Business model targeting subprime customers with high risk appetite

The pawnshop sector in the Vietnamese market is currently very fragmented with up to 25,000 stores (estimated by the end of 2024, according to a report by Fiin Group), in which many new generation pawnshop chains have appeared (including the participation of foreign "giants" such as Srisawad).

Although this field in Vietnam is very potential, the barriers to entering the market are not too many, but the difficulty is how to operate and manage the chain of stores effectively. There are even pawnshop chains that are bustling to open a series of new stores but can disappear from the market after only a few years. That is the reason why very few pawnshop chains can expand to the scale of F88 with a system of up to 888 stores nationwide.

|

This is a field with a higher risk appetite than banks or financial companies because the target customers are mostly sub-standard groups (not meeting the criteria of banks) such as freelancers, workers, small traders... At F88, the customer segment is mostly freelancers (accounting for about 70%), this is a group of customers who are "vulnerable", have unstable income and high possibility of bad debt. However, Mr. Phung Anh Tuan emphasized that F88 wants to ensure serving all customer needs so it can accept a higher risk appetite, in return for focusing on building its risk management model.

Sharing his “secret”, Mr. Phung Anh Tuan said that F88 spent the first 5 years of its development journey just to package the formulas for the business model, build a risk management platform, technology, culture and shape the core product, and then start to expand the scale. The business model can be copied but the ability to manage risks when replicating the model is not easy, especially in the lending business, risk management is extremely difficult.

Risk management: the "vital" factor that creates F88's position

Mr. Phung Anh Tuan said that the risk management and credit scoring model must be built based on two core factors: the characteristics of the customer base that it serves and the company's operating procedures. Due to its high risk appetite, F88's risk management model is also different from that of banks and financial companies, especially in asset appraisal, debt collection and bad debt handling.

The biggest strength in F88's risk management model is technology and data information system, which significantly optimizes the appraisal of mortgaged assets. Based on this system, F88 has built and operated a professional asset appraisal process, helping to prevent the risk of overvaluation (leading to losses during liquidation) or undervaluation (causing customers to seek competitors).

The difference of F88 is that it has autonomously built and developed an internal credit scoring system, which is customary and standard for the development orientation of the Company. More importantly, F88 said that it will not stop at the initial scoring step but will continuously monitor risks throughout the loan life cycle to adjust limits and policies to suit the customer's risk level.

|

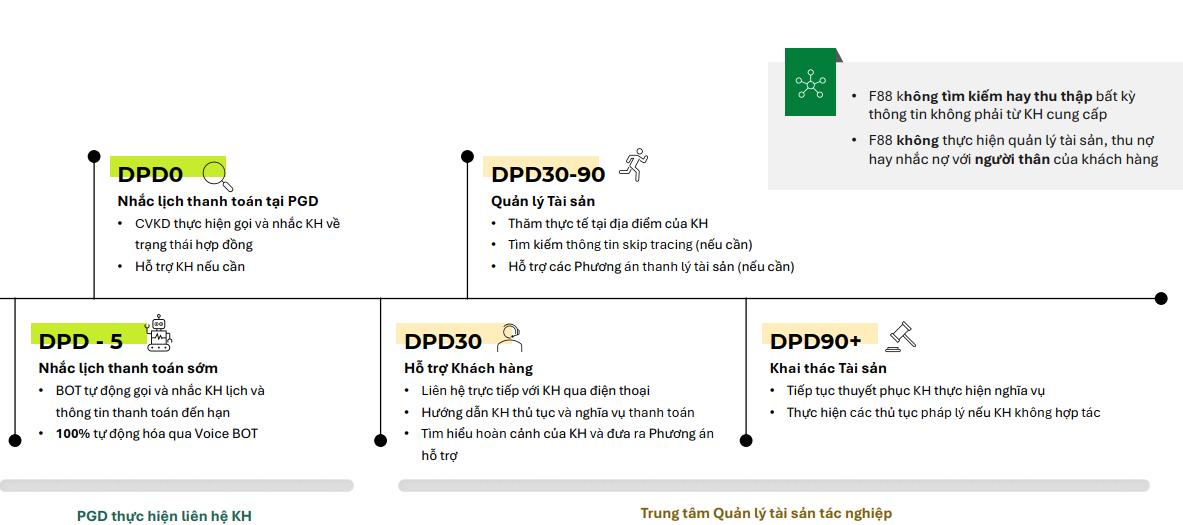

| Debt collection process at F88 |

Technology is also thoroughly applied in F88's debt collection process with stages based on the unpaid due date (DPD), including from reminding early payment 5 days in advance (DPD - 5) to direct debt collection and asset recovery (DPD90+). F88's exclusive technology is to attach GPS tracking devices to collateral assets with the consent of customers, helping to improve efficiency in managing collateral assets.

F88 designs products suitable for loan limits based on the value of collateral and the actual financial capacity of customers (average disbursement limit is about 12 million VND for motorbike registration loans and 146 million VND for car registration loans). Designing product scale suitable for customer segment characteristics is also an important factor affecting F88's debt recovery ability (customers' debt repayment awareness is also higher when the loan amount is small and lower than the asset value, the loan to asset value ratio - LTV at F88 is commonly at 50-80%).

