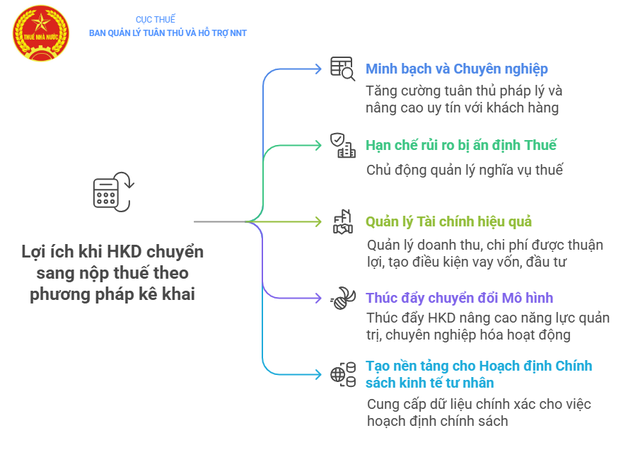

5 benefits when business households pay taxes by declaration method

The shift from the contract method to the declaration method is an inevitable step for household businesses to develop more sustainably, access credit, supply chains, and formal business opportunities.

Firstly, it increases transparency and professionalism. Switching to tax payment by declaration method helps business households operate more transparently and professionally. Business households will declare taxes monthly or quarterly based on clear accounting books, invoices and documents. This helps to record revenue and expenses accurately, in compliance with accounting and tax laws.

At the same time, the use of electronic invoices when switching to the declaration method also brings many benefits, such as helping to increase credibility with customers in the modern business environment, contributing to limiting risks related to law as well as in tax management.

Second, limit the risk of being taxed. Business households are in a proactive position in paying taxes when they are proactive in self-declaring and self-determining the amount of tax payable, which is not affected by the previous year's revenue and the fixed amount determined by the tax authority. If during the year, the business household encounters difficulties due to the market, it can declare according to the actual situation without being taxed as before.

Third, full accounting helps businesses easily demonstrate revenue, expenses and profits clearly to banks or partners. As a result, the process of borrowing capital or mobilizing additional investment sources becomes more convenient. At the same time, compliance with accounting requirements also creates favorable conditions for branch expansion or finding and cooperating with new business partners.

Fourth, it helps to promote business households to change their models. Switching to methods of declaring revenue, using invoices, managing cash flow through accounts... is also a form of creating positive pressure for business households to upgrade their management capacity, professionalize their operations, and move towards transforming into formal enterprises. From there, they can access capital, participate in large supply chains, and develop more sustainably.

Fifth, create a foundation for private economic policy making based on real data. When switching to a tax calculation mechanism based on actual revenue declaration and electronic invoices, the management agency will have a clear, comprehensive, accurate and transparent picture of the business activities of this sector. From there, the state will have enough basis to build policies to support and develop the private economy in a substantial way, instead of just relying on estimates, feelings or models lacking input data.

When switching to the declaration method, the contracting household will make adjustments and supplements to the tax declaration.

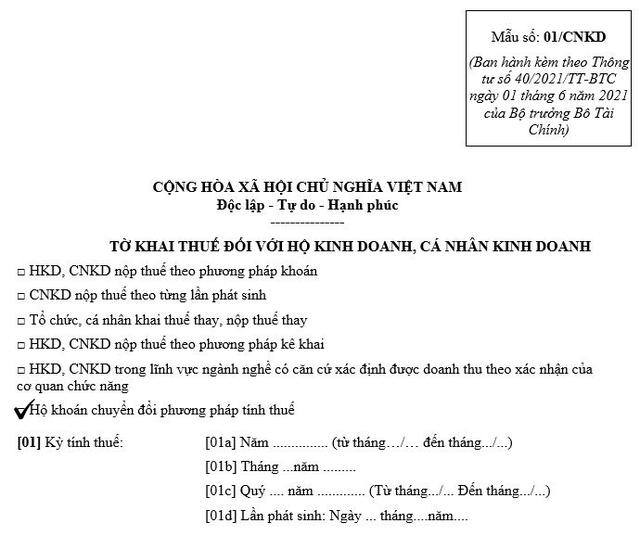

Pursuant to the provisions of Clause 4, Article 3; Point b, Clause 3, Section b6, Point b, Clause 4, Article 13 of Circular No. 40/2021/TT-BTC dated June 1, 2021 of the Ministry of Finance , business households currently paying taxes under the lump-sum method (lump-sum households) are allowed to switch to the declaration method.

