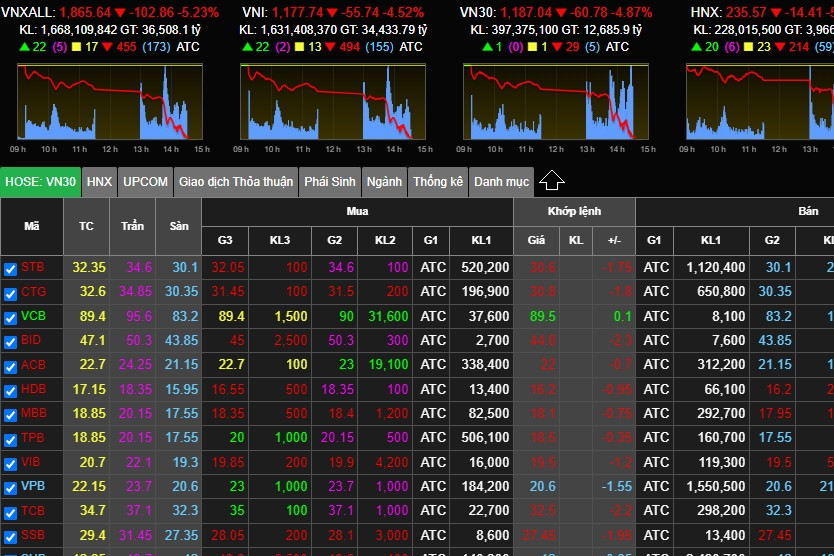

So what's happening to the stock market when domestic investors are selling off at any price, causing thousands of stocks to plummet, including 275 that hit the floor limit, while foreign investors are turning around and buying heavily again?

PV VietNamNet had a discussion with Mr. Vicente Nguyen, Chief Investment Officer (CIO) of AFC Vietnam Fund, about the rare price drop associated with several new records, as well as the outlook for capital flows and the Vietnamese stock market.

Taking profits + weak psychology leading to panic

- The stock market just experienced a sharp decline on August 18th, with the VN-Index falling 55.5 points, equivalent to a 4.5% drop. This was a rare and significant loss in recent years. In your opinion, what led to such a strong sell-off?

Mr. Vicente Nguyen: Profit-taking is one of the main reasons, and after many brokers took profits, they urged clients to sell off their shares. The weak sentiment, coupled with the market sentiment, led to the sell-off on the afternoon of August 18th. Fundamentally or economically , there's nothing new about it.

Specifically, which group of stocks/stock codes dominated this sharp decline?

With over 270 stocks hitting their lower limit, almost every sector experienced equally sharp declines. However, a closer look reveals that the real estate sector is likely the most affected, as this group has recently attracted significant speculative capital and surged despite sluggish business performance.

- Did any margin calls occur during the session, or is there a possibility of them occurring in subsequent sessions, sir?

The market has only fallen 4.5%, which isn't enough to trigger a widespread margin call, but it could affect a few specific stocks that have already fallen significantly. A further 5-7% drop in subsequent sessions might be the only way to trigger a widespread margin call.

- Liquidity in the August 18th trading session reached 42,000 billion VND (approximately 1.75 billion USD), nearly double the recent average per session. This is a very large number. How do you explain this sudden surge in liquidity?

That's how the market works; there are buyers and sellers. When sellers panic and sell at any price, there are also buyers willing to purchase good stocks at low prices. At that point, liquidity increases rapidly.

For example, in such sell-off situations, most of the sellers are individual investors and the buyers are institutions, both domestic and foreign. Therefore, high liquidity is normal.

VinFast is a good sign.

- VinFast's listing on the US stock market brought a positive boost to the "Vin" group of stocks. However, VinFast shares have since experienced a sharp decline. How do you assess the VFS listing on the US market and its impact on the domestic market?

The listing of VFS is a very positive sign for Vingroup Group and for Vietnam's financial and economic landscape. For Vingroup, this event increases access to international capital markets, thereby enhancing opportunities to raise capital.

Because VFS chose to list through a SPAC rather than a traditional IPO.

For Vietnam's economy and finance, this event has a huge promotional impact. Many investors will learn about Vietnam and its economy.

Furthermore, this listing also creates a significant impetus for other Vietnamese businesses that want to list or raise international capital.

- What do you think about VinFast's share price at the close of trading on August 17th - around $20 per share, equivalent to a market capitalization of $46 billion?

Whether a valuation is high or low depends on each investor's perspective and approach. Based solely on profits and the current situation, this valuation might be excessively high, but considering VFS's prospects and potential, it could be considered average or only slightly overvalued.

However, the electric vehicle (EV) sector is a completely new industry, even globally. The number of profitable companies in this field is currently very small. Therefore, VFS's losses are normal. Most importantly, the product must be good, trusted, and favored by customers; then the future and prospects remain bright, because EVs seem to be the global trend.

- Was the downward fluctuation in VinFast's share price a negative factor contributing to Vingroup's share price (which hit the floor limit) on August 18th?

In this respect, that's true. Because what goes up also comes down. Domestic investors often assume that VFS is valued at $85 billion, and Vingroup owns 51%, which is over $42 billion. Therefore, VIC must also be valued at over $42 billion, not including Vinhomes or Vincom Retail…

Therefore, it's understandable that when VFS's value decreases, VIC's valuation also decreases accordingly. From the perspective of an investment fund like ours, however, they aren't very related. Other funds may have a different view.

