The profit picture for the banking sector in the first quarter of 2026 is showing strong divergence. While some "big players" maintain growth thanks to stable credit volume and fee income, many medium and small-sized banks have recorded significant profit declines, even plummeting compared to the same period last year.

Profits plummeted.

According to the Q1/2026 financial reports, many banks recorded a significant decline in profits due to narrowing net interest margins, increased risk provisioning costs, and pressure to resolve bad debts.

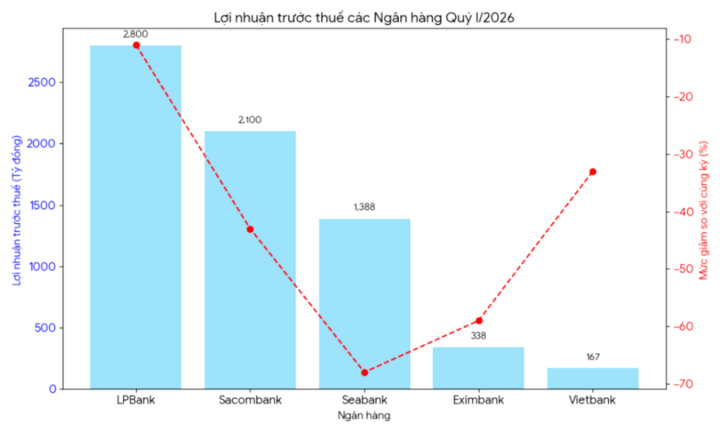

Many banks reported a significant drop in pre-tax profits compared to the same period last year. (Photo: Dai Viet)

At LPBank , pre-tax profit in the first quarter of 2026 reached just over VND 2,800 billion, a decrease of 11% compared to the same period last year. LPBank's pre-tax profit declined sharply due to slower credit growth and persistently high capital costs. Some extraordinary income from the previous year no longer helped the bank maintain its profit surge.

Sacombank also experienced a significant decline in profits. Specifically, the bank's pre-tax profit in the first quarter of 2026 reached only over 2,100 billion VND, a decrease of 43% compared to the same period last year. Sacombank recorded a slowdown in business results after a period of rapid growth. Revenue from service activities and the handling of non-performing loans no longer showed the breakthroughs of previous quarters, while the pressure to make provisions increased significantly.

At SeABank , the decline in profits was also significant. Pre-tax profit in the first quarter of 2026 reached only VND 1,388 billion, a decrease of 68% compared to the same period last year. According to the financial report, the reason for this erosion of profits is that the cost of capital mobilization increased faster than the growth rate of interest income. The net interest margin (NIM) tends to narrow as banks are forced to maintain attractive deposit interest rates to retain funds.

Eximbank was no exception; this bank also experienced a sharp decline in pre-tax profit in the first quarter of 2026, reaching only 338 billion VND, a decrease of 59% compared to last year. Vietbank also had a pre-tax profit of only 167 billion VND, a decrease of 33% compared to the previous year.

Both Eximbank and Vietbank recorded a decline in profits due to slow credit growth and a lack of significant improvement in non-interest income. Foreign exchange and investment securities trading also no longer contributed as much as in 2025.

Among smaller banks, Saigonbank also reported pre-tax profits of only VND 88 billion in the first quarter of 2026, a 10% decrease compared to the same period last year. The bank continues to face numerous challenges related to scale, operational efficiency, and competitive pressure. Saigonbank's first-quarter profits also declined significantly compared to the previous quarter due to increased operating expenses and provisions for bad debts.

Banks are experiencing a sharp decline in profits due to shrinking net interest margins, rising risk provisioning costs, and pressure to resolve bad debts. (Photo: BL)

Reasons for the sharp decline in profits.

According to financial experts, there are several reasons why banks' business results declined in the first quarter of 2026.

According to financial analyst Nguyen Thuy Hang, the decline in business results of many banks in the first quarter of 2026 is primarily due to a narrowing net interest margin (NIM).

According to Ms. Hang, after a period of fierce competition in capital mobilization from the end of 2025, the cost of capital for many banks remains high. However, lending interest rates are unlikely to increase correspondingly due to pressure to support businesses and stimulate the economy.

In addition, credit growth has not met expectations, significantly impacting revenue. Many businesses remain cautious about borrowing capital amidst slow demand recovery and a real estate and consumer market that has not yet fully recovered.

Furthermore, bad debts are showing signs of increasing again after a period of restructuring and debt deferral. This forces banks to significantly increase their risk provisions, directly reducing profits.

"Another reason is the weakening of non-interest income. In 2025, many banks had a surge in revenue from bancassurance, bond investments, or foreign exchange trading. By 2026, these revenue sources will no longer maintain the high growth rates they did before," Ms. Hang said.

According to Ms. Hang, the pressure on banks' profits may continue in the coming quarters if bad debts are not thoroughly resolved and credit demand does not recover strongly.

However, analysts still expect that more stable interest rates in the second half of 2026 could help improve profit margins for banks. In addition, accelerating digitalization, cutting costs, and expanding service fee revenue will be crucial directions for banks to maintain sustainable growth in the coming period.

Source: https://vtcnews.vn/nhieu-ngan-hang-co-tinh-hinh-kinh-doanh-giam-ar1016915.html

![[Image] Hanoi's urban life under the challenge of a "scorching hot" environment](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/05/25/1779706979265_nang-nong-t5-2026-minh-duy-7-4636-jpg.webp)

Comment (0)