Supply and demand pressures have driven cocoa prices plummeting.

At the close of yesterday's trading session, the industrial raw materials market witnessed overwhelming selling pressure as most key commodities in the group simultaneously declined in price. Cocoa, in particular, became the focus of investor attention, recording its third consecutive day of price decline.

Specifically, the March cocoa futures contract lost as much as 7.24% yesterday, falling to $3,805 per ton, its lowest level in over two years.

According to the Vietnam Commodity Exchange (MXV), the dual pressure from both supply and demand is weighing heavily on the global cocoa market as global consumption weakens significantly while supply shows signs of a stable surplus.

The global cocoa market is facing a bleak consumption outlook as reports of fourth-quarter 2025 crushing output show significant declines in key producing regions.

According to data released by the European Cocoa Association (ECA) on January 15th, cocoa grinding in the region in the fourth quarter of 2025 fell sharply by 8.3% compared to the same period last year, to 304,500 tonnes. This is not only a much deeper decline than previous market forecasts (-2.9%) but also marks the lowest fourth-quarter production level in the past 12 years.

A similar situation was observed in the Asian market. A December 16th report from the Asian Cocoa Association indicated that cocoa grinding in the region had decreased by 4.8%, falling to 197,022 tons. Meanwhile, in the US market, activity remained virtually stagnant with negligible growth.

Weakening consumer demand is also evident in the financial reports of industry giants. Barry Callebaut AG, the world's largest producer of raw chocolate, reported that its cocoa sales plummeted 22% in the quarter ending November 30th.

While consumer demand shows signs of slowing, the global cocoa supply picture continues to show signs of surplus, reinforcing the downward price trend on exchanges.

According to the latest report from StoneX, the global cocoa market is expected to experience a surplus in the medium term. Specifically, the organization forecasts a surplus of 287,000 tons in the 2025-2026 crop year and a continued surplus of 267,000 tons for the 2026-2027 crop year. Similarly, the International Cocoa Organization (ICCO) reported that as of January 23rd, global cocoa reserves had increased by 4.2% year-on-year, reaching 1.1 million tons.

The "mismatch" between supply and demand has directly pushed ICE-monitored inventories to their highest level in 3.5 months, exceeding 1.83 million bags. This abundant inventory is creating significant oversupply pressure, fueling a prolonged downward correction trend.

Furthermore, in West Africa – the world's cocoa capital – meteorological conditions continue to favor the harvest. According to World Weather Inc., the region will maintain stable weather patterns for the next two weeks.

Sparse coastal showers combined with warm temperatures are expected to continue until the end of February, before seasonal rains begin to increase in the south. Notably, the intensity of the Harmattan winds in Africa remains mild, helping to limit negative impacts on crop development. Temperatures, while warm, are not excessively hot, creating ideal conditions for the current growing season.

