With tight supply, global coffee prices continue to rise.

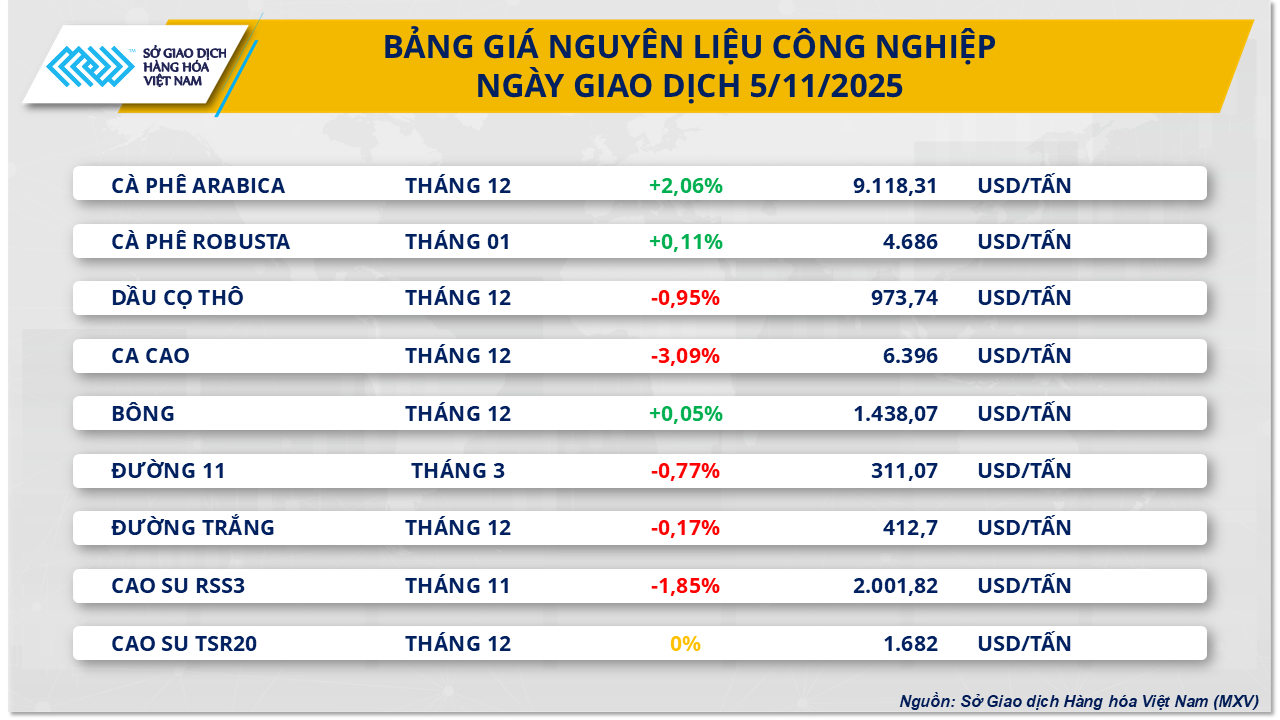

At the close of yesterday's trading session, the industrial raw materials market saw relatively mixed developments. Notably, the supply shortage continued to push coffee prices higher. Specifically, Arabica coffee prices increased by more than 2% to $9,118 per ton – nearing their highest level since mid-October; while Robusta coffee prices also increased by 0.1% to $4,686 per ton.

According to the Vietnam Commodity Exchange (MXV), concerns about supply shortages in Brazil continue to be a key factor supporting coffee prices on the international market. The Brazilian National Supply Agency (Conab) recently released a forecast indicating that Brazil's coffee production for the 2025-2026 crop year is estimated at only 55.2 million bags, a decrease of nearly 2% compared to the previous year. Of this, Robusta production is expected to reach a record 20.1 million bags, but Arabica production – Brazil's main coffee variety – is projected to decrease by more than 11%, to below 35.2 million bags. The cause is attributed to unfavorable weather conditions and the "biennial" growth cycle of coffee plants, which often leads to a significant drop in yield after the peak season.

Besides production factors, supply on the ICE exchange is also tightening. Monitored Arabica inventories are continuously decreasing, currently standing at only around 22,000 bags – a record low in many years.

