Global commodity markets continued to experience significant volatility during the trading week of May 4-8 as investors continuously adjusted their expectations based on new developments in the Middle East. Within just a few sessions, market sentiment shifted rapidly from concerns about supply disruptions to expectations of de-escalation of conflict, then back to caution amid the risk of military escalation.

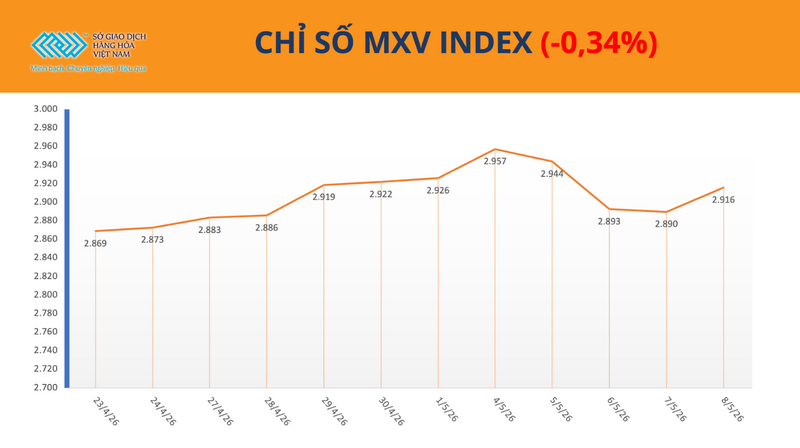

According to the Vietnam Commodity Exchange (MXV), developments last week showed the market's sensitivity to signals from the Middle East. Any information related to a potential de-escalation of conflict quickly weakened buying pressure in the energy market. Conversely, any signs of escalation immediately brought back concerns about supply disruptions, supporting oil prices and safe-haven assets. Amidst the continuous reversal of capital flows driven by geopolitical expectations, the MXV-Index ended the week down slightly by 0.34% at 2,916 points.

Oil prices fell across the board.

MXV-Index. Source: MXV

According to MXV, the energy sector experienced a sharp correction this past week after a period of rapid growth. However, oil price movements indicate that the market remains focused on the risk of supply disruptions in the Strait of Hormuz – a shipping route for approximately 20% of global commercial oil.

At the start of the week, Brent crude oil prices fluctuated as US- Iran tensions continued to escalate and shipping through the Hormuz Strait was affected. Concerns about disruptions to oil supplies from the Middle East fueled speculative buying in the energy market.

However, this sentiment quickly reversed after just a few days. News that the US and Iran had signaled their readiness to resume negotiations caused the market to sharply reduce expectations of a prolonged confrontation. As a result, oil prices plummeted nearly 8% on May 6th – one of the sharpest declines since the beginning of the year.

By the end of the week, the market was once again in a state of flux as new military developments emerged around the Persian Gulf. This shows that oil prices now reflect not only actual supply and demand, but also the level of investor concern about geopolitical risks.

MXV believes that the oil market is heavily influenced by expectations. When signs of de-escalation appear, the price premium due to concerns about the conflict quickly narrows. Conversely, as soon as tensions escalate, risk-averse buying returns to the market.