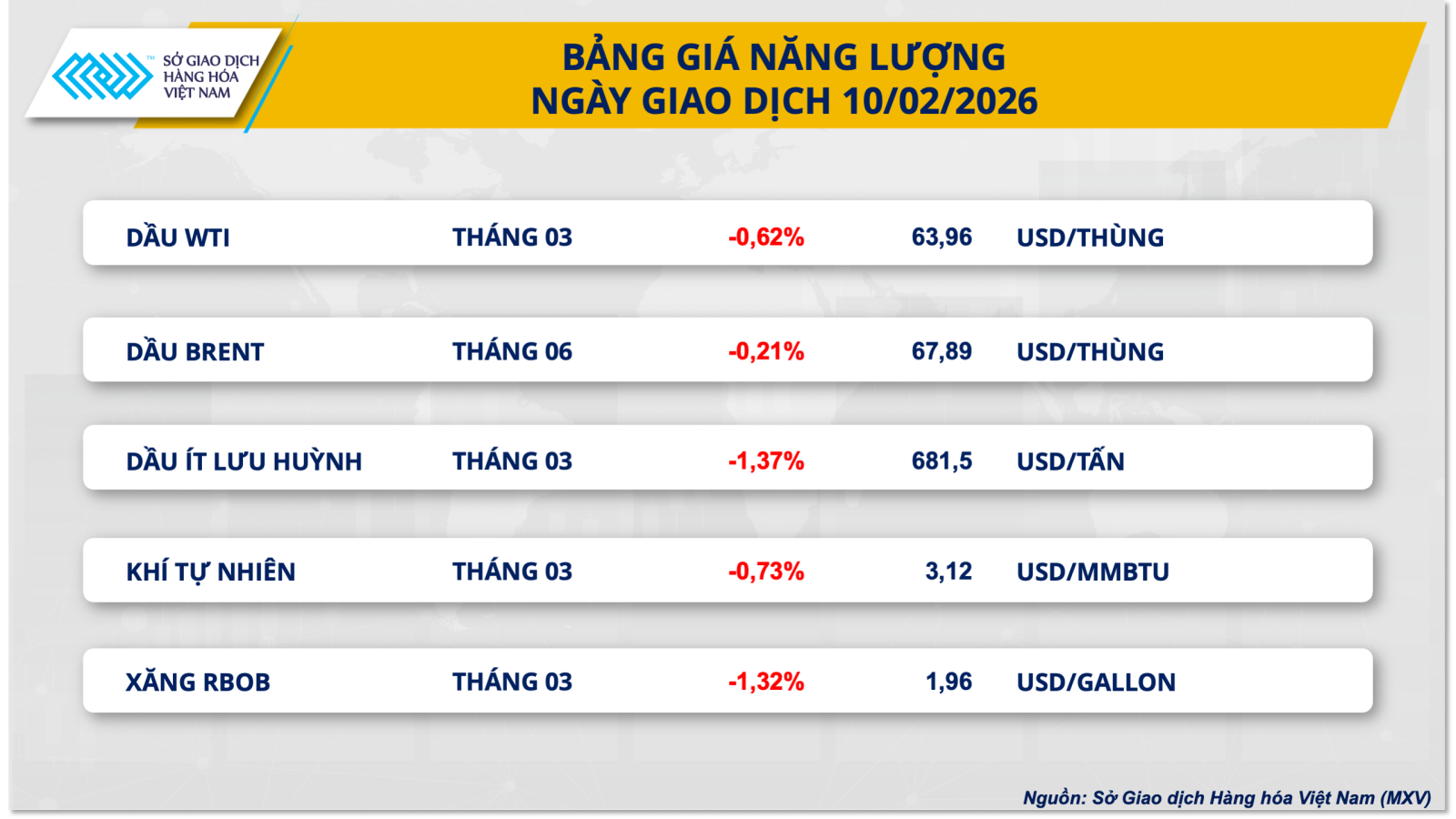

World oil prices fell sharply amid a gloomy outlook for the US economy .

Meanwhile, in the energy market, red dominated all five commodities in the group. Brent crude oil ended the session at $67.9 per barrel, a decrease of more than 0.2%; while WTI crude oil also recorded a decrease of more than 0.6%, falling back below $64 per barrel.

According to MXV, pressure from concerns about the outlook for consumption in the US weighed heavily on the global oil market during yesterday's trading session.

According to the latest data from the US Department of Commerce, retail sales in December 2025 unexpectedly remained flat, and the October data was also revised downward. The main reason is that households are tightening their spending on vehicles and high-value goods. This has slowed consumer spending and economic growth in the US this year, leading to a direct decrease in energy demand.

In addition, in its January 2026 Short-Term Energy Outlook (STEO) report, the U.S. Energy Information Agency (EIA) projected that demand for gasoline in the country would decline in both 2026 and 2027.

However, conversely, the EIA has upgraded its outlook for distillate and jet fuel consumption. This adjustment is based on positive GDP growth and industrial production expectations according to S&P Global's macroeconomic model. This is seen as a key factor in curbing the short-term decline in oil prices.

On the other hand, despite localized supply disruptions in the US and Kazakhstan or recent price fluctuations, the EIA maintains its forecast of global oversupply for the next two years.

The agency predicts that strong growth in global oil production will drive up inventories throughout the forecast period. As a result, crude oil prices are projected to maintain a downward trend, averaging $58 per barrel in 2026 and further declining to $53 per barrel in 2027.

Besides macroeconomic factors, the geopolitical situation in the Middle East is also showing signs of easing, causing the "risk premium" on oil prices to lose the momentum it had at the beginning of the week.

Attention is now focused on the latest statements from US President Donald Trump. In an interview yesterday, Trump suggested that the US and Iran could absolutely reach a new nuclear agreement, replacing the previous one that was withdrawn from in 2018.

According to energy consulting firm Gelber & Associates, investors "are hesitant to push prices in any direction until there are clearer signals from diplomacy, subsequent inventory data, or any confirmation that supply is being significantly impacted, not merely threatened."

Source: https://baotintuc.vn/thi-truong-tien-te/dut-mach-phuc-hoi-mxvindex-lui-sat-moc-2500-diem-20260211090607706.htm

![[Photo] Standing Committee member of the Party Central Committee Tran Cam Tu working with the Central Inspection Committee](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/05/28/1779969579668_ndo_br_bnd-2495-jpg.webp)

Comment (0)