Amending and supplementing regulations on taxpayers and taxable income

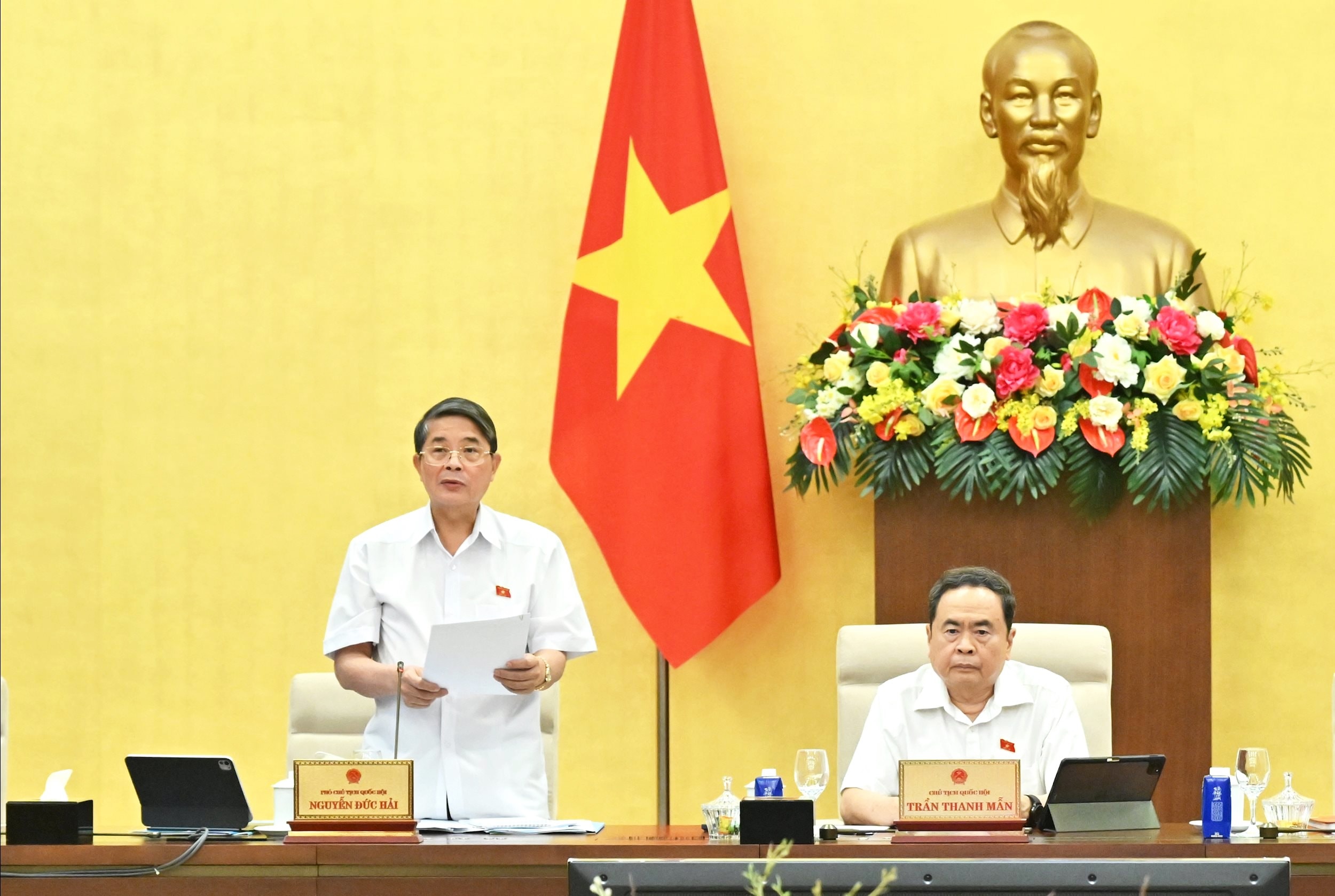

The proposal for the Law on Personal Income Tax (amended) presented by Deputy Minister of Finance Cao Anh Tuan said that the promulgation of the draft Law aims to expand the tax base; review, amend and supplement regulations on taxpayers and taxable income; study and adjust the threshold and personal income tax rates for some types of income, ensuring consistency with the nature of each type of income and the regulatory objectives of personal income tax. Study and adjust the family deduction level for taxpayers and dependents, amend and supplement regulations related to some specific deductions to suit the new context...