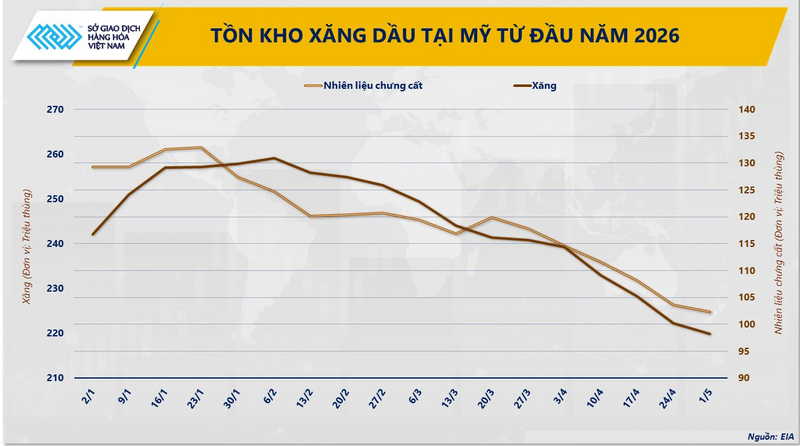

Regarding supply and demand, reports from the U.S. Energy Information Agency (EIA) continued to support oil prices as commercial crude oil inventories fell by more than 2.3 million barrels in the week ending May 1st. Gasoline inventories also decreased for the 12th consecutive week ahead of the peak summer consumption season, indicating that fuel demand in the U.S. remains positive.

US gasoline and diesel inventories since the beginning of the year. Source: MXV

At the end of the week, Brent crude oil prices fell by more than 6%, to around $101 per barrel; WTI crude oil fell by about 6.4%, to just over $95 per barrel.

Domestically, despite sharp adjustments in world oil prices during the latter half of the week, the fact that international prices remained above $100 per barrel for several previous sessions continued to put pressure on the May 8th price adjustment.

Silver leads the recovery of the group of metals.

In contrast to energy, the metals group recorded a positive recovery week as market sentiment gradually stabilized. COMEX silver became the focus of investment flows, rising in 4 out of 5 sessions and closing the week up approximately 5.8%.

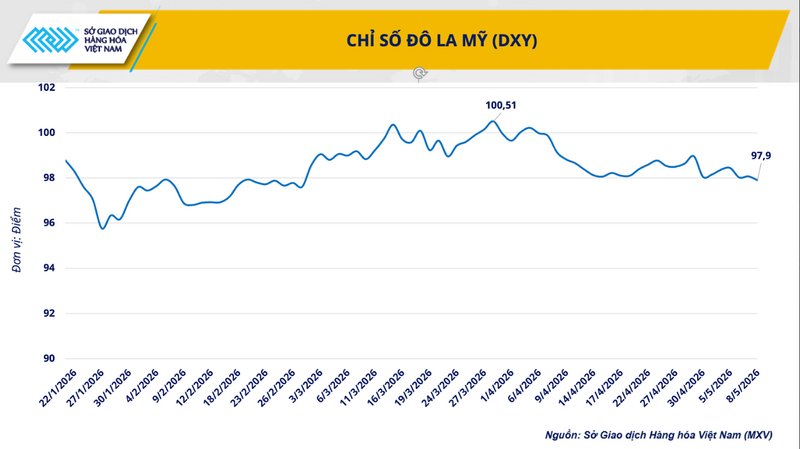

According to MXV, the performance of silver over the past week quite clearly reflects the shift in expectations in the global financial market. As the risk of temporary energy disruptions eased, inflationary pressures also eased, causing the yield on 10-year US Treasury bonds to fall from around 4.45% to around 4.36%. At the same time, the weakening of the Dollar Index (DXY) below 98 points also significantly supported assets priced in USD such as silver.

US Dollar Index (DXY). Source: MXV

Besides macroeconomic factors, the silver market also recorded positive signals from speculative capital flows as the net long position of Managed Money on the COMEX exchange continued to increase. Global silver ETFs also maintained a net buying trend, indicating that market sentiment is gradually leaning towards the scenario where the Fed has more room to ease policy in the final months of the year.

However, MXV believes that the precious metals market has not yet truly entered a sustainable uptrend. The US labor data for April continues to show that the world's largest economy remains relatively resilient, thus making it likely that the Federal Reserve (Fed) will continue to maintain a cautious stance on inflation.

This week, market attention will be focused on US CPI and PPI data. This is seen as a crucial test to assess whether the recent energy shock has begun to spill over into producer prices and consumer inflation. The results of this data will directly impact interest rate expectations, the US dollar, and money flow trends across all commodity markets.

Source: https://congthuong.vn/gia-dau-the-gioi-giam-hon-6-456068.html

![[Photo] Strengthening character and expertise: Intense training for artillery soldiers.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/06/30/1782815602541_lu-368-1875-4571-jpg.webp)