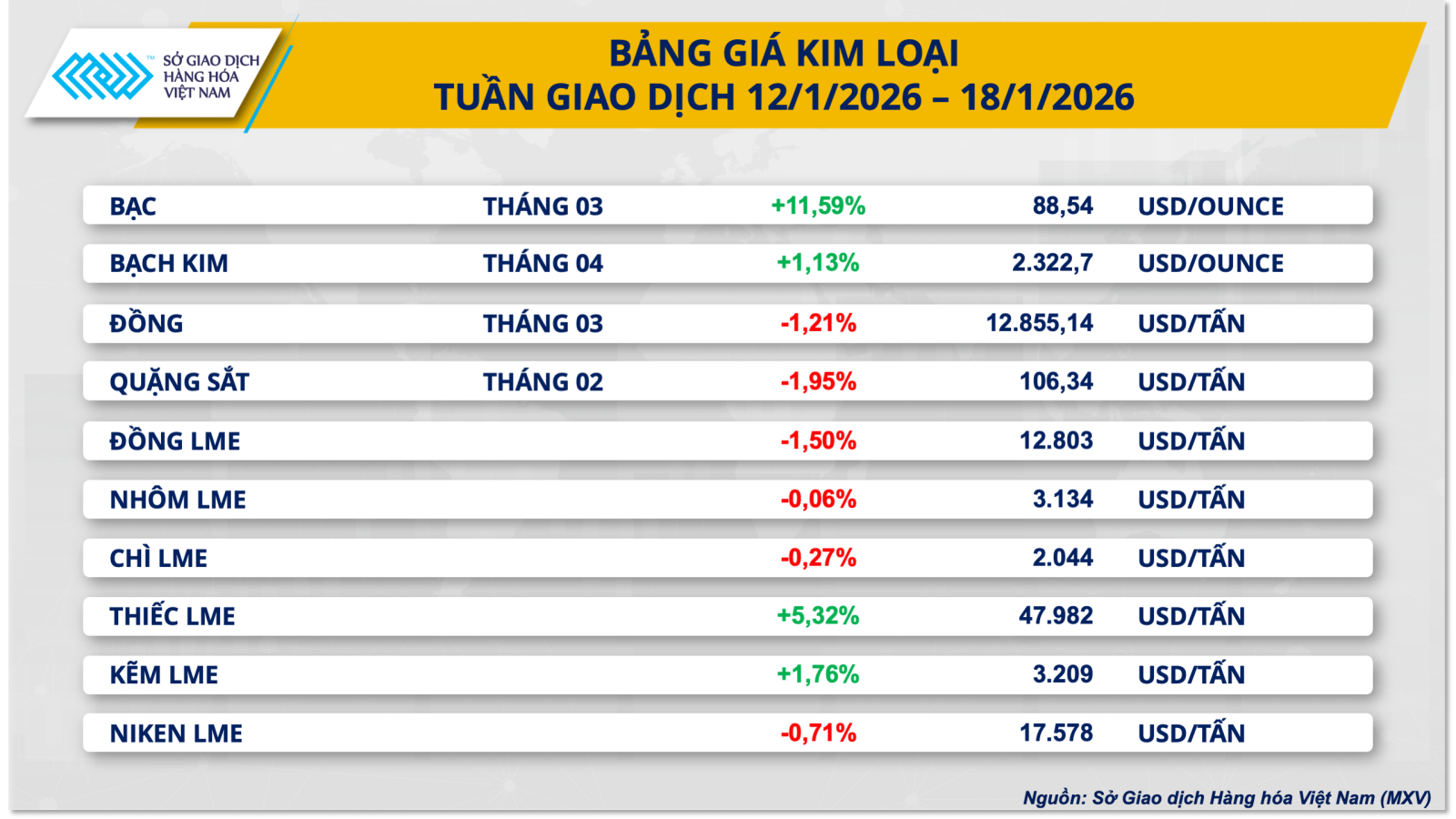

Silver prices have risen sharply, but investors are becoming more cautious.

Concluding the past trading week, the metals market witnessed a clear divergence among commodities within the group. Silver, in particular, became the focal point, maintaining strong upward momentum for most of the week. COMEX silver prices rose consecutively in the first four trading sessions of the week, surpassing the $92/ounce mark on January 15th – the highest level in many years.

