That was the sharing of Mr. Tran Le Minh - General Director of Vietnam Investment Credit Rating Company (VIS Rating) when talking to the press about the new regulations on professional securities investors being proposed in the draft amended Securities Law.

|

| Mr. Tran Le Minh - General Director of Vietnam Investment Credit Rating Company. (Photo: DT) |

Reporter (PV): Sir, there is a reality in the individual corporate bond market that the number of individual investors participating is very large, while in theory, this is a market for professional securities investors, especially institutional investors. What is your comment on this reality?

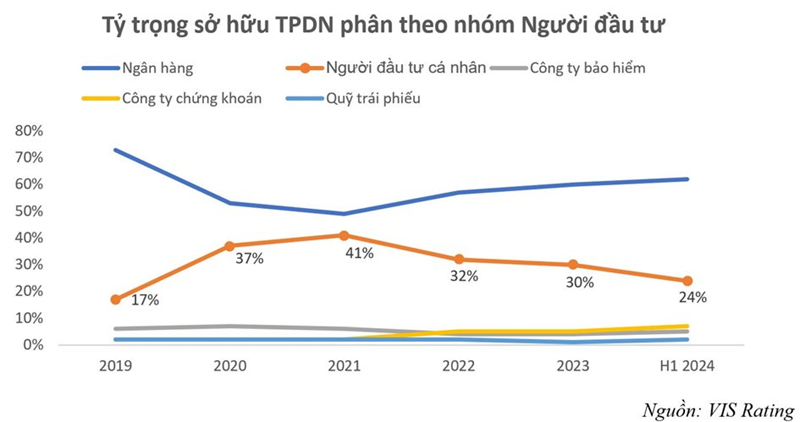

Mr. Tran Le Minh: This comment is correct, individual investors are the second largest group of corporate bond holders after banks and are much larger than other institutional investor groups such as insurance companies or investment funds. In 2021, individual investors held the largest corporate bond holders with a proportion of 41% of the total market size while banks held 49%. After recent developments, this proportion has gradually decreased to 24% by June 2024, but the second position remains unchanged.

One point to note is that many of the individual investors who hold corporate bonds are not professional investors but small individual investors; in many cases, investing in corporate bonds is an alternative channel to saving because they believe that corporate bonds are highly safe products - this is an unreasonable point from the reality of market development and needs to be adjusted.

PV: In addition to many other important contents, the Draft Law on Securities Amendment has added regulations related to professional securities investors. What do you think about the Drafting Committee's approach?

Mr. Tran Le Minh: The draft amended Securities Law is attracting many opinions from market members. Through studying the explanatory documents for the development of the Law, I see that the Drafting Committee has focused on the necessary points to resolve unreasonable issues in practice and create conditions for the corporate bond market to develop safely, stably and sustainably. In particular, the two key points are the regulations on professional securities investors (investors participating in the private corporate bond market) and the division of responsibilities to promote the issuance of corporate bonds to the public.

A notable point in the draft is the addition of a provision that professional securities investors participating in the purchase, trading, and transfer of private corporate bonds are organizations according to regulations. This also means that the regulation that privately issued corporate bonds can only be issued and traded between professional institutional investors. The Drafting Committee has also provided detailed explanations for this opinion based on actual market developments and market characteristics as well as practices and experiences from markets in other countries in the region. I think that market members have reached a consensus on the view that the privately issued corporate bond market is a market for professional investors.

Due to the specific nature of the privately issued corporate bond market, the level of information disclosure related to bonds and issuers is significantly less, state management is reduced and the market's self-governance role is enhanced. On the other hand, the diversity in the terms and conditions of bonds has made this type of corporate bond a complex product that requires specialized knowledge to invest and is not suitable for small investors.

Along with that, regulations related to the market will always need to be updated and supplemented to ensure that privately issued corporate bonds cannot be sold to investors who do not have the necessary knowledge and experience for investment. This is a normal activity to ensure the protection of the legal framework for small investors.

PV: With your perspective and research, how do countries around the world view the development of individual corporate bond market participants?

Mr. Tran Le Minh: Regional markets, specifically the ASEAN+3 group (China, Korea and Japan), all have specific legal regulations for the private corporate bond market and regulations on investors in this market. The general view is that private corporate bonds are not a market for the general public. Investors participating in the market must meet certain conditions.

The ASEAN+3 Bond Market Forum (ABMF), supported by the Asian Development Bank (ADB), has conducted research on these issues and pointed out that if individual investors are allowed to participate in investment, they must have experience, knowledge, and expertise in the bond market in addition to having large enough assets. Currently, regulations related to professional investors only provide regulations related to assets and transactions, and have not quantified the requirements for experience and knowledge. Regulations related to professional individual investors in all countries in the above group are stipulated in the highest legal documents, which are laws or decrees.

|

PV: As an expert with experience in financial market research, what do you suggest for the individual corporate bond market to develop in its true nature and goals, but also in harmony with the actual development situation of this market?

Mr. Tran Le Minh: It should also be noted that, in stock markets around the world, individual corporate bonds are considered a type of "excepted securities" and are therefore not subject to the scope of the Securities Law. When issuing, the issuing organization does not have to register and is not subject to the management of the Securities Commission of each country.

Recently, the corporate bond market has revealed practical shortcomings and has been addressed through the issuance of Decree No. 65/2022/ND-CP.

The amendment of points related to the market for corporate bonds issued to the public and regulations on professional securities investors in the draft amended Securities Law with a shortened process has shown the urgency of the issue. Therefore, this amendment of the Law is very suitable in terms of timing and further consolidates the points that need to be adjusted for the market for corporate bonds issued individually, which have been initiated since the promulgation of Decree 65/2022/ND-CP.

To achieve the goal of bringing the corporate bond market size to 25% of GDP by 2030, the market needs a period of rapid recovery. Observable figures to assess the market recovery are the size of outstanding bonds in the entire market reaching the peak in 2022 and the value of newly issued bonds being higher than the value issued in 2021. Creating a suitable legal framework to promote rapid recovery is important, but stability cannot be sacrificed for growth.

Therefore, I believe that the goal of the draft amendment to the current Securities Law is to create a stable and long-term development period that is consistent with market developments, creating the premise for a more transparent market recovery and not to repeat the unreasonable points or risks that occurred in the individual corporate bond market in the recent period.

PV: Thank you!

Source: https://dangcongsan.vn/kinh-te/trai-phieu-doanh-nghiep-rieng-le-nen-danh-cho-nha-dau-tu-chung-khoan-chuyen-nghiep-678187.html

Comment (0)