Accordingly, when switching to the declaration method, the contracting household will make adjustments and supplements to the lump-sum tax declaration according to Form 01/CNKD issued with Circular 40/2021/TT-BTC of the Ministry of Finance.

On the declaration, the business household must select the item "Household to change tax calculation method" so that the tax authority can use it as a basis to adjust the tax rate for the conversion period. The deadline for submitting the adjusted declaration is no later than the 10th day from the date the business household starts changing the tax calculation method.

Households declare and implement the accounting regime according to the instructions in Circular No. 88/2021/TT-BTC dated October 11, 2021 of the Ministry of Finance. Compliance with regulations helps business households be more proactive in managing production and business activities and fulfilling tax obligations to the State.

What should business households pay attention to when paying taxes by declaration method?

Tax declaration and payment for business households paying taxes by declaration method shall be carried out according to the instructions in Article 11 of Circular No. 40/2021/TT-BTC, specifically as follows:

(1) Regarding tax declaration documents, specified in point 8.2 of Appendix I - List of tax declaration documents issued with Decree No. 126/2020/ND-CP dated October 19, 2020 of the Government, including:

- Tax declaration form No. 01/CNKD according to Circular 40/2021/TT-BTC

- Appendix: List of business activities during the period of business households and business individuals according to form No. 01-2/BK-HDKD according to Circular 40/2021/TT-BTC (if there is a basis to determine revenue according to confirmation of competent authorities, this Appendix is not required to be submitted)

(2) Regarding the form of tax declaration submission,

- Electronic Tax Portal at https://thuedientu.gdt.gov.vn "INDIVIDUAL" subsystem

- National public service portal at https://dichvucong.gov.vn

- In case electronic submission is not possible: submit directly at the one-stop department or via the postal system.

(3) Regarding the place to submit tax declaration documents, according to the provisions of Clause 1, Article 45 of the Law on Tax Administration, it is the Tax Team directly managing the place where business households and individuals conduct production and business activities.

(4) Regarding the deadline for submitting tax declarations, according to regulations in Clause 1, Article 44 of the Law on Tax Administration:

- In case of monthly declaration: no later than the 20th day of the month following the month in which the tax liability arises.

- In case of quarterly declaration: no later than the last day of the first month of the next quarter following the quarter in which the tax liability arises.

(5) Regarding tax payment deadline, according to regulations in Clause 1, Article 55 of the Law on Tax Administration:

- No later than the last day of the tax return submission deadline

- In case of supplementary tax declaration, the tax payment deadline is the deadline for submitting the tax declaration of the tax period containing errors or omissions.

(6) Regarding tax payment method:

- eTax Mobile application.

- Electronic Tax Portal at https://thuedientu.gdt.gov.vn "INDIVIDUAL" subsystem

- National public service portal at https://dichvucong.gov.vn

(7) Tax declaration obligation in case of temporary suspension of operations and business:

- Notify the tax authority as prescribed in Article 91 of Decree No. 01/2021/ND-CP, Article 4 of Decree No. 126/2020/ND-CP, Article 12 of Circular No. 86/2024/TT-BTC

- Tax declarations are not required, except in cases where business households and individual businesses temporarily suspend operations or do not conduct business for a full month if declaring taxes monthly, or temporarily suspend operations or do not conduct business for a full quarter if declaring taxes quarterly.

On March 20, 2025, the Government issued Decree No. 70/2025/ND-CP amending and supplementing Decree No. 123/2020/ND-CP regulating invoices and documents with the regulation that business households paying taxes under the lump-sum method with revenue of 1 billion VND/year or more, from June 1, 2025, must use electronic invoices connected to cash registers.

Decree No. 70/2025/ND-CP is an important step forward to help businesses change their mindset, apply technology to manage work more effectively, optimize processes and profits.

This is also considered a stepping stone towards eliminating lump-sum tax, so that households and business individuals can switch to tax declaration methods from January 1, 2026 according to Resolution No. 198/2025/QH15 on a number of special mechanisms and policies for private economic development of the National Assembly.

Source: https://baobackan.vn/huong-dan-ho-kinh-doanh-nop-thue-theo-phuong-phap-ke-khai-post71415.html

Comment (0)