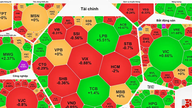

The VN-Index briefly dropped nearly 60 points, but then recovered, closing the session down 48.37 points.

Following the volatile trading session on June 8th, the VN-Index retreated to 1,790.59 points, equivalent to a decrease of -2.63%.

According to trading statistics on the HSX exchange (representing the VN-Index), as many as 250 stocks declined, while only 66 stocks increased.

Stock markets plunged on June 8th.

The HNX and UpCom exchanges also saw a wave of red, with the number of declining/rising stocks being 106/40 and 140/102 respectively.

Investors believe the VN-Index crash stemmed from the negative amplification of sentiment from the US financial market and the Middle East conflict.

In the US, the Dow Jones index fell sharply last weekend, plummeting nearly 700 points amid a massive sell-off in technology stocks.

Consequently, shares of companies like Nvidia, Qualcomm, and Microsoft were sold off, negatively impacting the global technology industry.

However, analysts believe that the collapse of the world's leading technology stocks is due to their rapid growth rate over the past year, which has even increased by 70-80% since the beginning of 2016.

Global stock markets, including Vietnam's, were also affected by this information, causing investor sentiment to waver.

In addition, the US and Israeli attacks on Iran caused oil prices to rise again, thereby impacting global stock markets.

From a technical perspective, the VN-Index may continue to fluctuate in an attempt to find a point of equilibrium amidst dwindling liquidity.

According to VPS data, the trading value on June 8th reached nearly 20,000 billion VND across the entire market, of which HSX accounted for over 18,900 billion VND, HNX nearly 1,000 billion VND, and UpCom over 800 billion VND.

Market liquidity was higher than the previous two sessions, but still remained low, while there were no convincing signs of money flowing back into the market.

This is evidenced by the fact that selling pressure remained dominant in most sectors on June 8th, particularly in the leading stocks representing each sector.

In the banking sector, leading stock VCB fell 0.65% with weak liquidity, while the industry's "big brother" BID also dropped 2.38% with weak liquidity and closed at its lowest price of the session.

Other bank stocks such as VPB, MBB, CTG, and TCB also closed at their lowest prices of the session. This signals that bank stocks will continue to face selling pressure in the following sessions and will only stop if bargain-hunting buying occurs.

The real estate sector showed a few bright spots, such as DXG with a technical rebound, but lacked group consensus, with red dominating. In particular, the immense pressure from the VinGroup stocks caused the VN-Index to fall sharply, with VIC down 5.80% and VHM down 3.49%.

The securities sector was in a similar situation to real estate and banking, with SSI down 2.41%, VND down 4.26%, TCX down 2.01%, etc.

However, the market's support lies in the fact that most stocks in leading sectors have not yet broken through their support levels (based on technical analysis). Therefore, in a positive scenario, if institutional capital returns, these stock groups could regain their upward momentum, thereby supporting the VN-Index.

Amidst the downturn in the Vietnamese stock market, foreign investors reverted to their selling habits, net selling over 600 billion VND on the HSX.

The focus of net selling by foreign investors was concentrated inFPT (-121.89 billion VND), VHM (-113.37 billion VND), MSN (-93.52 billion VND), VIC (-83.38 billion VND)...

Conversely, foreign investors were the biggest buyers of VCB shares with a value of VND 98.72 billion,ACB with VND 98 billion, STB with VND 42 billion, and so on.

Source: https://suckhoedoisong.vn/chung-khoan-do-lua-phien-8-6-169260608154712941.htm

![[Photo] Opening Ceremony of the 13th National Congress of the Ho Chi Minh Communist Youth Union](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/06/24/1782286753905_ndo_br_1-8510-jpg.webp)

![[Photo] The 13th National Congress of the Youth Union conducts personnel work.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/06/24/1782299943080_ndo_br_1-6868-jpg.webp)

![[Photo] General Secretary and President To Lam attends the Central Public Security Party Committee Conference](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/06/24/1782302063612_a1-bnd-9302-9166-jpg.webp)