The momentum from foreign institutional capital flows returning

Update on the stock market, trading session on July 25, 2025, VN-Index closed at a historical peak of 1,531.13 points with liquidity maintained at a high level, reaching 33,939 billion VND.

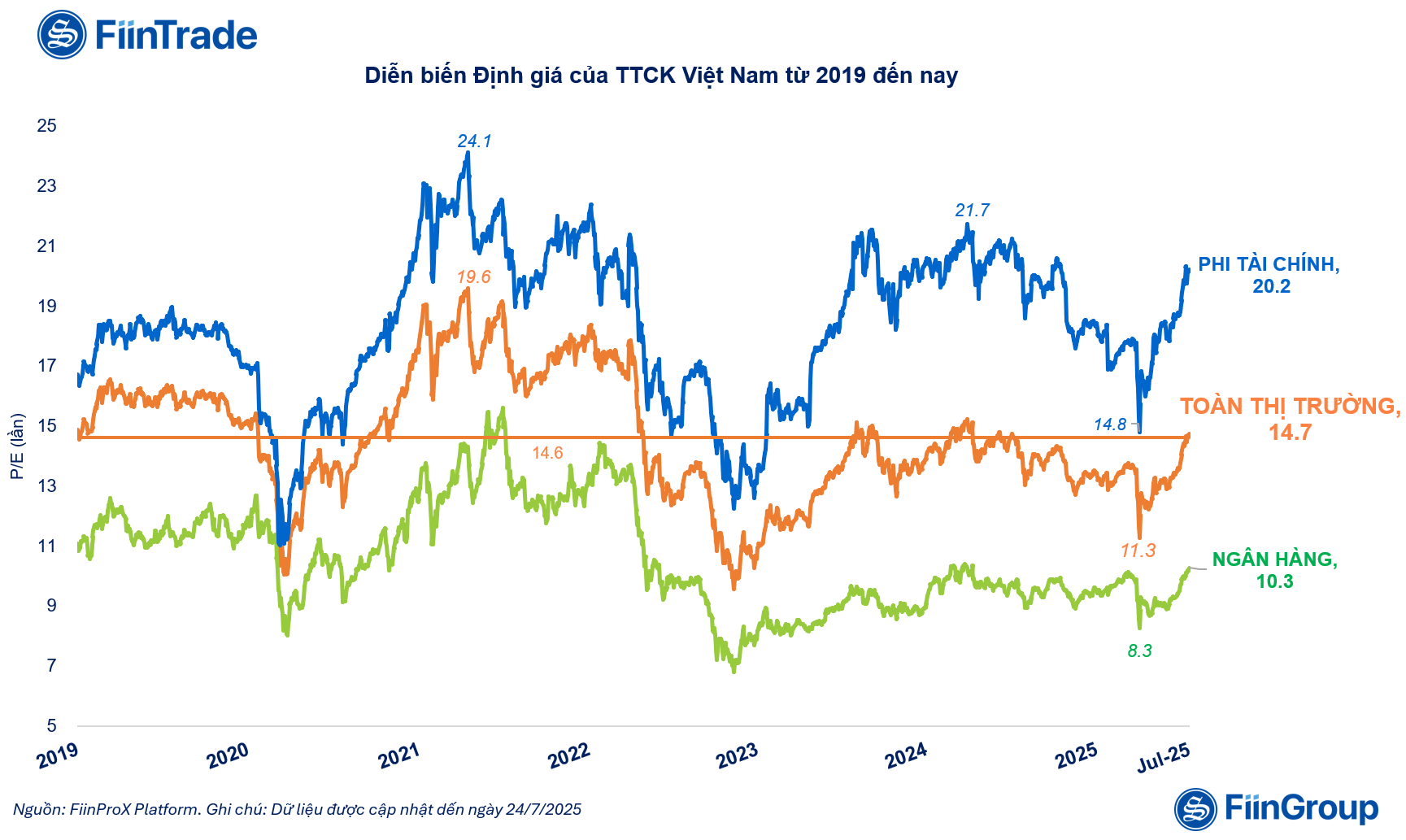

Assessing this growth, FiinTrade said that market valuations have been significantly increased in 2025. Specifically, the P/E of the whole market has increased by 30% since the beginning of April 2025, reaching 14.7 times - higher than the 5-year average and up 10% compared to the end of 2024.