However, profit-taking pressure emerged towards the end of the week, coupled with a cooling of geopolitical risk factors, causing silver prices to correct downwards by more than 4% in the final trading session. Closing the week, COMEX silver prices settled at $88.54 per ounce, representing an increase of nearly 11.6% compared to the end of the previous week.

According to the Vietnam Commodity Exchange (MXV), the strong surge in silver prices last week was the result of a confluence of factors. From the beginning of the week, capital flows tended towards safe-haven assets like precious metals as the market increased concerns about uncertainties related to US monetary policy. Legal developments surrounding the Chairman of the Federal Reserve (Fed) partly raised questions about political pressure on policy direction, thereby fueling defensive sentiment in the financial markets.

Furthermore, newly released economic data shows that inflation in the US is showing signs of cooling down, reinforcing expectations that the Fed may continue to ease monetary policy in the near future. According to the US Bureau of Labor Statistics (BLS), the Consumer Price Index (CPI) for December 2025 increased by 2.7% year-on-year, the core CPI increased by 2.6%, while the Producer Price Index (PPI) for November increased by 0.2%, all in line with market forecasts. In this context, analysts believe that some of the increased costs from import tariffs are being proactively absorbed by US businesses, thereby preventing inflationary pressure from rising too sharply. This is seen as a favorable environment for non-yielding assets such as precious metals.

Besides macroeconomic factors, geopolitical tensions related to US-Iran relations last week also contributed to triggering safe-haven demand, supporting the upward trend in silver prices. At the same time, demand for strategic minerals for energy transition continued to act as a long-term support for the metals market. However, towards the end of the week, as geopolitical risks showed signs of easing and the US signaled that it would not temporarily implement new tariffs on strategic minerals, the market gradually regained its balance.

Notably, data from the U.S. Commodity Futures Trading Commission (CFTC) shows that in the week ending January 13, the net long position of managed money in COMEX silver contracts fell to 13,792 contracts – the lowest level since the end of February 2024. This suggests that the recent surge in silver prices was primarily driven by safe-haven and physical market demand, rather than a strong expansion of speculative money flows.

Domestically, due to its heavy reliance on imports, the price of 999 silver continues to closely follow global trends. As of January 18th, the price of 999 silver in Hanoi was listed at 2.899 - 2.929 million VND/ounce (buying price - selling price), while in Ho Chi Minh City, the price fluctuated around 2.901 - 2.935 million VND/ounce, an increase of over 12% compared to the end of the previous week.

