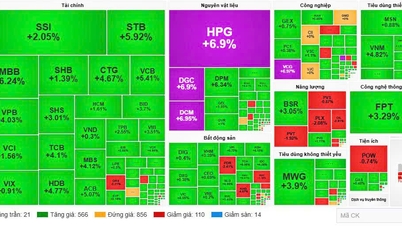

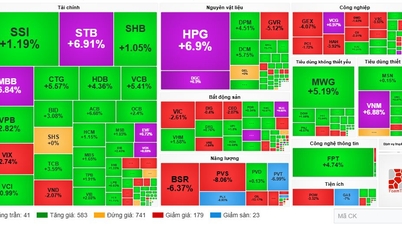

At the close of trading on November 6th, the VN-Index fell 12.25 points to 1,642.64 points; the VN30 index fell 16.87 points to 1,869.60 points. On the Hanoi Stock Exchange, the HNX-Index decreased 0.55 points to 266.15 points; the UPCOM-Index fell 0.28 points to 116.22 points. Total market liquidity reached VND 20,235 billion, with a trading volume of over 687 million shares.

The banking sector was the focal point of weakness, with red dominating:SHB fell 2.16%, HDB 3.06%, VPB 2.56%, MBB 0.84%, TCB 1.47%, VCB 0.82%, ACB 1.17%, BID 0.39%, and EIB 2.47%. This simultaneous correction caused the VN-Index to lose its crucial support and created a ripple effect on other sectors.

In the securities sector, SSI fell 1.72%, VIX fell 2.96%, VND fell 1.75%, and HCM fell 2.17%. Meanwhile, the real estate sector showed mixed performance, with VIC rising 0.63%, KBC rising 1.71%, and DIG rising 0.74%, while DXG, VHM, PDR, and KDH continued to decline.

The industrial, consumer, and steel sectors also recorded negative developments: CTD decreased by 5.99%, VJC by 1.95%, HPG by 0.76%, NKG by 1.18%, HSG by 0.86%, DPM by 1.81%, MSN by 1.75%, MCH by 4.37%, while MWG increased slightly by 0.12%.

The only bright spots came from the oil and gas sector, with PVD rising 1.86% and PVS increasing 1.17%. Additionally, several infrastructure and transportation stocks such as CII, HHV, VSC, and HAH also maintained their gains.

Net selling pressure from foreign investors remained high at VND 1,067 billion, concentrated on STB (VND 179.6 billion), VPB (VND 102.5 billion), HPG (VND 89.2 billion), SSI (VND 61.1 billion), and CTG (VND 59.7 billion). Conversely, they net bought MWG (VND 177.5 billion), VIC (VND 71.7 billion), VNM (VND 31 billion), PVD (VND 15.7 billion), and GMD (VND 13.9 billion).

Accordingly, institutional capital is trending towards portfolio restructuring, prioritizing leading stocks with strong financial foundations and stable profitability. In terms of index impact, VIC, BCM, and BMP are the three stocks providing the most positive support, while VPB, VCB, and HDB have the most negative impact on the VN-Index.

Compared to the region, the Vietnamese market is moving against the trend. However, the domestic decline is considered short-term, with expectations that blue-chip stocks will continue to support the market once sentiment stabilizes.

Source: https://baotintuc.vn/thi-truong-tien-te/vnindex-giam-hon-12-diem-20251106171509026.htm

![[Photo] Meeting of the Standing Committee of the National Assembly Party Committee with the Standing Committee of the Government Party Committee on the First Session of the 16th National Assembly](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/03/10/1773107502031_ndo_br_thu-tuong-pham-minh-chinh-va-chu-tich-qh-tran-thanh-man-dong-chu-tri-hoi-nghijpg-jpg.webp)

![[Photo] Da Nang: Mountainous commune adorned with flags and flowers, ready for election day.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/03/10/1773113803384_ndo_br_9-jpg.webp)

Comment (0)