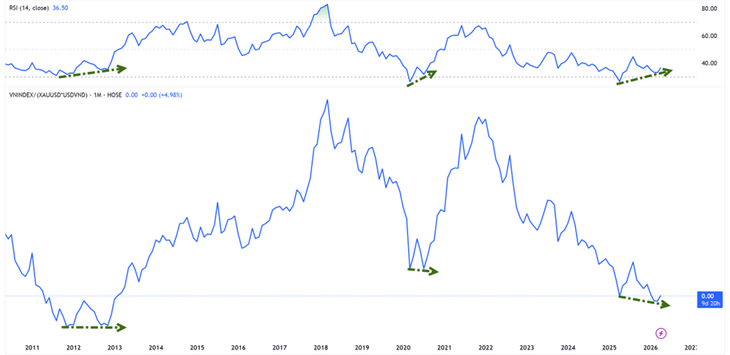

Compared to gold, the VN-Index is at its lowest point in over a decade - Photo: HUU HANH

According to statistics from Tuoi Tre Online , the Vietnamese stock market has emerged from a correction phase since the April 9th trading session. To date, the VN-Index is on its fifth consecutive week of gains.

Stock market valuation in gold: still at the bottom.

In terms of performance, the VN-Index has returned to its growth trajectory for the fourth consecutive year. As of the end of the trading session on April 22nd, the index had increased by approximately 4.1% compared to the beginning of 2026.

However, world gold prices are also experiencing their fourth consecutive year of growth and have now increased by nearly 9% since the beginning of 2026.

Mr. Nguyen The Minh - Director of the Investment Banking Division of An Binh Securities Joint Stock Company - cited a noteworthy statistic indicating that if the VN-Index is measured in gold (VNI-XAU index), the market is currently trading around the bottom of the 2012-2013 period.

This means that even if the index recovers, stocks are being left far behind by gold in the upward trend.

However, VNI-XAU is showing bullish divergence signals with momentum indicators.

"In the past, this signal appeared during the 2012-2013 period and in 2020 - times when the market formed a long-term bottom before entering a new upward cycle," Mr. Minh analyzed.

Cheap money hasn't returned yet, but the pressure has eased.

From a cash flow perspective, interest rate developments are showing initial positive signs. Mr. Bui Van Huy, Director of Investment Research at FIDT JSC, stated that the interbank overnight interest rate had fallen sharply from around 8%-10% at the beginning of April to 4% in mid-April.

The cooling of short-term capital costs helps reduce liquidity pressure in the system and improves market sentiment as concerns about capital being drawn away from risky assets are somewhat alleviated.

However, according to Mr. Huy, this cannot yet be considered a sign of a new cycle of cheap money. In 2025, credit growth is expected to be around 19% while deposits will only increase by 11.4%, forcing many banks to continue relying on the interbank market and bond channels.

Therefore, the recent move was more of a "local de-escalation" than a reversal of monetary policy.

The impact on stocks currently is mainly limited to supporting valuations and sentiment, while forming a longer-term uptrend still requires additional conditions such as profit growth and the return of real cash flow.

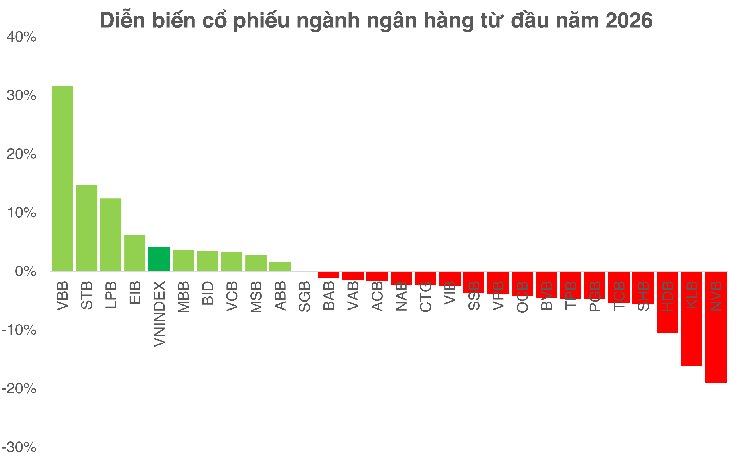

Banks remain the "test case" for the market.

According to Mr. Bui Van Huy, the banking sector remains the most important variable for assessing the sustainability of the market. In terms of valuation, this group is currently trading around a P/B ratio of 1.3 times with an ROE of approximately 16% - significantly lower than historical levels.

While there is still room for revaluation, opportunities will not be evenly distributed. 2026 is projected to be a period of strong differentiation, with banks having strong capital bases, high CASA, and stable asset quality continuing to increase their advantages, while weaker banks face pressure from declining NIM and rising cost of capital.

With the industry-wide NIM potentially falling below 3% and credit becoming more selective, investing in banks becomes more challenging, requiring a more selective approach rather than simply buying based on industry trends.

As of the end of trading on April 22nd

From another perspective, Mr. Nguyen Van Truc - Director of the Analysis Center of NSI National Securities Joint Stock Company - emphasized that the wave of capital increases is establishing a new competitive landscape, aiming towards a charter capital of 100,000 billion VND.

In the short term, raising capital may put pressure on stock prices due to increased supply. But in the long term, the deciding factor remains the efficiency of capital utilization. If the profits generated exceed the dilution level, the stock may be revalued to a higher level.

Conversely, if capital is not converted into real growth, downward price pressure is inevitable.

Source: https://tuoitre.vn/chung-khoan-viet-dang-o-dau-so-voi-gia-vang-20260422185600168.htm

![[Image] Pleasant weather helps students enter the 10th grade entrance exam with confidence.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/05/29/1780034401612_ngay-1-thi-lop-10-minh-duy-8-5009-jpg.webp)

![[Photo] Ba Lang An Lighthouse - the "eye of the sea" amidst the "rock museum" of Quang Ngai province.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/05/29/1780038698840_anh-man-hinh-2026-05-29-luc-14-10-42.png)

Comment (0)