lines, so the room expansion process is more complicated than other cases. However, we believe that this plan will be completed soon and the possibility of SCG continuing to increase its ownership in BMP is possible. As for NTP, the foreign room is almost not closed, mainly because SCG holds nearly 24%, largely due to the large holding ratio of internal shareholders and the largest shareholder is SCIC with an ownership ratio of 37.1%. If NTP agrees to increase foreign room to 100% like BMP, the possibility of a merger is quite high, and with the position of these two leading enterprises in the industry, the Thai people must accept to pay a price higher than the market price of the shares.

(Source: VCBS)

Source: https://nhuatienphong.vn/bai-viet/trien-vong-nganh-nhua-2017/680.html

![[Photo] National Assembly Chairman Tran Thanh Man visits Vietnamese Heroic Mother Ta Thi Tran](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/7/20/765c0bd057dd44ad83ab89fe0255b783)

Comment (0)