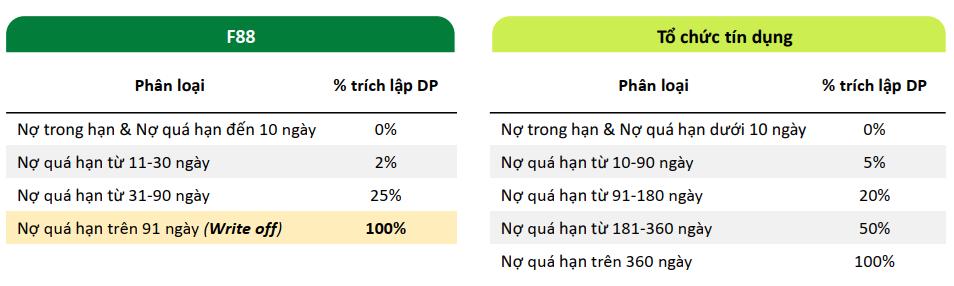

In particular, the risk provisioning at F88 is carried out more cautiously than at credit institutions. The construction of this system is based on advice from foreign markets along with many years of operation in Vietnam. With the characteristic of short-term loans, F88 makes 100% provision for debts overdue for more than 90 days (while credit institutions make 100% provision for debts overdue for more than 360 days). This written-off debt will be handled by provisioning costs and transferred off-balance sheet for monitoring and debt collection policy by the Asset Management Center (recorded in business results if debt collection is successful).

|

| F88's provisioning ratio compared to credit institutions |

In 2025, F88's risk ratio will be the lowest ever.

F88 was established in 2013, followed by the first 5 years to package the formulas for the business model, 2028 marked the development milestone of the Company when it converted from traditional operations to a new model (vehicle registration loan). Ms. Tran Mai Thao - CFO F88 shared that after changing the model, from 2018 to now, F88's business activities have grown remarkably with a compound annual growth rate (CAGR) of net loan balance reaching 77% and revenue reaching 79%. This result is thanks to the strategy of adjusting the product portfolio and especially the credit risk management policy.

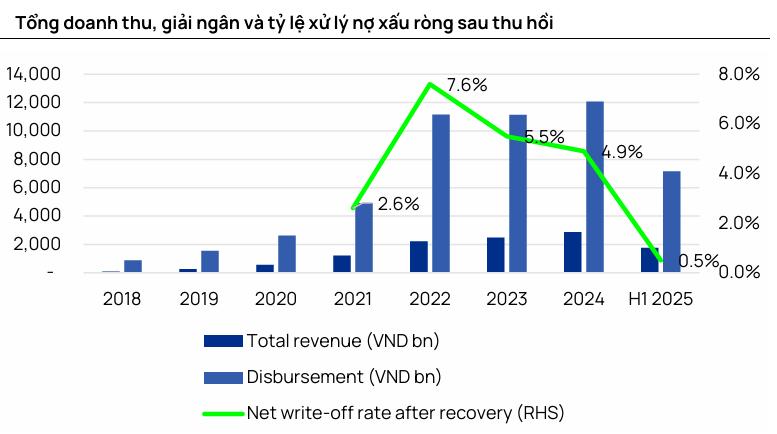

According to Vietcap Securities Company's report, the bad debt ratio on outstanding debt of pawnshop businesses is high at 10-20% (industry average is about 14%) while at consumer finance companies it is 5-10% and commercial banks 1-5%. However, F88 does not monitor the bad debt ratio like credit institutions but based on the write-off rate (because loans overdue for more than 90 days have been written off and monitored off-balance sheet). In addition, due to the specific characteristics of the business model, loans at F88 have short terms, so businesses often measure asset quality based on the loan amount disbursed (assuming a loan of 10 million VND with a term of 4 months, continuously rotating for 12 months, the loan disbursement amount is 30 million VND).

Based on this calculation, F88's net bad debt ratio after recovery has decreased significantly from 7.6% in 2022 to 4.9% in 2024, in the first half of 2025 this ratio was only at 0.5%.

|

| Net bad debt settlement ratio after recovery of F88 (Report of Vietcap Securities Company) |

Mr. Phung Anh Tuan said that F88's goal for the next years is to control this ratio below 5%, and the Board of Directors of F88 will review it every year to suit the Company's risk appetite. In Q2/2025 alone, the on-time payment rate of loans at F88 will reach 85%. For processed debt, the recovery rate of processed debt over written-off debt of F88 is 34%.

Vietcap Securities commented that despite significantly expanding its loan portfolio, F88 still maintained a stable debt settlement rate, reflecting its solid credit risk management capabilities. In addition, operating efficiency improved, with costs slightly reduced even as disbursements and customer numbers increased sharply. “In the first half of 2025, F88 showed strong financial performance, marking a clear shift from a cautious recovery phase to breakthrough growth. Revenue increased thanks to stable lending activities and soaring insurance income, while profit after tax increased more than 3 times - driven by better asset quality, tight cost control and improved profit margins.” F88's profit after tax recorded VND255 billion, and ROE 2.37%/month.

Mr. Nguyen Quang Thuan (Chairman of FiinGroup) commented that the alternative finance sector currently has a lot of potential and room for development, the important issue is how to convert to a new generation model and apply technology to optimize operations. Technology and data are the biggest valuation factors of F88 besides people and systems, Mr. Thuan emphasized.

It can be seen that F88 has built a credit risk management ecosystem that goes beyond the framework of a traditional pawn shop. Thanks to that, the Company can replicate the packaged model to increase scale while still ensuring high business growth results, creating a leading position in the industry.

Source: https://baodautu.vn/f88-tao-vi-the-dan-dau-nganh-nho-mo-hinh-quan-tri-rui-ro-rieng-biet-d378559.html

![[Photo] Prime Minister Pham Minh Chinh chaired a meeting of the Steering Committee on the arrangement of public service units under ministries, branches and localities.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/10/06/1759767137532_dsc-8743-jpg.webp)

![[Photo] Prime Minister Pham Minh Chinh chairs a meeting of the Government Standing Committee to remove obstacles for projects.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/10/06/1759768638313_dsc-9023-jpg.webp)

Comment (0)