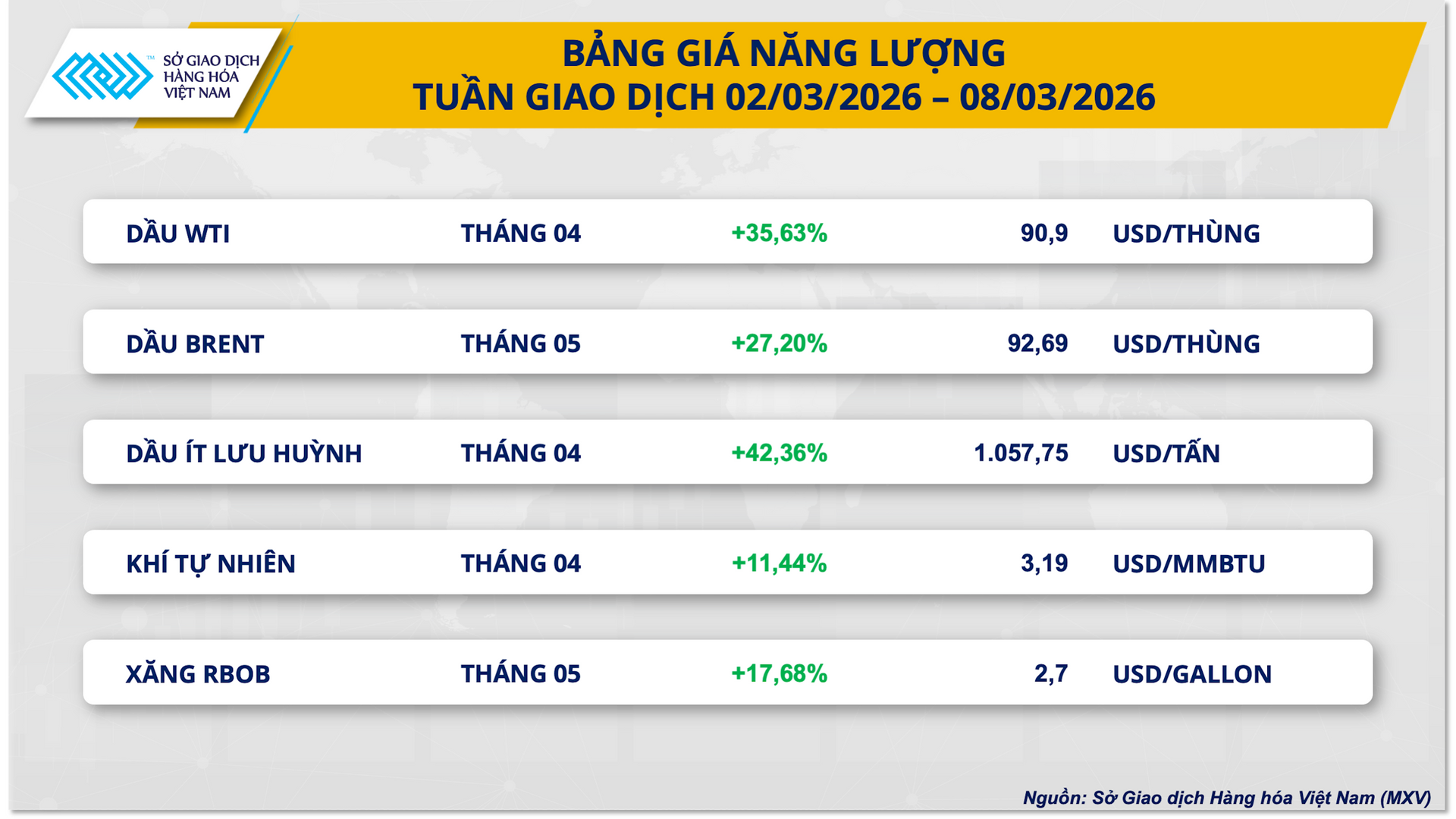

In the energy market, world oil prices experienced a sharp increase this week as geopolitical risks in the Middle East escalated.

At the close of trading on March 6th, WTI crude oil prices surged to $90.9 per barrel, a 35.6% increase compared to the end of the previous week and reaching their highest level since September 2023. Meanwhile, Brent crude oil prices also rose 27.2%, to nearly $92.7 per barrel – their highest level since April 2024.

According to the Vietnam Commodity Exchange (MXV), the sharp rise in oil prices reflects the growing market concern about potential supply disruptions from the Middle East – a region that accounts for a significant share of global oil production.

Traders therefore quickly increased their long positions to hedge against volatility. At the same time, many refineries in Asia and Europe actively sought alternative sources of supply to compensate for the oil shortage. With the US being the world's largest crude oil producer, WTI oil traded on the NYMEX clearly benefited, especially as global refining margins remained attractive.

