“If you are young and healthy, you don't need to buy life insurance yet.”

This is one of the common misunderstandings among young people. In fact, youth is an advantage because at this stage, usually in good health, you will easily be approved by the insurance company for a contract with a low premium (standard premium). But when you get older, your body begins to show signs of illness, the insurance company may approve insurance with a premium higher than the standard premium, or even refuse to issue an insurance contract. Many people only start buying insurance when they see health problems, however, at this time, pre-existing diseases will be excluded or insurance will be refused.

Another common misconception among young people is that it is enough to buy health insurance (health card) annually, and there is no need to participate in life insurance. In fact, annual health insurance only has low premiums when you are young and in good health. However, the application will be re-evaluated every year, so if your health has problems the following year, the insurance premium will increase very high or cannot be renewed. With life insurance, long-term protection benefits will bring maximum peace of mind to customers.

"When you have a lot of money, you should buy life insurance"

Many people believe that life insurance is for people with average income or higher. In fact, life insurance products today are designed in a variety of ways with flexible fees, suitable for many different income groups.

Low-income groups or those not ready to spend on life insurance can consider simple, protection-oriented products with short premium payment periods or refund commitments, such as term insurance products.

Higher income groups who need both risk protection and medium- and long-term asset accumulation can consider investment-linked insurance products. Those who need comprehensive protection can participate in additional supplementary insurance packages for health care, critical illness, etc.

