Ms. Vu Phuong Thuy, a communications specialist at a securities company on Ton Duc Thang Street (Saigon Ward, Ho Chi Minh City), said that her monthly income ranges from 29-30 million VND. However, she hasn't considered buying a house in the city yet.

According to Ms. Thuy, owning a home in Ho Chi Minh City is becoming increasingly out of reach as house prices have risen too high while incomes are increasing very slowly. She finds renting a house more suitable than owning one.

"Every month, I spend about 5 million VND on rent. Economically speaking, renting is much more advantageous than buying a house in the current climate. Because house prices are rising, interest rates are increasing, and the financial pressure is immense," said Ms. Thuy.

According to Ms. Thuy, this is also a good time to accumulate capital. When interest rates fall and other conditions are favorable, it won't be too late for her to buy a house.

Many young people in Ho Chi Minh City choose to rent long-term instead of buying a house. (Illustrative image: Dai Viet)

Mr. Tran Dinh Thang, residing on Hoang Sa Street (Nhieu Loc Ward, Ho Chi Minh City), shared that he and his wife and children are currently renting a small house for 10 million VND per month. His family hasn't considered buying a house in the city yet because renting is more suitable for them.

According to Mr. Thang, the combined monthly income of him and his wife is approximately 55 million VND. This amount is enough for their family of three to live comfortably. If they were to buy a house, they would have to borrow money from friends and relatives, in addition to the pressure of bank loans. Meanwhile, renting a house allows the family to spend more freely.

"We've decided that owning a house or property in Ho Chi Minh City isn't necessary. We can rent a house long-term, as long as it ensures the best possible quality of life for our family," Thang said.

According to Thang, instead of spending a large sum of money to buy a house, he and his wife would use it to invest in their children's education or travel together, enjoying a happy life.

According to observations by VTC News reporters in Ho Chi Minh City, many young people are hesitant to buy a house. They don't consider owning a home in the city too important, opting instead for long-term rentals.

Renting is the most popular choice.

Research by the Vietnam Association of Real Estate Brokers (VARS) shows that over 60% of young people under 35 in major cities like Ho Chi Minh City, Hanoi, and Da Nang are prioritizing renting. They consider this the optimal solution to reduce financial burdens and enjoy freedom amidst rising real estate prices.

PropertyGuru's survey results also indicate that the trend of searching for rental properties has increased by nearly 22% in the past few years. The group of customers aged 25-34 who are searching for rental properties has the highest rate, accounting for nearly 62%. Even the high-income group (21-40 million VND/month) has a rental search rate of up to 42%.

Representatives from VARS argue that high housing prices and the lack of preferential interest rates are barriers making it difficult for many people to buy a home. This also leads people to choose to rent.

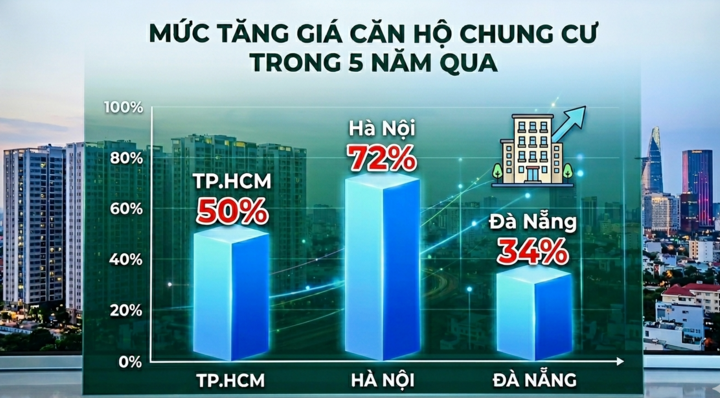

VARS found that apartment prices in Ho Chi Minh City have increased by 50%, Hanoi by 72%, and Da Nang by 34% in just the past five years. Meanwhile, the average income of people has only increased by about 6-10% per year, a very low increase of only 6.8 - 8.9 million VND per month.

"If people borrow an average of 1.5-2 billion VND to buy a house, they have to pay 18-25 million VND per month in principal and interest, which is 4-5 times higher than the cost of renting. Therefore, renting will significantly reduce financial pressure for people if they don't need to accumulate assets," a VARS representative stated.

Rising housing prices in cities are becoming a barrier for young people to buy homes. (Photo: Dai Viet)

The policy of supporting people under 35 to buy houses is being implemented quite extensively by banks. However, according to statistics from the State Bank of Vietnam, as of the end of March 2026, outstanding loans to this group of customers only reached about 240 billion VND. This is a very low figure compared to expectations.

According to Mr. Nguyen Van Dinh, Chairman of the Vietnam Real Estate Brokers Association, young people still face many difficulties in borrowing money to buy a house. Borrowing means having to repay the debt over 15-25 years, or having to cut back on many other expenses to have a shorter repayment period.

Furthermore, the unpredictable nature of floating interest rates discourages many young people from borrowing. Therefore, many young people choose to rent instead of owning a home and struggling to repay the debt.

According to a representative from Avison Young Vietnam, in the short term, serviced apartments, inner-city mini-apartments, and small-sized apartments suitable for single people or nuclear families are expected to continue to be popular, with stable rental yields and occupancy rates.

"Given that the State has identified rental housing as a strategic pillar from now until 2030, it is necessary to diversify rental housing types. In particular, the model of long-term commercial rental housing (build-to-rent), operated systematically according to unified standards, should be considered for piloting," an Avison Young representative analyzed.

According to Avison Young Vietnam, to improve housing access for young people, policies need to focus more on supply structure rather than just controlling credit.

Specifically, the definition of "affordable housing" and the design of incentive mechanisms are similar to those for social housing. Affordable housing is a segment with low profit margins and long payback periods, while investment costs are constantly increasing. Without support such as shortened approval times, tax incentives, or permission to increase building density to offset costs, businesses will not find it commercially viable to invest systematically and on a large scale.

According to Avison Young Vietnam, the legal framework should be clarified to promote the rental housing market. Specifically, the rights and obligations of the parties regarding lease terms or price increase mechanisms should be codified to protect tenants.

Finally, consideration should be given to expanding the lease-to-own option for commercial housing to reduce the financial burden on young people with genuine housing needs, in addition to leveraging loan options.

Source: https://vtcnews.vn/nguoi-tre-ngay-cang-ngai-mua-nha-ar1022022.html