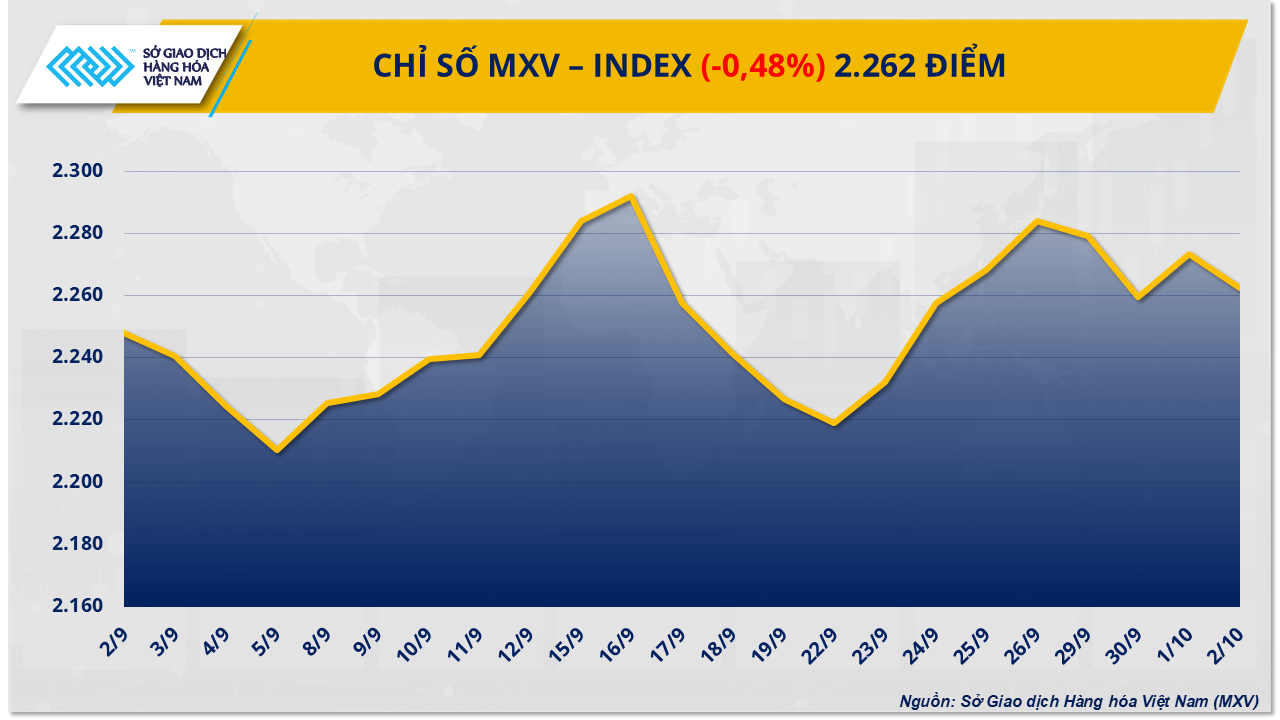

Oil prices hit their lowest level since May.