Contributions to this increase in valuation mainly come from the Non-financial group, including stocks of the Vin family (VIC, VHM, VRE), Gelex family (GEX, GEE), and Banks (TCB, MBB,SHB , OCB), Securities (SSI, HCM, VCI, VND).

Stock market growth valuations have risen significantly in 2025 |

Assessing the current growth of the market, analysts from FiinTrade said there are many differences compared to the 2021 period.

If in 2021, the market exploded thanks to individual cash flow, pushing the entire market valuation to the peak (19.6 times), then the recovery in 2025 will have different characteristics. The main driving force comes from the return of foreign institutional capital, in the context of increasingly clear expectations of upgrading the market from "frontier" to "emerging" and the macro picture is changing positively.

Although the index is increasing, it should be noted that the current profit base of listed companies has not really broken through. The two sectors that account for a large proportion of the profit structure and market capitalization - Banking and Real Estate - are still facing certain resistance.

The banking sector recorded modest profit growth due to pressure on narrowing net interest margins (NIM), while the real estate sector is only in the early stages of the recovery cycle and needs more time to be more clearly reflected in business results.

Profit highlights from Securities, Public Investment and Export Companies

Update on business results, according to data compiled by FiinTrade as of July 25, 2025, 596 listed enterprises (representing 35.4% of total market capitalization) have announced financial reports or preliminary estimates of business results for the second quarter of 2025.

Because the number of enterprises is not large enough, it is still not enough to represent the whole industry/the whole market. However, preliminary assessment shows that the after-tax profits of enterprises are maintaining a stable growth rate, increasing by 12.5% compared to the same period in 2024.

In the group of financial enterprises, securities companies are the leading representatives of growth. The Securities group had a 39.5% increase in after-tax profit compared to the same period last year in the second quarter, leading the Finance sector. Notably, some small and medium-sized securities companies recorded extraordinary profits compared to the same period thanks to the positive market performance in the second half of the second quarter, such as VIX, DSC with the proprietary trading segment or DNSE with the margin lending segment.

In the non-financial group, the recovery was evident in the group of public investment and export enterprises.

The after-tax profit in the second quarter of 2025 of 544/1,512 enterprises in the non-financial group (representing 34.8% of the group's capitalization) increased by 11.2% over the same period. This is the second consecutive quarter of slowing growth, however, there are still many bright spots thanks to favorable seasonal factors and positive impacts from support policies.

In the Public Investment group, Construction and Materials continued to improve thanks to the strong disbursement of public investment in the second quarter, with profits increasing by 43.4% in the Construction group and 49.7% in the Construction Materials group, respectively. Notably, Cement enterprises (HT1, BTS, HOM) and Construction Stone (VLB, DHA, NNC) recorded positive growth, while the Plastic Pipe group (BMP, NTP) witnessed a slowdown in profit growth.

The steel industry recorded a 24.7% year-on-year profit growth in the second quarter, led by Hoa Phat (HPG) with a 29.5% increase. However, the industry’s revenue decreased by -6.1%, including HPG and HSG, showing that the recovery in market demand is still weak.

For the export group, seafood companies such as ANV, FMC and Textile (VGT, TNG, HTG) recorded a sharp increase in profits in the second quarter of 2025, up to 576.8% and 47.1% respectively thanks to a wave of orders to avoid the risk of high taxes. This is a bright spot in the context of many manufacturing industries still recovering slowly. However, this growth rate does not reflect the results of many leading enterprises.

Source: https://baodautu.vn/dong-von-ngoai-quay-lai-dong-luc-manh-me-thuc-day-vn-index-lap-ky-luc-moi-d342199.html

![[Photo] General Secretary To Lam presents the First Class Labor Medal to the Vietnam National Energy and Industry Group](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/9/21/0ad2d50e1c274a55a3736500c5f262e5)

![[Photo] General Secretary To Lam attends the 50th anniversary of the founding of the Vietnam National Industry and Energy Group](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/9/21/bb0920727d8f437887016d196b350dbf)

Comment (0)