As of April 17, 2024, MCH is trading on the Upcom floor with a closing price of VND 138,900, equivalent to a market capitalization of nearly VND 100,000 billion (USD 4 billion). 93.7% of MCH's equity is held by its parent company Masan Consumer Holdings, with an average trading volume of 10 sessions of this stock being about 58,500 units.

According to newly released information from MCH's General Meeting of Shareholders documents, the company also increased the cash dividend to 100% (1 share receives 10,000 VND), having previously advanced 45% and will pay the remaining 55% in 2024.

A recent analysis report by HSBC assessed that moving the floor to HOSE will help MCH shares have higher liquidity.

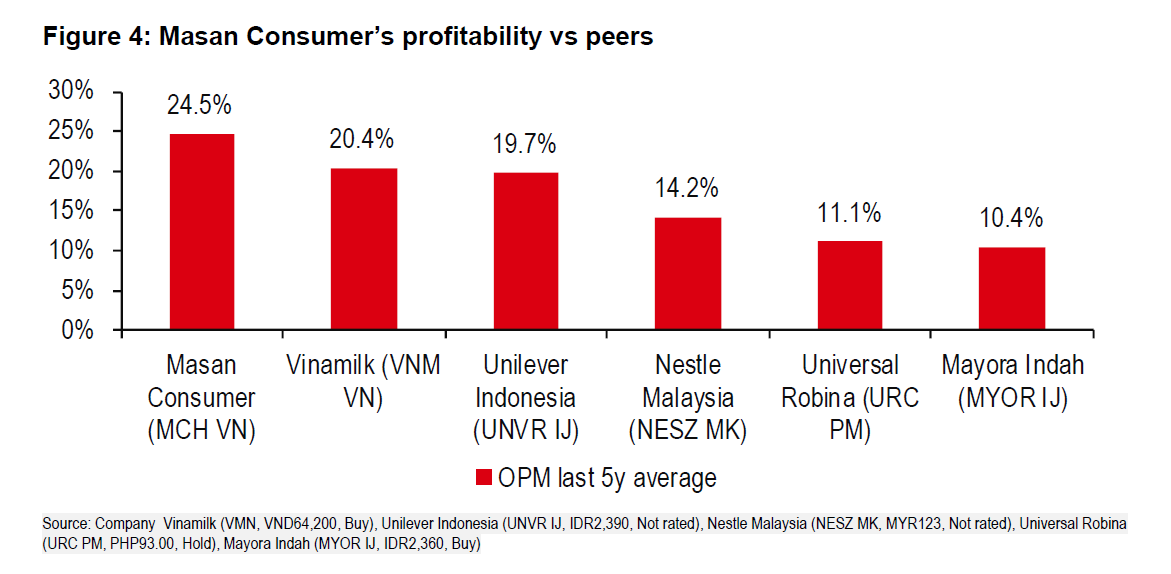

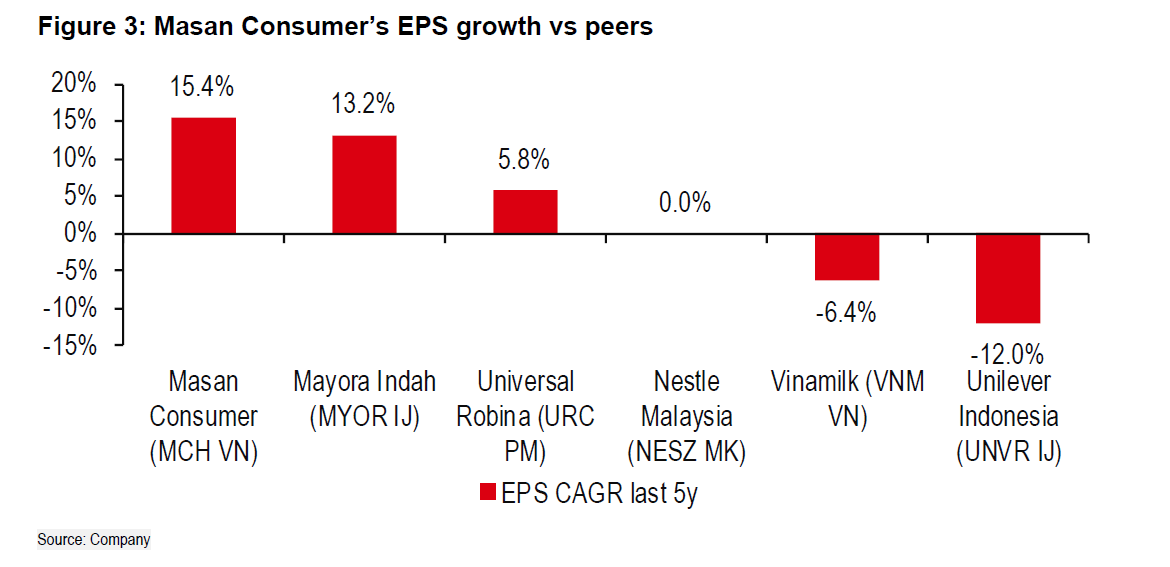

HSBC assessed that Masan Consumer has a "record" of high profit margins, stable revenue growth and significantly outperforms its peers in the FMCG and packaged food sectors in the region.

Masan Consumer has recorded phenomenal growth since 2018. In 2023, the company set a new record profit when recording a profit after tax of VND 7,195 billion, an increase of 30% compared to 2022. EPS in 2023 reached VND 9,888/share, a sharp increase compared to EPS in 2022 of VND 7,612/share.