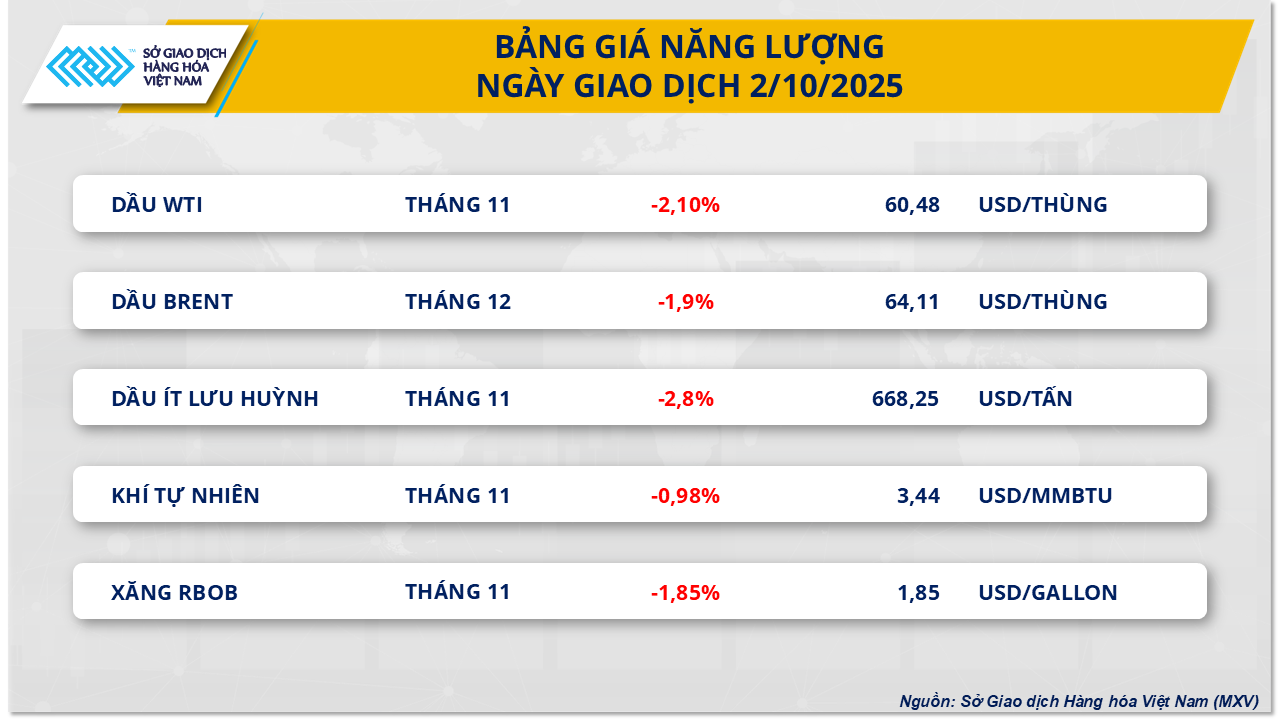

According to the Vietnam Commodity Exchange (MXV), the energy sector saw a simultaneous decline yesterday, with all five commodities trading in the red. Notably, crude oil prices continued their streak of four consecutive days of decline.

Specifically, Brent crude oil prices fell nearly 1.9%, to $64.11 per barrel – the lowest level since the end of May; WTI crude oil fell even more sharply, by 2.1%, closing at $60.48 per barrel, the lowest level in 5 months.

The downward pressure on prices mainly stems from the prospect of oversupply. The market is focusing on the OPEC+ meeting on October 5th, with many predicting that the alliance will continue to increase production in November. According to analysis by JPMorgan Chase, the largest investment bank in the US, the combination of the potential for further supply increases, slower global refining activity due to maintenance, and demand entering a low point will lead to increased inventories and continue to weigh on prices.

In the U.S., data from the Energy Information Agency (EIA) further reinforced this trend. In the week ending September 26th, inventories of crude oil, gasoline, and distillate fuels all increased. At the same time, refinery operating capacity and output decreased, reflecting weakening short-term fuel demand.

Domestically, retail fuel prices were adjusted upwards on October 2nd, significantly impacted by Russia's fuel export ban. Diesel saw the sharpest increase, rising by 380 VND/liter (2.04%), while E5RON92 and RON95 gasoline only edged up slightly by 6 VND/liter (0.03%) and 44 VND/liter (0.22%) respectively.

According to the Ministry of Industry and Trade and the Ministry of Finance, domestic price fluctuations reflect the combined impact of several factors: OPEC+ maintaining its production increase trend, rising US oil reserves, slowing global demand, and escalating geopolitical tensions between Russia and Ukraine.

