Who is the partner buying real estate at 191 Ba Trieu?

According to the Draft Restructuring Plan associated with bad debt settlement for the period 2021-2025 just announced by Techcombank , the bank said it is correcting and editing according to the recommendations in Inspection Conclusion No. 95/KL-Cúc I.2.m and No. 1930/KL-Cúc I.2.m of the State Bank.

Techcombank said that it has basically completed the recommendations stated in the inspection conclusion, except for some recommendations such as:

Regarding the investment proposal for Vincom Tower B, 191 Ba Trieu, Hanoi , basement B1, B2, part of the first and second floors of Vincom commercial area, 191 Ba Trieu (Real estate 191 Ba Trieu), according to this bank, after Techcombank moved its headquarters from 191 Ba Trieu, Hanoi to 6 Quang Trung, Hanoi , Techcombank AMC (a subsidiary of Techcombank on debt management and asset exploitation) has actively sought partners to transfer this real estate.

As a result, the Company has found a partner, Truong Thinh Company, and the two parties are actively completing the transfer of the real estate at 191 Ba Trieu.

Regarding the real estate at 191 Ba Trieu, in 2011 Techcombank bought this property from Vingroup Corporation of Chairman Pham Nhat Vuong for a price of VND1,044 billion. (The bank later moved its headquarters to this address after selling the old headquarters at 72 Ba Trieu to VietBank for about VND390 billion).

Although it is negotiating with its partner, Truong Thinh Company, Techcombank's financial report for the first quarter of 2023 recorded revenue from the sale of investment real estate in the first quarter of 2023 of VND 1,775 billion, while in the first quarter of 2022, the bank did not record this revenue.

This revenue is said to come from Techcombank selling the real estate at 191 Ba Trieu, thereby recording a profit of 730 billion VND.

In early 2023, Techcombank officially moved to its new headquarters at 6 Quang Trung, Hoan Kiem District, Hanoi. However, the bank has never officially announced the transfer of the 191 Ba Trieu real estate or the partner who bought this property.

Individual customers borrowing to buy real estate have income from 1.3 billion VND/year

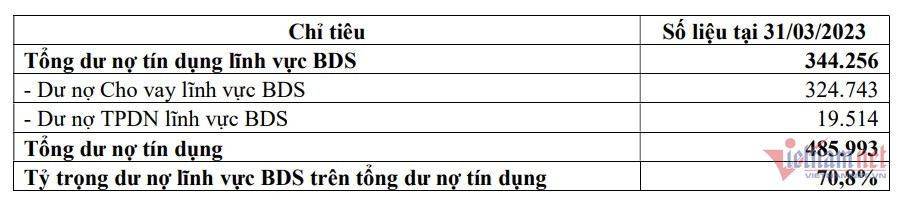

Regarding the shortcomings in real estate credit activities, Techcombank said that as of March 31, 2023, outstanding real estate loans were VND 344,256 billion, accounting for up to 70.8% of the bank's total outstanding credit.

Of which, outstanding loans in the real estate sector are 324,743 billion VND, outstanding corporate bonds in the real estate sector are 19,514 billion VND.

For customers who are businesses and project investors, the bank said it mainly provides credit to businesses and investors to develop apartment and urban areas to serve the needs of people in large cities such as Hanoi and Ho Chi Minh City.

Techcombank provides credit to the real estate sector according to the value chain, also known as the “ecosystem”. Accordingly, the Bank prioritizes providing credit according to a closed chain from investors, to contractors and final home buyers.

For homebuyers, Techcombank's homebuyer customer portfolio is highly differentiated, focusing mainly on customers borrowing to buy projects with reputable investors or residential real estate in locations 1-2-3 in major cities.

Customers borrowing to buy houses at Techcombank are mainly those with a total income of over 1.3 billion VND/year, this group accounts for 90% of total outstanding loans for home buyers.

With the above credit orientation for homebuyers, the bad debt ratio for the individual customer segment borrowing to buy houses and real estate at Techcombank is relatively low at the end of the first quarter of 2023 (approximately 0.36%).

Techcombank affirms that it always focuses on implementing post-loan control to ensure credit safety and minimize bad debt ratio. This includes establishing post-control departments, compliance control departments, and early detection and warning departments. Customers are subject to post-control in accordance with credit management procedures on a monthly or quarterly basis based on risk classification.

In addition, the business unit also conducts monthly/quarterly post-loan control, including: visiting customers; on-site inspection of collateral; on-site inspection of projects; checking documents on capital use purposes; collecting information from third parties; collecting financial and legal records of customers...

Periodically, the unit conducts an overall assessment of the customer's credit situation after the loan, including: updating analysis and assessment of the situation, business, finance, financed plan, cash flow, collateral situation, risk indicators EL/ECL, RWA... to assess the customer's ability to fulfill financial obligations.

Source

Comment (0)