Many challenges in the short term.

Savills' recently released Q4 2023 Ho Chi Minh City real estate market report shows that the apartment segment is facing several short-term challenges.

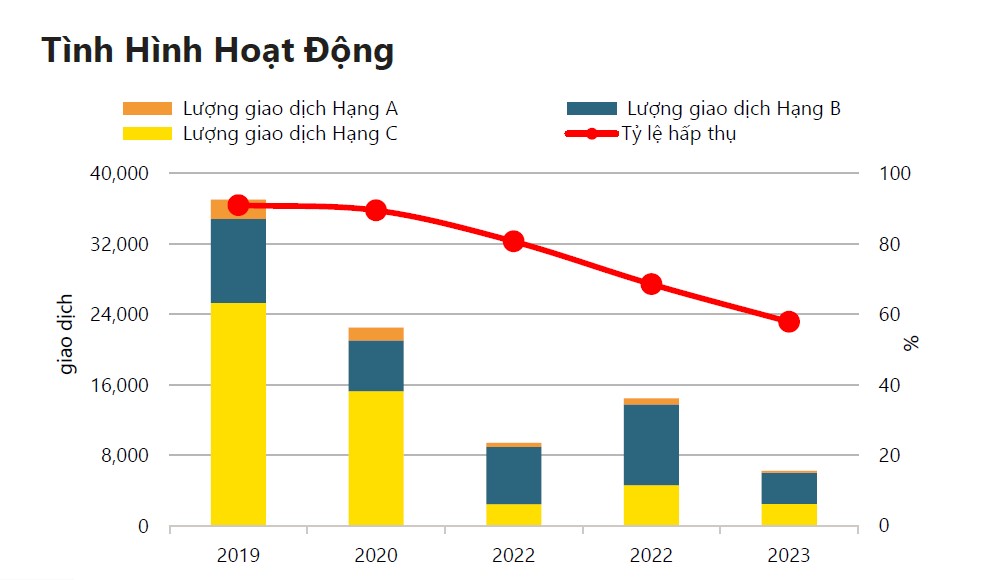

Accordingly, the primary supply for the whole of 2023 reached only 10,700 units, the lowest figure in the past 10 years. In Q4 2023 alone, the primary supply was 7,600 units, unchanged quarter-on-quarter but down 5% year-on-year. New supply accounted for 37% of the primary supply. Of this, two prominent projects, The Privia and its next phase, The Glory Heights, led 88% of the new supply. Meanwhile, the report did not record any new Grade A supply in the quarter.

Furthermore, the volume of apartment transactions over the past 10 years has steadily decreased by 7% annually. Amidst the scarcity of supply and high selling prices in 2023, the market only recorded 6,200 transactions. However, in the fourth quarter alone, the transaction situation improved with 3,000 units, a 52% increase quarter-on-quarter and a 120% increase compared to the same period last year.

Primary supply recorded in 2023 was the lowest in the last 10 years.

Troy Griffiths, Deputy Managing Director of Savills Vietnam, commented: “The short-term challenge for the apartment segment still stems from the scarcity of new supply and high selling prices. As homebuyer sentiment improves and there aren't too many alternative investment options, the housing market will recover.”

The absorption rate improved by 14 percentage points quarter-on-quarter and 23 percentage points year-on-year to 40%. New supply accounted for 78% of the transaction volume and was absorbed at 84%; these projects sold well due to clear legal status before launch, long payment terms, bank loan support, and accessible prices ranging from VND 2-5 billion per unit. Excluding new supply, market transactions remained weak with only 670 units sold, corresponding to an absorption rate of 14%.

Report on apartment transactions based on data from Savills.

One positive point in Savills' data is that in 2024, new supply is expected to quadruple compared to 2023. Class B will account for 44% of the market share, Class A will have 37%, while Class C will only have 19%. By 2026, an estimated 40,800 units from 116 projects are expected to be launched.

Affordable apartments can only be found in provinces surrounding Ho Chi Minh City.

According to Savills' report, primary sales prices in Q4 2023 returned to 2020 levels at VND 69 million/m2 (net usable area), a decrease of 36% quarter-on-quarter and 45% year-on-year, after many high-end projects had to temporarily close some of their inventory. Simultaneously, properties priced under VND 2 billion completely disappeared from the market last year. The supply of properties priced between VND 2-5 billion dominated the market, accounting for nearly 90%.

Between 2024 and 2026, the supply of apartments priced between VND 2-5 billion will decrease significantly, while products in the VND 5-10 billion range will emerge and dominate the market. Buyers in Ho Chi Minh City may choose to explore neighboring provinces to find more affordable housing options. By 2024, Binh Duong, Dong Nai, and Long An are expected to account for 96% of the supply of apartments priced under VND 5 billion.

According to Savills' 2023 survey of 30 Grade A and B projects, rental yields remained stable year-on-year at 4.8%, but property value growth decreased by 1.9 percentage points year-on-year to 2.9%. Therefore, the total return on apartment investment in 2023 decreased by 1.7 percentage points compared to the previous year, to approximately 7.7% year-on-year.

Ms. Giang Huynh, Deputy Director and Head of Research and S22M at Savills Ho Chi Minh City, analyzed: “Investment returns from apartments in Ho Chi Minh City tended to decrease slightly during the 2019-2023 period. According to our data, areas such as the former District 2, District 3, and District 10 had the highest investment returns during that time.”

Ms. Giang Huynh, Deputy Director, Head of Research and S22M Department, Savills Ho Chi Minh City

Over the past decade, the supply of new apartments in Ho Chi Minh City's 22 districts has decreased by 253,000 units. Notably, supply in the former District 9 area decreased by 21%, accompanied by a 15% annual price increase. Supply in District 1 also decreased by 2% but saw a significant annual price increase of 39%.

The expert also stated that although overall returns have decreased over the past five years, they are still higher than deposit interest rates. This indicates that apartments remain a profitable investment channel. In the short term, rental yields are expected to increase due to a decrease in the number of apartments being handed over and deposit interest rates remaining low.

Source

![[Photo] National Assembly Chairman Tran Thanh Man working with the Standing Committee of the Law and Justice Committee](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/05/21/1779378929214_ndo_br_1-4610-jpg.webp)

![[Photo] General Secretary and President To Lam presides over a working session with the Central Policy and Strategy Committee on the development of the materials industry.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/05/21/1779359935432_a3-bnd-3129-1412-jpg.webp)

Comment (0)