In key growing regions, production continues to face numerous obstacles. In Brazil, the heatwave in early October caused scorching and shedding of flower buds, posing a serious risk to the 2026-2027 crop. Meanwhile, in the Central Highlands, prolonged heavy rains during the harvest period have significantly hampered progress. Typhoon Kalmaegi, with wind speeds of level 13-14 and gusts up to level 17, is forecast to make landfall in the area on November 7th, bringing very heavy rainfall. Meteorological forecasts indicate Gia Lai could receive an additional 212.5 mm of rain, while Dak Lak is expected to experience an additional 139 mm over the next 15 days, further increasing already high humidity levels in the growing regions.

In the domestic market, coffee trading remains sluggish, although stable purchasing activity is still being recorded from some warehouses in the Buon Ma Thuot area. Large businesses continue to purchase regularly, while some warehouses are temporarily staying out of the market or only choosing to buy from distant locations.

On November 5th, the price of coffee purchased for delivery to Buon Ma Thuot fluctuated between 119,000 and 119,500 VND/kg. Units with quality certifications were willing to raise prices to 120,000 - 120,500 VND/kg. In Gia Lai , large warehouses focused on purchasing goods for delivery to Binh Duong at a price approximately 1,000 VND/kg higher than the general market price, accompanied by strict requirements on raw material quality. The current purchase price at warehouses is around 120,000 VND/kg for delivery to Binh Duong, while goods delivered to Pleiku ranged from 119,000 to 119,500 VND/kg depending on the standards.

Supply in Gia Lai is gradually stabilizing as the harvest enters its main phase. It is expected that in the next 2-3 weeks, new supply will become clearer and more consistent, contributing to improved liquidity in the market.

The prospect of oversupply continues to weigh on oil prices.

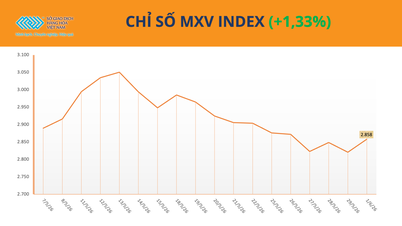

Conversely, according to MXV, the energy market was deeply in the red yesterday. World oil prices continued to face downward pressure due to the increasingly clear prospect of a global oversupply, especially after the latest report from the US Energy Information Agency (EIA). At the close of trading on November 5th, WTI oil prices once again fell below $60/barrel, recording a decrease of approximately 1.6% and settling at $59.6/barrel; while Brent oil prices also returned to $63.5/barrel, corresponding to a decrease of approximately 1.3%.

Data from the EIA shows that commercial crude oil inventories in the US rose by more than 5 million barrels in the last week of October, the sharpest increase since July. The American Petroleum Institute (API) also reported similar results, estimating inventories at 6.5 million barrels – significantly higher than market forecasts.

According to Kpler's chief analyst Matt Smith, "The recovery in imports coupled with a slowdown in refining activity as refineries undergo routine maintenance" is driving the trend. In the week ending October 31, the U.S. imported an average of 5.9 million barrels of oil per day, an increase of nearly 900,000 barrels from the previous week.

The above information further reinforces the prospect of global oversupply, which had been predicted beforehand due to the potential increase in supply not only from OPEC+ but also from American countries, including Canada. In its newly released budget plan, Ottawa plans to eliminate emissions regulations in oil and gas extraction, which could lead to an increase in supply from this North American nation.

Over the past week, world oil prices have fallen by approximately 1.5-2%. However, this fluctuation has not been uniformly reflected across refined petroleum product exchanges. On the SGX (Singapore) exchange, RON92 and RON95 gasoline prices decreased by nearly 2%, while the price of other oil products increased by 2.5-3%. This divergence is expected to directly impact the domestic retail gasoline and diesel price adjustment by the Ministry of Industry and Trade - Ministry of Finance, scheduled to be announced this afternoon.

Source: https://baotintuc.vn/thi-truong-tien-te/gia-ca-phe-tang-manh-dau-wti-roi-khoi-60-usdthung-20251106095536844.htm

![[Photo] General Secretary and President To Lam presides over a meeting with the Central Organizing Committee.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/06/03/1780482764658_a1-bnd-4741-3342-jpg.webp)

![[Photo] Secretary of the National Assembly Party Committee, Chairman of the National Assembly presides over the meeting of the Standing Committee and Executive Committee of the National Assembly Party Committee.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/06/03/1780480353201_ndo_br_bnd-2585-jpg.webp)

![[Photo] First session of the 14th Congress of the Vietnam Trade Union](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/06/03/1780465947883_ndo_br_img-3852-jpg.webp)

![[Video] Sunset at Lap An Lagoon – Where the sun sets over the fishing nets](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/05/31/1780192137701_beach-landscape-sea-water-nature-grass-745871-pxhere-com.jpeg)

Comment (0)