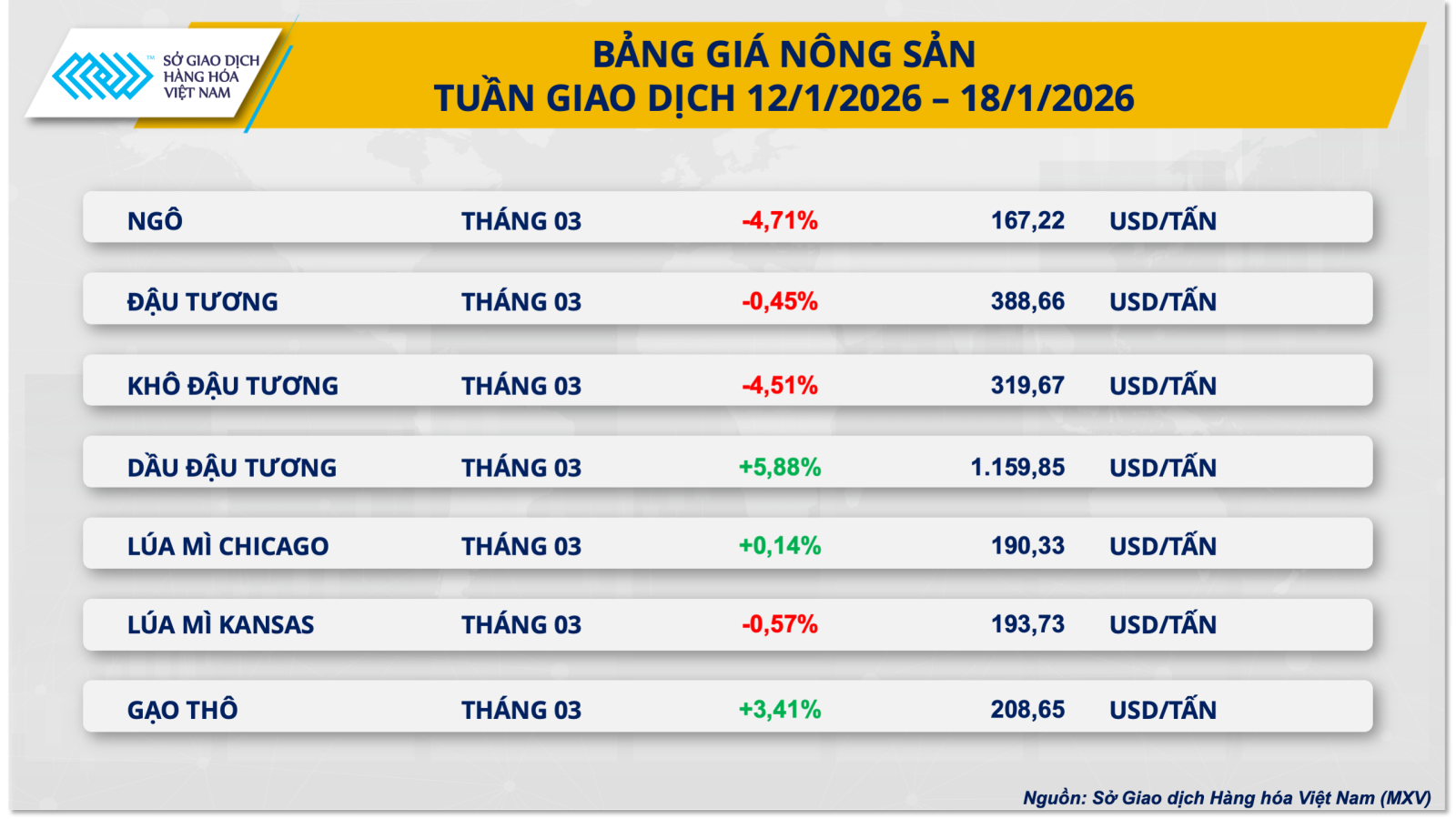

Corn prices plummeted by more than 4.7%.

Conversely, the agricultural market witnessed a return of selling pressure across most key commodities. Notably, world corn prices fell by more than 4.7% this week, to $167.2 per ton.

Pressure on the corn market emerged early this week after the U.S. Department of Agriculture (USDA) released its January World Agricultural Supply and Demand Report (WASDE). In that report, the USDA unexpectedly raised its forecast for U.S. corn production in the 2025-2026 crop year to a record 432.3 million tons, a 1.6% increase from the previous month's report, thanks to upward adjustments in both yield and harvested acreage. This move pushed ending corn inventories in the U.S. to their highest level in nine years.

Globally, the USDA also adjusted ending corn inventories upwards by 11 million tons, to approximately 291 million tons, indicating a growing oversupply situation. Furthermore, China's corn production exceeding 300 million tons added to market pessimism, driving corn prices down sharply at the start of the week.

Following the shock from the WASDE report, corn prices briefly recovered mid-week thanks to positive signals from the energy sector. According to the U.S. Energy Information Agency (EIA), ethanol production in the week ending January 9th reached a record high, reflecting increased demand for corn in biofuel production. However, this recovery quickly weakened as supply reports continued to send negative signals.

Specifically, the International Grains Council (IGC), in its January 2026 report, raised its forecast for global corn production in the 2025-2026 season to approximately 1.31 billion tons, significantly higher than previous estimates, mainly due to favorable harvests in the US and China. At the same time, the Rosario Grains Exchange (BCR) also raised its forecast for Argentine corn production to a record 62 million tons, despite dry weather conditions. These data further reinforce the outlook for abundant supply, maintaining downward price pressure on the corn market in the short term.

Source: https://baotintuc.vn/thi-truong-tien-te/gia-bac-lap-dinh-ky-luc-mxvindex-cham-2516-diem-20260119091426005.htm

![[Photo] Hue: Admire the 2.4 trillion VND sea bridge, the longest in Central Vietnam.](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2026/05/24/1779614018347_anh-man-hinh-2026-05-24-luc-16-13-29.png)

Comment (0)