In Vietnam, the heat from the global market quickly spread to the domestic petroleum market. Amidst the continuous sharp increase in refined oil prices in Singapore, the price management mechanism was flexibly adjusted after the Government issued Resolution 36/NQ-CP on March 6th, allowing for emergency price adjustments when the base price fluctuates by 7% or more. Immediately afterwards, the Ministry of Industry and Trade issued an urgent document to implement supplementary price adjustments outside the normal price adjustment cycle.

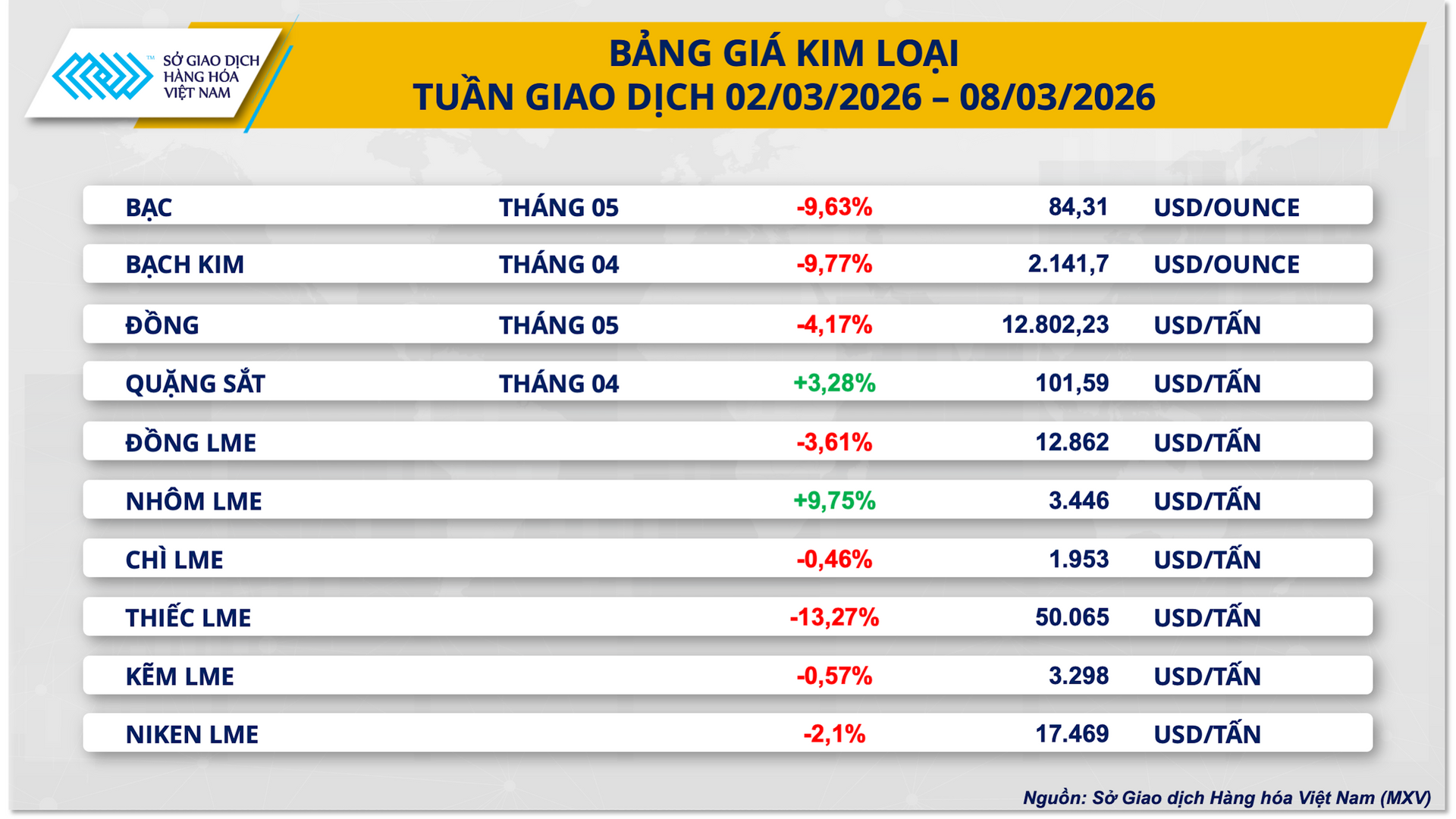

Conversely, the precious metals market saw less positive developments. COMEX silver futures for May delivery fell 9.6% this week, retreating to $84.3 per ounce as the US dollar strengthened.

The US Dollar Index (DXY) rose approximately 1.4% to nearly 99 points as investors adjusted their expectations regarding the Federal Reserve's monetary policy. The market now forecasts that the Fed may only implement one or two interest rate cuts this year, with the first likely to occur in September.

Despite short-term pressure, the silver market still shows supportive signals from supply and demand factors. Silver inventories at major trading centers such as Shanghai and COMEX have fallen sharply since the beginning of the year, reflecting continued high physical demand, particularly in high-tech and clean energy industries. These factors are expected to continue supporting silver prices in the medium and long term.

Source: https://hanoimoi.vn/gia-dau-bung-no-mxv-index-tang-hon-6-737018.html

Comment (0)