|

| Non-interest income is one of the brightest spots of the banking industry in the first half of 2025. |

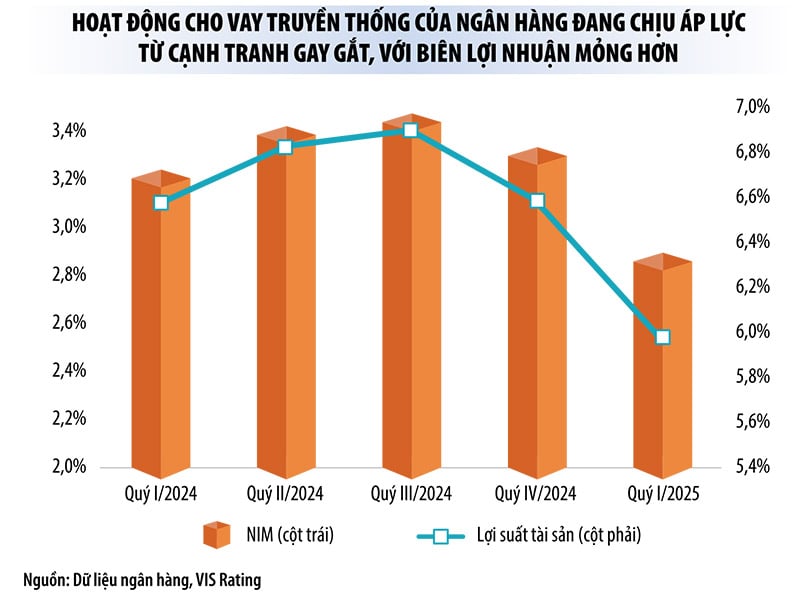

Strong increase in non-interest income offsets decline in net interest margin

The second quarter 2025 financial report shows that in the first half of this year, non-interest income was one of the brightest spots in the banking industry.

For example, atACB , total operating income in the first 6 months of the year increased insignificantly compared to the same period last year, even net interest income decreased by 5.7%, but non-interest income increased by nearly 40%, thanks to large contributions from foreign exchange trading, investment securities trading, debt collection and risk handling.

Similarly, at VIB, net interest income in the first 6 months of this year decreased by more than 11%, while non-interest income increased by nearly 20%. At LPBank, net interest income decreased by 1.3%, while non-interest income increased by 17.3%. AtSHB , net interest income increased by 53%, while non-interest income increased by 163%. At MB, non-interest income increased by 30%, while net interest income increased by 22.8%.

“In the context of fierce competition in deposit interest rates, causing net interest margins (NIM) to narrow and net interest income to be under pressure, many banks are actively expanding into asset management to diversify their revenue sources outside of traditional credit activities. This could become a common trend in the medium term,” said an analyst from SSI Research.

Notably, in the first half of this year, many banks recorded a sharp increase in profits from other business activities, even increasing by several times, mainly due to a surge in debt collection and risk handling.

Specifically, at Techcombank, most business activities decreased compared to the same period in 2024, but net profit from other activities increased by 3.1 times compared to the same period last year (more than 66% of profit from this segment came from debt that had been resolved). At ACB, net profit from other activities also increased by 2.9 times. At LPBank , revenue from debt that had been resolved increased by 2.3 times compared to the same period in 2024, helping the bank's net profit from other activities increase by 2.2 times.

At KienlongBank, net profit from other business activities increased 3 times compared to the same period last year (in particular, bad debt collection handled by risk provisions increased 2.8 times). This figure at SHB increased 1.5 times. Meanwhile, VPBank, VIB and MB recorded increases of 49%, 63% and 82% respectively.

Ms. Le Thu Uyen, an analyst at VPBank Securities Company, said that the legalization of Resolution No. 42/2017/QH14 of the National Assembly on piloting bad debt settlement of credit institutions is creating an important turning point in handling secured assets, helping banks speed up capital recovery. This will help many banks continue to increase revenue from bad debt in the coming time, especially banks with a large proportion of consumer credit.

|

Non-interest income is no longer “ancillary”

Currently, interest income still accounts for 70-90% of total operating income of banks, but non-interest income plays an increasingly important role, with outstanding growth rate. Many banks consider this a strategic business segment, instead of being "supportive" as in the previous period.

According to Ms. Le Thu Uyen, in the context of NIM trending downward, non-interest income is playing an important role in maintaining total operating income and pre-tax profit.

“We believe that the growth in non-interest income in the second quarter of 2025 will partly offset the decline in NIM at some banks. This will help these banks maintain stable total operating income and pre-tax profit,” Ms. Uyen analyzed.

Currently, banks such as Techcombank, Sacombank, VPBank, ACB, VietinBank, MB have a high contribution rate from non-interest income. Many banks, thanks to their multi-layered digital ecosystem, have taken advantage of their advantages to increase non-interest income.

In recent years, a series of banks have also promoted mergers and acquisitions (M&A) of securities and insurance companies to increase market share in these fields, or expanded into the securities sector to help increase revenue from service fees and effectively exploit the customer network to develop the ecosystem. In the first half of this year, a number of banks announced plans to buy shares of securities companies (Sacombank, SeABank, MSB) or enter into strategic cooperation with securities companies (OCB, VIB).

Ms. Nguyen Ha My, an analyst at VIS Rating Company, said that in the context of traditional lending activities being under pressure from fierce competition, thinner profit margins and credit growth limits still being applied, it is understandable that banks expand their securities business to improve profitability. In 2024, some securities companies associated with banks, such as Techcom Securities Joint Stock Company (TCBS), contributed significantly (nearly 20%) to the parent bank's profits.

In the list of non-interest-bearing business activities, banking experts assess that foreign exchange trading, asset investment (government bonds, fund certificates, etc.), and payment services are no longer the “golden goose”. Meanwhile, the securities and insurance sectors still have a lot of room.

In addition, the asset management segment will be targeted by many banks if gold and cryptocurrency exchanges are established. Banks that are “quick” to enter the digital asset game will benefit greatly, not only by increasing service fees, but also by strengthening relationships with high-net-worth clients.

However, SSI Research analysts warned that providing this service also poses many risks for banks, requiring banks to upgrade their internal control systems, risk management frameworks and legal compliance systems accordingly.

Source: https://baodautu.vn/ngan-hang-lai-lon-nho-thu-ngoai-lai-d345605.html

![[Photo] General Secretary To Lam meets voters in Hanoi city](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/9/23/d3d496df306d42528b1efa01c19b9c1f)

![[Photo] The 1st Congress of Party Delegates of Central Party Agencies, term 2025-2030, held a preparatory session.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/9/23/e3a8d2fea79943178d836016d81b4981)

![[Photo] Prime Minister Pham Minh Chinh chairs the 14th meeting of the Steering Committee on IUU](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/9/23/a5244e94b6dd49b3b52bbb92201c6986)

![[Photo] Editor-in-Chief of Nhan Dan Newspaper Le Quoc Minh received the working delegation of Pasaxon Newspaper](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/9/23/da79369d8d2849318c3fe8e792f4ce16)

Comment (0)