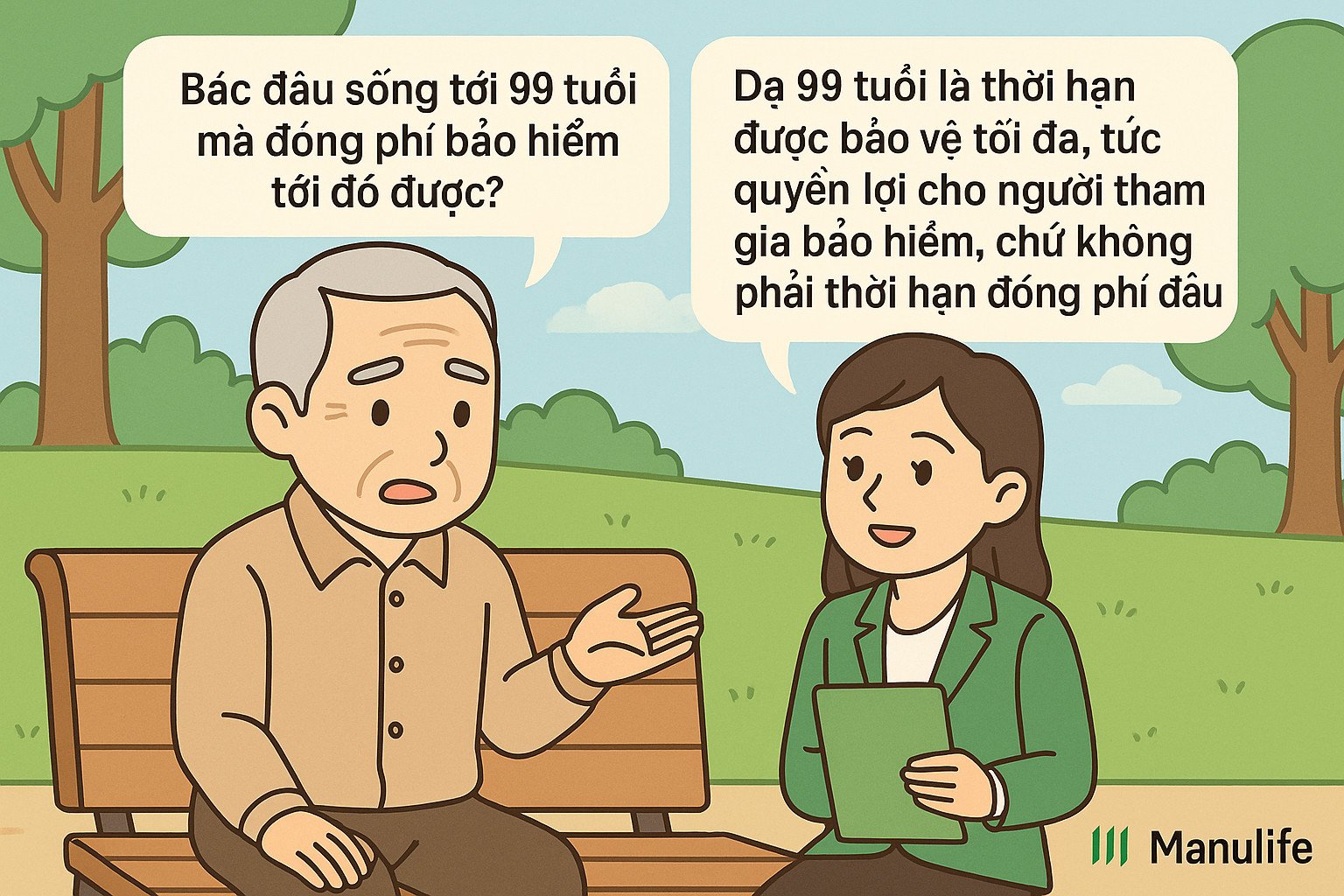

“The consultant said to pay the fee for 15 years, but the contract says it expires at age 99. What's going on?”

This is a common misconception, stemming from a failure to distinguish clearly between 'premium payment period' and 'contract period'.

The contract term (also known as the insurance period) is the maximum period of time during which the customer is protected by the insurance contract.

The premium payment period is the period of time during which the customer needs to pay the premium to be insured.

Traditional products usually have the same premium payment period and contract term, usually 10, 15, 20 years. Customers choose the premium payment period and contract term when participating in insurance.

Compared to traditional products, popular investment-linked insurance products today are more flexible. Customers do not need to choose the contract term when participating in insurance, but the maximum insurance period of the contract is usually set until the customer reaches 99 years old.

Customers need to pay a minimum premium for the first 3 or 4 years, then have the right to choose to stop or continue paying premiums flexibly until the 10th, 15th, 20th year or longer depending on their needs. The insurance contract will remain in effect if the account value is sufficient to cover the insurance costs. Customers also have the flexibility to terminate the contract before the contract term ends and receive the account value (if any) at the time of contract termination, but are not required to pay until age 99 to receive the account value.

For example, Ms. Nguyen Thi A (30 years old) - participates in a unit-linked insurance package of Manulife with an insurance term until the age of 99, which means her contract lasts for 69 years. After the first 3-4 years of paying mandatory premiums, Ms. A can choose to continue paying premiums until the 10th, 15th or 20th contract year depending on her financial capacity and needs, without having to pay insurance premiums for the entire 69 years. She can also choose to terminate the contract when she reaches the age of 70 and receive the contract account value at that time, without having to wait until the age of 99.

“Paying fees for many years, withdrawing not much!”

The nature of life insurance is to protect you from unforeseen risks, unlike saving money in a bank or other forms of investment. When you have participated in life insurance, whether you have just paid the premium for 1 month or have paid for a long time, if a risk occurs (accident, death, permanent disability, etc.), the insurance company will pay you compensation many times higher than the premium you have paid.

Besides, life insurance is a long-term product, so to have accumulated value, you need to determine to participate for a long time. If you only participate for the first few years and withdraw money, the refund value will not be high, because most of your insurance premium has been allocated to costs such as: initial fee, risk fee, contract management fee, fund management fee, agent commission, etc.

Therefore, you should maintain a long-term insurance contract. When it matures, your accumulated value will increase significantly. In addition, you can receive other benefits such as: contract maintenance bonus, investment profit if participating in investment-linked insurance products, etc.

Life insurance is a long-term financial plan. You cannot predict what will happen in the future, but you can proactively prepare to minimize the financial burden if risks arise. Understanding correctly, participating correctly, maintaining correctly - is the way to maximize the value of insurance, helping you feel more secure in the face of unexpected changes in life.

(Source: Manulife)

Source: https://vietnamnet.vn/nhung-lam-tuong-khien-nhieu-nguoi-bo-qua-bao-hiem-nhan-tho-2412535.html

Comment (0)