In addition, for Masan's retail segment, HSBC believes that WinCommerce is in a phase of high capital demand to open new stores and is about to break even. Therefore, listing Masan Consumer is a more reasonable and favorable option for the group. At the same time, this move is also one of the steps to prepare for the strategy of optimizing the value of Masan's unified retail consumer platform, The CrownX (the unified platform of MCH and WCM).

With WinCommerce EBITDA increasing, lower cash needs, and reduced benefits in non-core consumer businesses, Masan Group will significantly reduce financial pressure.

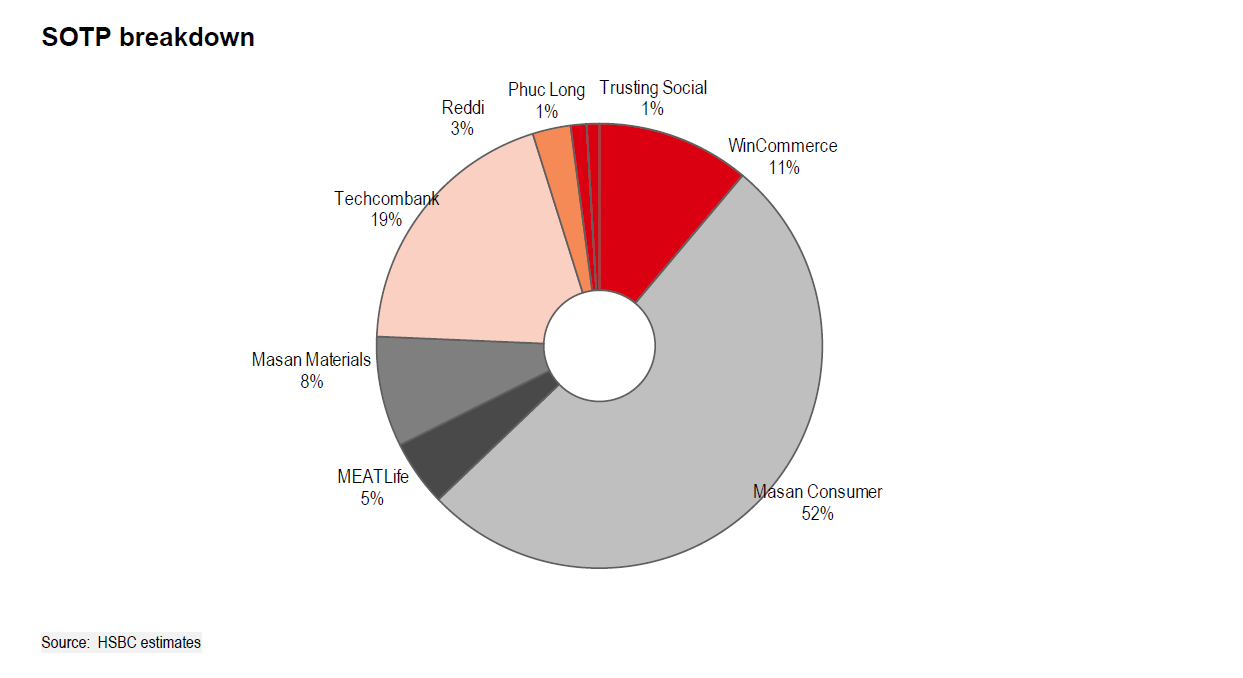

According to data as of April 17, Masan Consumer's market capitalization of $4 billion is higher than that of Masan Group (stock code MSN). Meanwhile, according to the SOPT valuation method (sum of component values), HSBC values Masan Consumer at 52% of Masan Group's value.

Some domestic analysis reports also positively assess MSN's prospects. BSC Securities Company expects the consumer segment in 2024 to continue to be the main growth segment by implementing the premiumization trend combined with the "Go Global" strategy, optimizing inventory and operating costs, while effectively exploiting the WIN membership program to create value for the ecosystem.

BSC assesses that the risks related to the settlement of due debts and the pressure to pay due debts are no longer large for MSN in 2024, thanks to the core consumer sector's operations approaching efficiency, MSN's financial leverage reduction strategy in 2024 and the expectation that the FED's monetary easing policy will be implemented in the second half of 2024, which will affect USD loans.

At WinCommerce, the new store model is gradually proving its effectiveness and continues to expand in number, while improving profit margins by exploiting private label lines, optimizing costs and benefiting from reduced depreciation costs.

According to the financial report of the fourth quarter of 2023 of Masan Group, this enterprise currently owns nearly 17,000 billion VND in cash and bank deposits. Masan's Free Cash Flow (FCF) has improved to 7,454 billion VND in 2023, a significant increase compared to 887 billion VND in 2022.

Cash and cash equivalents are expected to increase by nearly VND7 trillion after the equity investment led by Bain Capital, and cash dividends received from MCH and TCB ( Techcombank ), bringing the total amount the group can hold to USD1 billion in the near future.

In the latest update, with Masan's clear prospects, HSBC raised its target price for MSN shares to VND98,000/share.

Bean Linh

Source

![[Photo] National Assembly Chairman Tran Thanh Man visits Vietnamese Heroic Mother Ta Thi Tran](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/7/20/765c0bd057dd44ad83ab89fe0255b783)

Comment (0)