The Draft Law consists of 4 chapters and 30 articles, regulating taxpayers, taxable income, tax-exempt income, tax reduction, and the basis for calculating personal income tax.

The draft Law amends and completes regulations on tax calculation for each type of income, restructures and adjusts the names of some articles to correspond to the amended content. Amends and completes regulations on income subject to personal income tax for income from business; from salaries and wages; tax calculation for capital transfer activities; expands the scope of income from inheritance and gifts. Regulates the level of revenue not subject to tax for income from business consistent with the level of revenue not subject to value added tax prescribed by the Law on Value Added Tax (VND 200 million/year or less) and assigns the authority to the Government to regulate and adjust this level...

Need to specify taxable income

The review report presented by Chairman of the Economic and Financial Committee Phan Van Mai stated that the Standing Committee of the Committee agreed on the necessity of comprehensively amending the Law on Personal Income Tax to promptly institutionalize the viewpoints and orientations of the Party and State in perfecting the tax policy system, including personal income tax. Thereby, contributing to establishing a unified and synchronous legal framework and more clearly demonstrating the role of income regulation, aiming at social equity of the personal income tax policy.

Regarding taxable income (Article 3), the majority of opinions believe that this is an important content, directly related to the rights and legitimate interests of taxpayers, and needs to be specifically regulated in the Law. The provisions of the current Law on Personal Income Tax have also been summarized and evaluated, and new income items arising in practice that have not been regulated have basically been supplemented and reflected in the draft Law.

Therefore, it is recommended that the drafting agency conduct research to specify in the draft Law on taxable income. Some opinions suggest that, in case there is a need for regulations to adjust and supplement taxable income, it is recommended to consider regulations in the direction that the Government submits to the National Assembly Standing Committee for consideration and decision.

Many opinions suggest considering the tax on gold bar transfers to avoid inconveniences for people who transfer gold not for speculative or business purposes. Some opinions suggest adding the determination/limit of the weight threshold of gold bars subject to personal income tax.

Regarding family deduction (Article 11), the Standing Committee believes that the proposal to amend and supplement the regulations on family deduction levels is necessary to suit the current practical situation.

The practice of adjusting and amending the provisions of the current Law on family deductions and through studying the experiences of other countries shows that the family deduction level does not necessarily need to be adjusted regularly and continuously. Therefore, there is no need or urgency to assign the Government to regulate to ensure flexibility and timeliness.

The majority of opinions suggested that the Law should specifically stipulate the family deduction level for taxpayers and dependents as expressed in the current Personal Income Tax Law to ensure authority, clarity and transparency.

Some opinions agree to assign the Government to regulate the family deduction level. However, it is proposed to stipulate in the Law the minimum and maximum family deduction levels for taxpayers and dependents, establishing the basic principle for the Government to regulate the specific deduction level.

Concluding the discussion, Vice Chairman of the National Assembly Nguyen Duc Hai stated that the National Assembly Standing Committee highly appreciated the Government's preparation of the draft Law and the verification report of the Economic and Financial Committee.

At the same time, it is necessary to continue reviewing to ensure full institutionalization of the Party's policies, perfecting policies and laws on personal income tax, ensuring the provisions of the Law on compliance with the Constitution, synchronization and consistency with the law. Ensure that the Law's amendments resolve current difficulties and problems, ensuring that personal income tax is truly an important tool in regulating and redistributing income, aiming at the goal of social equity.

Review the scope of taxable income and taxable income levels to provide more specific and complete regulations, ensuring clarity, transparency, and compliance with the Constitution, because these are the core contents of the law, related to the rights, obligations, and tax responsibilities of people and businesses...

Regarding family deductions, it is recommended to study and complete them according to the proposal of the auditing agency, as shown in the current Law, which specifically stipulates the family deduction level for taxpayers and dependents. At the same time, it is necessary to stipulate the authority of the Government in submitting to the National Assembly Standing Committee for consideration and adjustment of the family deduction level in accordance with price fluctuations.

Source: https://daibieunhandan.vn/quy-dinh-cu-the-muc-giam-tru-gia-canh-voi-nguoi-nop-thue-nguoi-phu-thuoc-10390192.html

![[Photo] Solemn opening of the 1st Government Party Congress](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/10/13/1760337945186_ndo_br_img-0787-jpg.webp)

![[Photo] General Secretary To Lam attends the opening of the 1st Government Party Congress](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/10/13/1760321055249_ndo_br_cover-9284-jpg.webp)

Comment (0)