Opening the trading session on the morning of June 23rd, the VN-Index continued its upward trend, quickly surpassing the 1,880-point mark thanks to the impetus from Vingroup's group of stocks. Although VIC and VHM did not experience the same strong gains as the previous session, the sustained increases in these stocks were still enough to support the market and push the index upwards.

However, as the Vingroup group's performance slowed down, the market began to show clearer divergence on the electronic board. Consequently, the upward momentum of the VN-Index narrowed significantly, and after more than an hour of trading, the index had fallen below the 1,870 point mark.

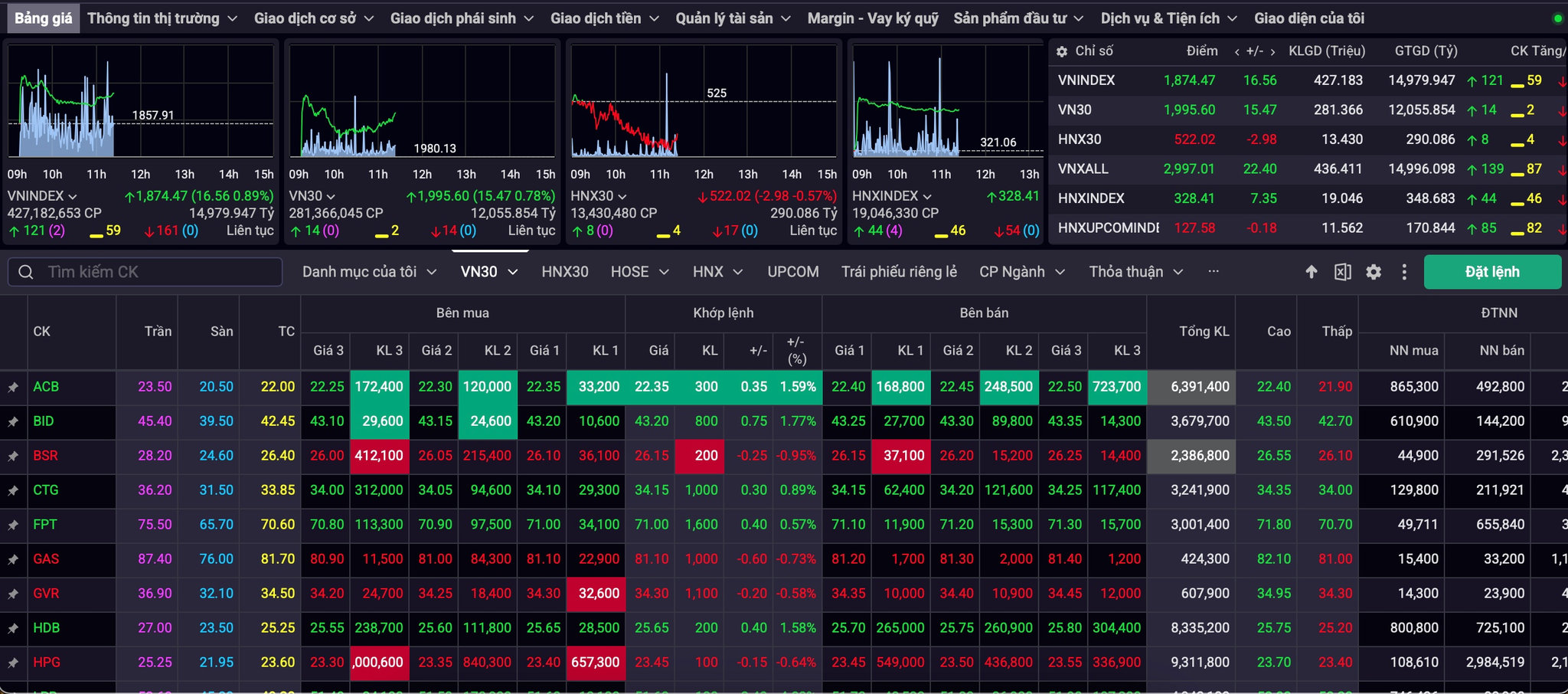

Amidst a lack of standout performances across most sectors, some securities stocks traded more positively than the average.

Specifically, CTS, BSI, and ORS all increased by over 3%, while TVS surged to its ceiling price of 13,800 VND. Notably, ORS ranked second in the entire market in terms of liquidity with a trading volume of over 8 million units.

In the real estate sector, VHM (+1.87%), VIC (+2.82%), NVL (-2.7%), VRE (-1.14%), KDH (-1.78%), TCH (-1%) and CEO (-1.95%).

Meanwhile, green spread across the banking sector withSHB (+0.73%), TCB (+3.88%), HDB (+1.98%), ACB (+2.5%), STB (+2.25%), VCB (+0.98%), and CTG (+1.03%). Similarly, the financial services sector saw gains with VIX (+0.29%), VND (+1.11%), ORS (+3.45%), SHS (+0.52%), and HCM (+0.18%).

At the close of this morning's trading session, the VN-Index rose 20.23 points to 1,878.14 points (+1.09%) compared to the previous session. Similarly, the HNX-Index increased by 328.62 points (+2.35%), equivalent to 7.56 points. Meanwhile, the UPCo M-Index decreased by 127.52 points (-0.19%), equivalent to 0.24 points.

Market liquidity reached VND 15,658.91 billion, with 451,000 shares traded. Across the sector, 124 stocks increased, 158 decreased, and 60 fell to their reference price.

According to experts at AIS Securities Company, the VN-Index continues to record strong recovery, regaining the important 20-day and 50-day moving averages.

The main support comes from the Vingroup conglomerate, energy, and infrastructure services. Conversely, adjustment pressure and differentiation are present in the technology and finance sectors.

A short-term recovery has officially formed, with the market's next target being the psychological resistance level of 1,900 points. However, it should be noted that capital flows have not yet spread strongly despite the index's rise. This is a cause for concern and caution. Taking advantage of the market's recovery, investors should prioritize holding positions in stocks that are attracting short-term capital flows.

According to experts at SHS Securities Company, the VN-Index is breaking above the downward trend under the strong influence of large-cap stocks. The quality of the market is still improving, opening up new growth prospects with many short-term profit opportunities.

However, liquidity remains quite low, and the potential for exceptional growth is still concentrated in a few leading stocks.

Liquidity has not really improved, possibly partly because the market is entering the end of Q2/2026, a time when investors reassess their portfolios after the first six months of 2026, update fundamental factors and business results to plan portfolio restructuring and evaluate new investment opportunities if any. Investors may consider investment opportunities in leading companies in growth sectors.

Source: https://baonghean.vn/vn-index-tang-hon-20-diem-trong-sang-23-6-10341662.html

![[Photo] Prime Minister Le Minh Hung presides over the thematic session on promoting science and technology development and innovation.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/06/23/1782207872934_ndo_br_dsc-1724-jpg.webp)

![[Image] Paris's oldest bridge goes viral after transforming into a giant cave.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/06/24/1782283441197_ndo_br_dsc05314-jpg.webp)