- How do you assess the news that Evergrande, China's second-largest real estate developer, has filed for bankruptcy protection in the US? How will this affect the Vietnamese real estate and financial markets, and investor sentiment?

This would be a significant blow to China's real estate industry, leading to long-term distrust and a major impact on the Chinese economy. However, this bankruptcy was anticipated, and its effects have already occurred, so the declaration of bankruptcy is merely a formality, thus reducing the overall impact. In the short term, there will be an impact on Vietnam, but not related to its financial situation, but rather its economy. The impact of this Chinese real estate crisis will significantly reduce purchasing power in China, thereby decreasing the demand for imported goods from Vietnam. This is an indirect impact.

- So what are the prospects for real estate stocks after the news from China's Evergrande?

Information about China's Evergrande has a negative psychological impact on Vietnam's real estate market, but it's not fundamentally related. However, Circular 06 (from the State Bank of Vietnam on lending activities) will significantly impact many existing real estate businesses, as many are raising capital from customers through investment cooperation contracts or business capital contribution contracts for projects that do not meet the conditions for sale.

However, it helps legitimate businesses with sound legal standing to increase their market share and customer base. Therefore, real estate companies that are inherently financially weak and have poor legal standing will likely fall into a long period of dormancy if they raise capital through this method. Personally, I believe this is a necessary cleansing process for the market.

Businesses with strong finances, clean projects, and sound legal standing will remain stable, sell their products, and secure loans for customers, thus overcoming the difficulties.

Meanwhile, many businesses will go into hibernation or go bankrupt. Then the market will gradually recover, and strong businesses will rise to the top. But I think this will happen in 2025-2026; 2024 will still be very difficult.

"The crash on August 18th was more of an opportunity than a risk."

- How do you assess the banking sector/stocks?

The difficulties stemming from rising bad debts will be overcome because the banking sector is the backbone of the economy. The government will certainly provide support. That's regarding the business situation; as for stocks, in the long term, bank stocks remain very promising because the economy is certain to experience strong and sustained growth.

Therefore, the banking sector is sure to grow. Currently, this group is extremely attractively valued with a P/E ratio of just under 10 times and a P/B ratio around 1 time. However, this will only be suitable for institutional investors with larger capital; I believe individual investors lack the patience to hold a stock for 3-5 years. They would rather lose their entire investment than wait that long.

- With deposit interest rates currently very low, what are your prospects for capital inflow into the stock market in the near future?

Low interest rates will stimulate investment in the stock market. Therefore, in this environment, the flow of money will increase sharply. As we saw on August 18th, the trading volume reached over $1.5 billion. If interest rates remain low, the flow of money will continue to pour into the stock market.

Personally, I believe the stock market is in a long-term uptrend, at least for the next 5 years. Therefore, crashes like the one on August 18th are more of an opportunity than a risk. If you choose the right company and patiently wait, you will make big profits in the next 5 years; I'm almost certain of that.

- The USD/VND exchange rate has recently risen sharply, exceeding 24,000 VND/USD. How will this impact foreign institutional investment (FII) flows and the stock market, and what is your forecast for the exchange rate from now until the end of the year?

If the exchange rate rises too sharply, foreign investors will certainly hesitate to disburse funds, especially new investors. This affects not only indirect but also direct (FDI) investors. However, it also has some positive impacts, such as stimulating exports better, as export businesses will benefit greatly from a rising exchange rate.

Personally, I believe the US dollar will continue to appreciate for the remainder of the year, as the Federal Reserve (Fed) appears likely to raise interest rates one more time and keep them at a high level.

Currently, there are no signs that the Fed will cut interest rates anytime soon. Conversely, the State Bank of Vietnam is urging commercial banks to lower lending rates, and even deposit rates, which widens the interest rate differential between VND and USD. Therefore, the exchange rate trend remains upward from now until the end of the year. Extreme caution is needed regarding this.

The economy is improving:

Commenting on the economic outlook for the end of the year, Mr. Vicente Nguyen believes that "growth will be better and stronger than in the first half of the year," because the most difficult period has passed, US interest rates have peaked, while inflation is gradually returning to normal levels. Therefore, exports will gradually improve, and industrial production will also improve significantly in the second half of 2023. This year's GDP is expected to be around 5-5.5% due to the government's active increase in public investment.

However, according to him, credit growth will remain low because businesses are hesitant to borrow and interest rates are still high.

"The economies of the US, Europe, and China will improve in the second half of 2023. However, it won't be significantly better because, while they've essentially passed the worst period, they are still weak, not recovering strongly. This will certainly affect Vietnam; exports and investment will gradually increase, but they haven't yet become robust," said Vicente Nguyen.

However, commenting on the long-term prospects of the Vietnamese economy and stock market over the next few years, he optimistically stated that they are "as bright as a full moon."

The reason is that a series of favorable agreements, capital flows shifting from China to Vietnam, and the restructuring and diversification of supply sources by European and American businesses will be a major driving force for the Vietnamese economy. Therefore, the stock market will perform well.

Source

![[Photo] Prime Minister Pham Minh Chinh presides over a meeting to assess the situation during the Lunar New Year holiday.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/02/22/1771768925196_ndo_br_dsc-6283-jpg.webp)

Comment (0)