Invite customers to buy insurance with higher interest rates than savings!

Reporting to VietNamNet newspaper, Ms. Nguyen Thi Bich Dao (residing in Phuc La ward, Ha Dong district, Hanoi) said that in March 2020, she deposited savings atVIB Transaction Office (Xa La, Ha Dong) with an interest rate of more than 7%/year.

Here, she was advised by staff Pham Thi Minh Phuong about the insurance package "Pru-Flexible Investment", which VIB cooperated with Prudential life insurance. Along with that was a commitment of higher interest rates than savings, and at the same time, support for customers to open credit cards to pay monthly installments, 2.5 million VND per month. Initially, Ms. Dao ignored all advice and persuasion.

One month later, returning to VIB Xa La to continue saving, Minh Phuong staff successfully convinced her with a “Pru-Flexible Investment” contract. She simply thought that this was a high-interest savings account with additional insurance benefits.

The contract is effective from March 4, 2020, with an insurance premium of 30 million VND/year (this contract has nothing to do with your savings deposit at VIB).

In 2021, Ms. Dao continued to be invited by Phuong's staff to participate in the Prudential Life Insurance package with the reason: "The other package has few health insurance benefits".

“At that time, I still had a lot of faith and wanted to be better protected because these two contracts would pay independently. So I joined the life insurance package and am still pursuing the second package. Phuong's greed made me very upset and I felt so stupid,” said Ms. Dao.

The reason Ms. Dao has the above feeling is because in October 2022, she discovered and thought that the nature of the first contract was completely different from what she was advised.

“Phuong emphasized that the interest rate is higher than the bank deposit interest rate, and there are also insurance benefits. Phuong provided an illustration table, but always concluded with the sentence 'this is just an illustration table, in reality it is higher'. Phuong's mistake in consulting was to affirm that 'the interest rate is higher than the savings deposit interest rate', which is completely wrong about the nature of the product,” Ms. Dao emphasized.

The bank requires proof of authenticity.

Regarding the "Pru-Flexible Investment" contract package, after discovering that the nature of this investment package was not consistent with what was advised, in October 2022, Ms. Dao filed a complaint to VIB.

After several trips and even loud arguments at VIB Xa La, it was not until March 2023 that she met the Director of VIB Xa La.

After two meetings, she was suggested to "resolve internally", the bank would support her with 15 million VND, equivalent to half a year of insurance premiums.

However, Ms. Dao did not accept the above proposal and continued to file a second complaint, requesting to terminate the "Pru - Flexible Investment" contract with the reason: Phuong's employee "abused trust, was dishonest, and gave advice that did not reflect the nature of the contract", and at the same time requested a refund of 3 years of insurance premiums paid.

“During the discussion, Phuong admitted that she had advised that the insurance package had a higher interest rate than savings. This admission was witnessed by two VIB employees. But VIB said it would not consider it as evidence, only accepting evidence in written form. This made me very upset,” said Ms. Dao.

During the process of working with the bank, VIB Xa La representative always said that because employee Pham Thi Minh Phuong (insurance sales consultant) had quit her job, it was very difficult to resolve her benefits.

“I clearly told them my wish to only stop the “Pru-Flexible Investment” Insurance package because I found it was not in line with what Phuong advised.

I would rather lose money than compromise and continue paying for a product that I was deceived about.

During the second meeting, the VIB customer service representative said, "It's already been 3 years since I paid, why bother paying more?" Ms. Dao was upset.

