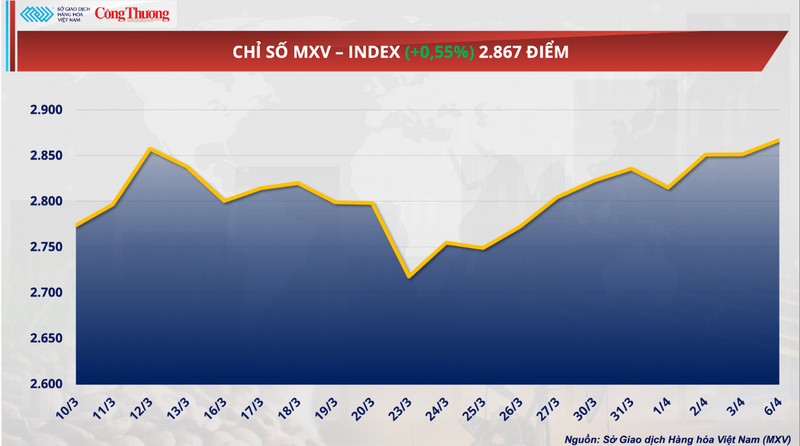

Despite many major exchanges being closed for Easter, leading to reduced liquidity, the global commodity market closed in positive territory on April 6th. Buying pressure towards the end of the session helped the MXV-Index rise 0.55% to 2,867 points. However, the start of the week showed a clear divergence, particularly between industrial raw materials and agricultural products.

MXV-Index

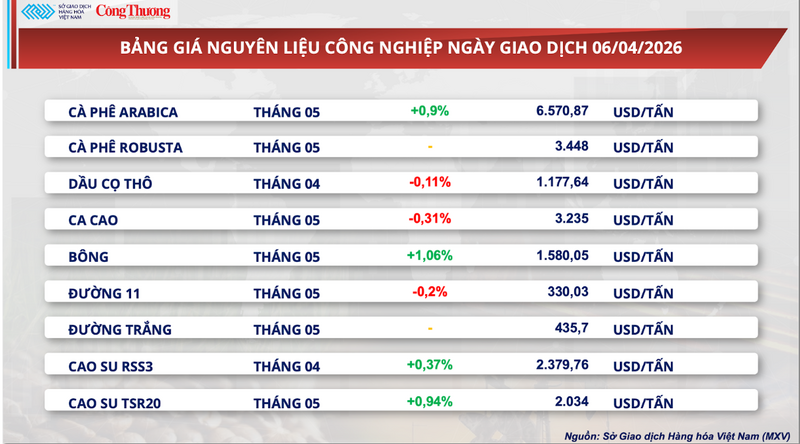

Cocoa prices plummet...to rock bottom.

According to the Vietnam Commodity Exchange (MXV), the cocoa market continued to fluctuate within a narrow range during yesterday's trading session. At closing, the May cocoa futures contract fell 0.31%, to $3,235 per ton, remaining near its lowest price in a year.

Industrial raw material price list

MXV stated that the biggest pressure continues to come from inventory. According to data from ICE, the amount of certified cocoa is maintaining its upward trend and reached 2.36 million bags as of March 31st - the highest level in over eight months. This development indicates that a short-term oversupply situation is gradually forming, especially given that the flow of physical goods is no longer as disrupted as before.

Regarding supply, the outlook in West Africa – the world's major cocoa producing region – is clearly improving. In Ivory Coast, rainfall this past week has been above average, reinforcing expectations for a stable and potentially better-than-expected mid-crop harvest from March to August. Favorable weather conditions are becoming a key factor in mitigating supply risks – a major driver of the sharp increase in cocoa prices in 2024.

Meanwhile, demand is showing clearer signs of weakening. Easter – the peak period for global chocolate consumption this year – is projected to be less favorable. According to Bloomberg Intelligence, retail sales during this period could fall by about 5% compared to the same period last year, reflecting consumers beginning to adjust their shopping habits after a prolonged period of high chocolate prices.

The next market focus will be the Q1 cocoa crushing figures for Europe and North America, expected to be released on April 16th. This is considered a crucial indicator for assessing the actual demand in the processing industry and confirming the market's "absorption" level after a period of historically high prices.

Conversely, several factors are still somewhat restraining the decline. Specifically, the pace of cocoa deliveries to ports in Ivory Coast is showing signs of slowing down. Cumulatively from the beginning of the crop year (October 1, 2025 - March 29, 2026), the amount of cocoa arriving at ports reached 1.43 million tons, a slight decrease of 0.7% compared to 1.44 million tons in the same period last year. This indicates that the actual supply has not yet fully exploded immediately.

Furthermore, policy adjustments in the world's two largest producing countries are creating additional long-term variables. Ghana has reduced procurement prices by nearly 30% for the 2025-2026 crop year, while Ivory Coast has cut farmer payments by as much as 57% as early as the mid-harvest season. With these two countries accounting for over 50% of global production, reduced farmer incomes could impact investment incentives in subsequent crop years, potentially leading to supply constraints in the medium and long term.