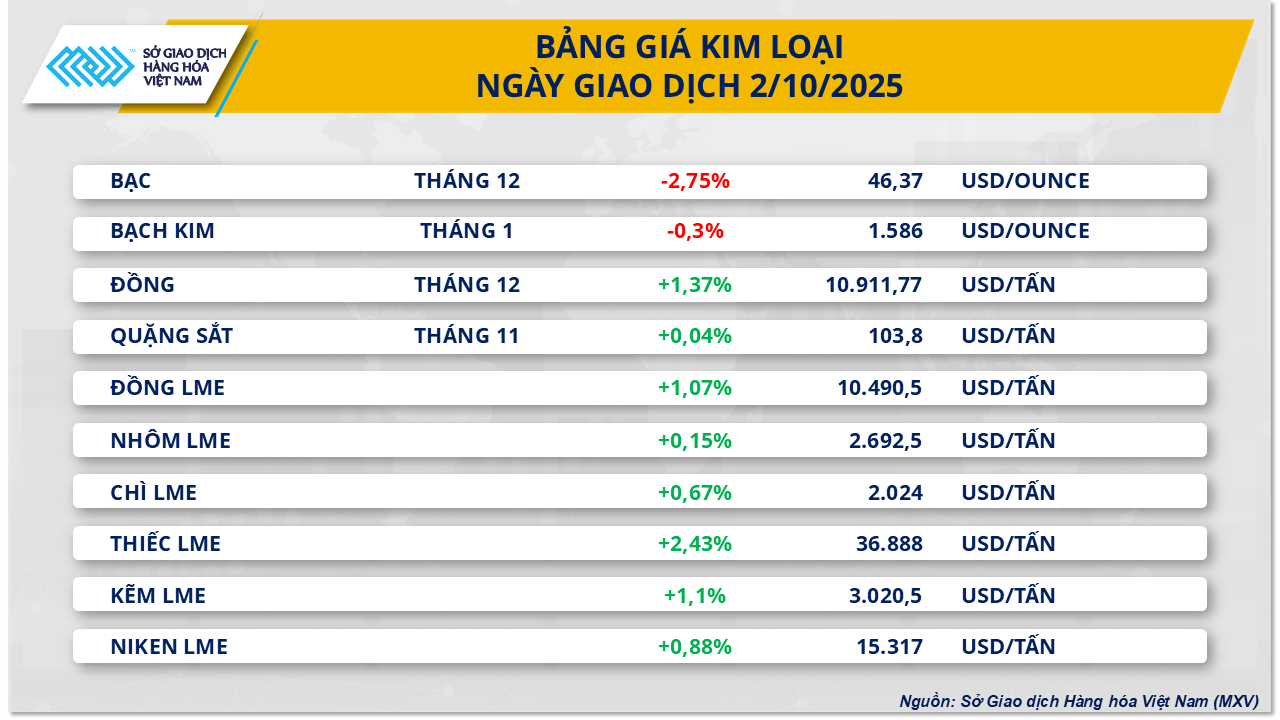

Concerns about tight supply are supporting copper prices.

Amid a polarized metals market, the COMEX copper index rose nearly 1.4% to $10,911 per ton yesterday. The main driving force came from concerns about the potential risks to global supply.

In Chile, the world's largest copper producer, August production fell nearly 10% year-on-year to just over 423,600 tonnes, according to the National Statistics Agency (INE). This is the sharpest decline since May 2023. The state-owned Codelco had previously warned that production might only remain around 5.5 million tonnes per year due to difficulties in deep-sea mining, declining ore content, and rising costs. Following the El Teniente mine collapse in late July, Codelco revised its 2025 production forecast downward by approximately 30,000 tonnes, to 1.34-1.37 million tonnes.

Global copper supply has also been affected by incidents at the Grasberg mine in Indonesia – the world's second-largest. The Freeport-McMoRan mine had to declare force majeure after a mudslide in early September disrupted mining operations. According to BMI, the top 20 mines alone account for approximately 36% of global production this year, so any incidents at these mines could have ripple effects throughout the supply chain.

Meanwhile, the demand outlook remains positive. China, the largest consumer of copper, recently announced its Action Plan for Stabilizing Non-Ferrous Metals Growth for 2025-2026, aiming for an average annual production increase of 1.5% across 10 key metals, including copper. Beijing also plans to expand copper applications in new energy vehicles and telecommunications infrastructure, demonstrating the metal's continued importance in its industrial development strategy.

The combination of supply disruption risks at major mines and the prospect of sustained demand from China is providing significant support for copper prices, while also strengthening the red metal's position among industrial raw materials.

Source: https://baotintuc.vn/thi-truong-tien-te/mxvindex-tiep-tiep-giang-co-tren-vung-2200-diem-20251003083035501.htm

![[Photo] General Secretary and President To Lam meets with National Assembly delegates from ethnic minorities.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/04/20/1776696701056_a1-bnd-8331-3342-jpg.webp)

![[Image] National Assembly discusses the implementation of the socio-economic development plan.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/04/20/1776696707422_ndo_br_img-20260420-185419-jpg.webp)

Comment (0)