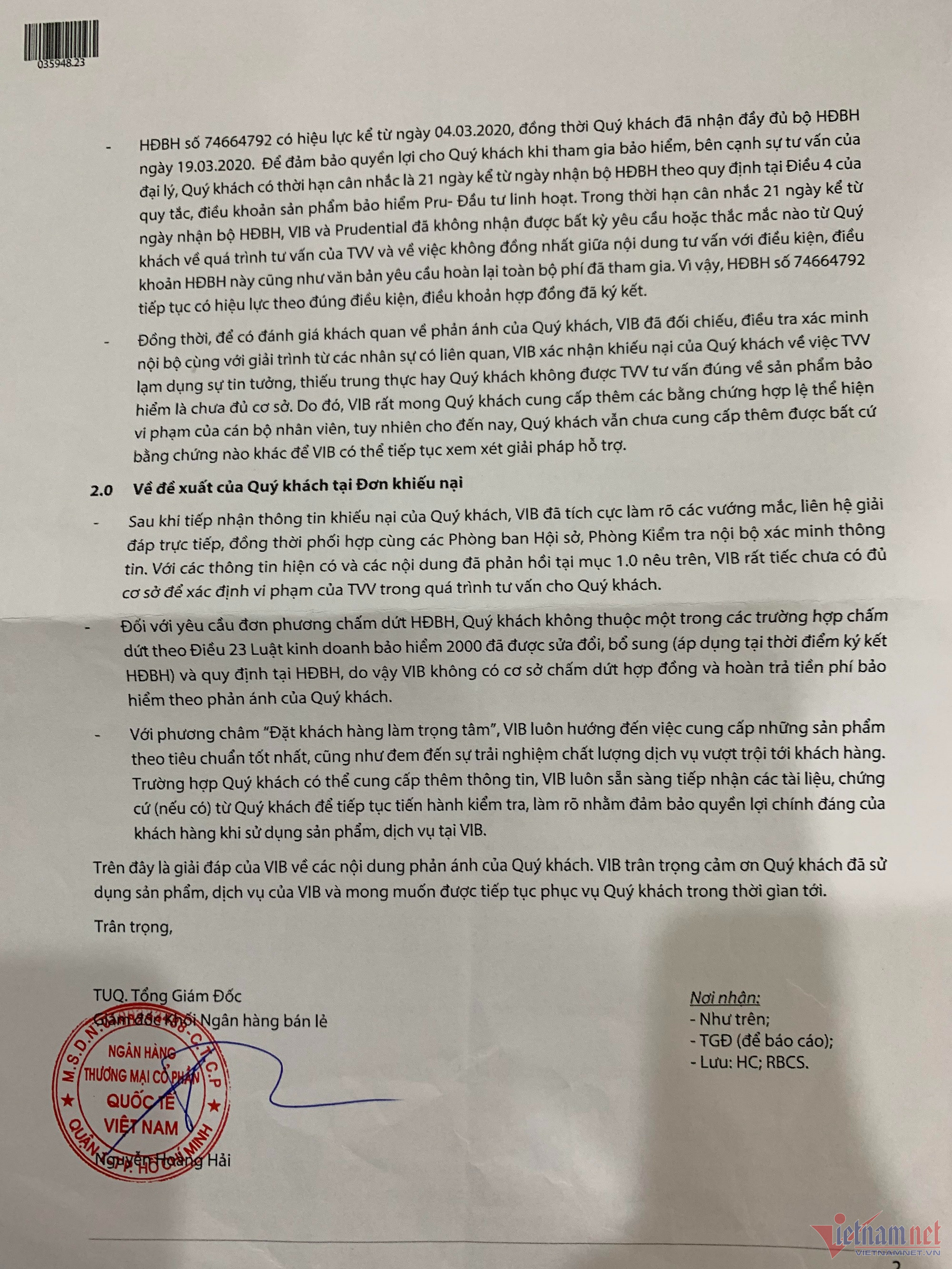

In a response letter to the customer on March 30, VIB stated that Ms. Dao had a 21-day period to consider the contract as stipulated in Article 4 of the terms and conditions of the "Pru-Flexible Investment" insurance product.

However, within 21 days from the date of receiving the insurance contract, VIB and Prudential did not receive any requests or questions from customers about the consultant's consultation process and the inconsistency between the consultation content and the terms and conditions of this insurance contract, as well as the written request for a refund of all the fees paid.

VIB also affirmed that the customer could not provide valid evidence showing the violation of the staff. Therefore, this contract continues to be valid according to the terms and conditions of the signed contract.

Believing that Ms. Phuong was dishonest and abused the trust of customers to advise and sell insurance products that were not true to the nature of the product, Ms. Dao did not agree with VIB's response and continued to request to terminate the "Pru - Flexible Investment" insurance contract and demand a refund of 3 years of paid insurance premiums.

PV. VietNamNet contacted Ms. Nguyen Thi Thanh Thuy, Director of VIB Xa La. Ms. Thuy said that customer Nguyen Thi Bich Dao wanted to close the contract and that request was met. VIB Xa La sent someone to contact Ms. Dao to invite her to come over to do the paperwork. "However, Ms. Dao has not come over to sign the documents yet, so this contract cannot be closed yet," Ms. Thuy said. Regarding the reason for not signing the final contract, Ms. Dao shared that if she agreed to sign the final contract, according to the bank's proposal, she would only receive 23.1 million VND, thus losing nearly 67 million VND in fees already paid. Meanwhile, VIB's communications department said it will check information from relevant departments about the case of customer Nguyen Thi Bich Dao. VietNamNet will continue to inform readers about the incident. |

Source

![[Photo] Prime Minister Pham Minh Chinh chairs the 16th meeting of the National Steering Committee on combating illegal fishing.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/10/07/1759848378556_dsc-9253-jpg.webp)

![[Photo] Super harvest moon shines brightly on Mid-Autumn Festival night around the world](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/10/07/1759816565798_1759814567021-jpg.webp)

Comment (0)