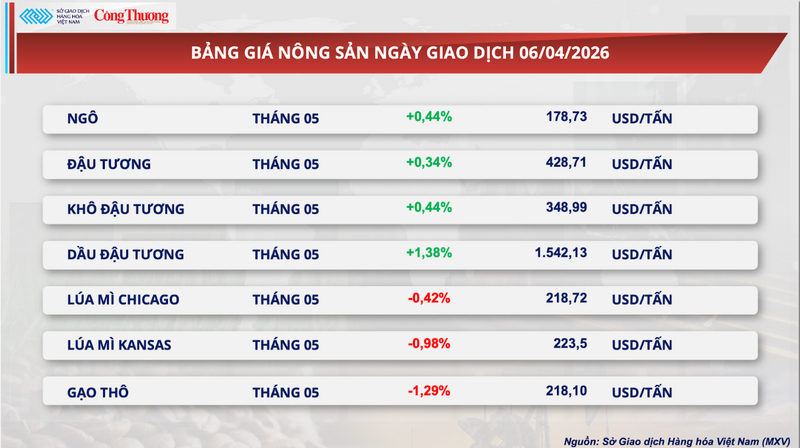

Funds significantly increase net long positions, soybean oil conquers new highs.

In contrast to the performance of cocoa, the soybean market recorded positive gains at the start of the week, clearly led by soybean oil.

Specifically, the May soybean futures contract on the CBOT rose 0.34% to $428.7 per ton. Meanwhile, soybean oil surged 1.38%, closing at $1,542.13 per ton, setting an all-time high.

Agricultural product price list

The price increase is driven by a confluence of factors, most notably better-than-expected export data. According to the US Department of Agriculture (USDA), the volume of soybean exports inspected last week reached over 779,300 tons, significantly higher than market forecasts. Notably, China accounted for nearly 70% of the total volume, indicating that import demand remains high and plays a pivotal role.

Furthermore, demand from the renewable energy sector continues to be a crucial supporting factor. Domestic oil crushing operations in the US are operating at their highest efficiency in 3.5 years, with estimated profit margins of around $110 per ton. This not only bolsters raw material demand but also attracts speculative capital back into the market.

Position data shows a significant increase in cash flow. Total net long positions across the entire soybean portfolio have exceeded 449,000 contracts. Specifically for soybean oil, investment funds are holding the largest net long positions in history. The market is currently pricing in expectations that vegetable oil will account for a record 52.5% of the value share in the biodiesel and renewable diesel production chain.

In addition, geopolitical factors, particularly tensions in the Strait of Hormuz, are also indirectly supporting prices through expectations of disruptions to the global energy supply chain.

Domestically, soybean meal prices continued to remain stable for near-term maturities but began to show a downward trend for longer-term maturities, reflecting expectations of more abundant supply in the coming months.

Specifically, at southern ports, the quoted price for spot and April futures remained at 13,400 VND/kg. Meanwhile, in the North, prices for April and May futures fluctuated between 13,200 and 13,500 VND/kg, maintaining a slight difference compared to the South.

On the import market, CNF prices for South American soybean meal showed a clear downward trend in the first trading sessions of April. With a reference exchange rate of 26,362 VND/USD, the flat price for shipments delivered between April 15th and May 15th was 77 USD/ton. However, for shipments in June and July, prices dropped sharply to 59-60 USD/ton.

A similar trend was observed in Basis prices, with mid-year shipments retreating to the 59-60 USD/ton range. Simultaneously, the price difference between the two regions continued, with the North typically being about 5 USD/ton higher than the South, reflecting differences in logistics costs and port location.

Price list for some other types of goods

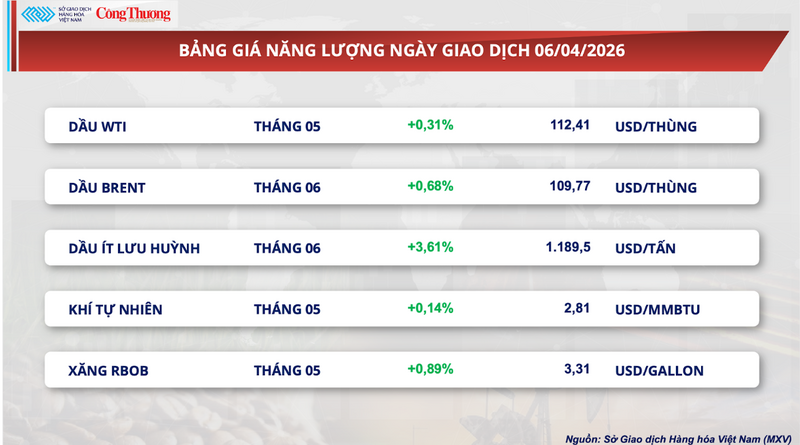

Energy price list

Metal price list

Source: https://congthuong.vn/gia-ca-cao-giam-ky-luc-450729.html

![[Image] Hanoi's urban life under the challenge of a "scorching hot" environment](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/05/25/1779706979265_nang-nong-t5-2026-minh-duy-7-4636-jpg.webp)

![[Image] Close-up view of the interchange connecting the two expressways and Long Thanh Airport.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/05/25/1779703378210_ndo_br_z7863716673926-224453a31600126cce10622af6290afd-4549-jpg.webp)

Comment (0)