New high-end supply is well received.

According to Savills Prime Office Costs report for Q3 2023 on global office costs, the outlook for premium office markets is challenging due to sharply rising costs and declining occupancy rates. However, in Vietnam, the Ho Chi Minh City office market still recorded encouraging results in the second half of 2023.

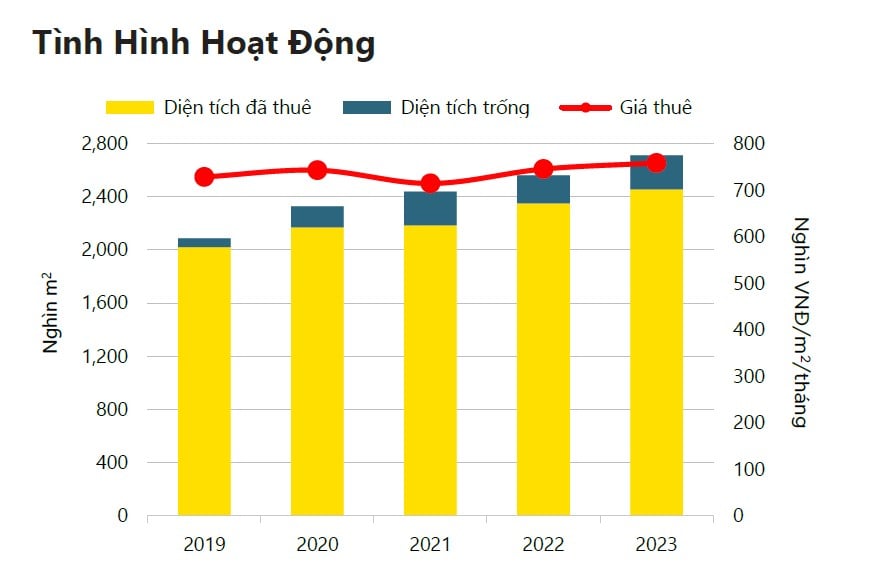

In 2023, the overall market supply continued to increase. Class A properties contributed significantly with a 68% year-on-year increase, welcoming three new projects along with three upgraded Class B properties.

Savills' Ho Chi Minh City real estate market report for Q4/2023 also shows that supply increased by 3% quarter-on-quarter and 6% year-on-year, reaching 2.7 million square meters of net leasable area (NLA). In the second half of 2023, Savills recorded many office leasing transactions from the Finance, Insurance, and Real Estate (FIRE) sector in the high-quality building segment.

The performance of the Ho Chi Minh City office market segment in 2023.

According to Ms. Lai Thi Nhu Quynh, Deputy Director of Commercial Leasing Services at Savills Ho Chi Minh City, this signal indicates a positive reception from tenants for high-end office spaces and a tendency to choose areas near the city center. In particular, the Thu Thiem area is a bright spot attracting significant interest from tenants due to its high-quality, large-scale spaces and competitive rental prices.

"At the same time, businesses that had planned to expand their offices beforehand have also found many suitable options recently, with diverse new supply sources in various areas of the city. This shows a greater sense of confidence among businesses when relocating offices during this challenging period," the expert added.

Ms. Lai Thi Nhu Quynh, Deputy Director of Commercial Leasing Services, Savills Ho Chi Minh City

Occupancy rate is nearly 90%.

In Q4 2023, rental rates increased by 1% quarter-on-quarter and 5% year-on-year to VND 779,000/m2/month with a high occupancy rate of 89%, a decrease of 1 percentage point quarter-on-quarter and 4 percentage points year-on-year.

Neil MacGregor, Managing Director of Savills Vietnam, said: "The Vietnamese office market is bucking the global industry downturn and maintaining high occupancy rates with stable rental price growth. Ho Chi Minh City is emerging as one of the best-performing office locations in the Asia Pacific region due to strong demand and still limited supply relative to its economic growth potential."

The quarter's net office space (NLA) reached 38,000 m2, primarily driven by new Grade A and C projects. Grade A projects accounted for 66% of the absorption, with tenants from the banking and IT sectors, while Grade C projects accounted for 19%, with new contracts from businesses in the distribution sector. Savills' 2023 transaction survey also showed that office space expansion transactions accounted for 74% of the total transaction area.

Tenants in the Finance, Insurance, and Real Estate sectors prefer high-quality projects and tend to relocate to areas outside the city center. Meanwhile, tenants in the IT and Distribution sectors prioritize projects with competitive rental rates. New office openings accounted for 15% of leased space, with foreign businesses accounting for 74% of transactions and favoring Grade A and B projects; domestic businesses opted for Grade C and accounted for the remaining 26%.

Class A office space remains in high demand.

“During the process of supporting clients, Savills Ho Chi Minh City Office Leasing Service has observed that tenants are increasingly gravitating towards new, high-end buildings that meet sustainable development standards, green certifications, and wellness features. Sectors such as finance and manufacturing remain the main tenants driving the market amidst economic volatility,” Ms. Quynh stated.

According to Savills, 10 projects with 142,000 m2 of NLA are expected to enter the market in 2024. The Ho Chi Minh City Center for Human Resource Demand Forecasting and Labor Market Information also stated that businesses in the FIRE, IT, and Distribution sectors will continue to expand in 2024. Strong demand will drive the market to maintain high and stable capacity.

By 2026, approximately 70% of future supply from Grade A and B projects will have green certifications such as Green Mark and LEED. Based on supply and future economic prospects, rental rates are expected to decrease slightly by 1% annually during the 2024-2026 period.

Source

![[Image] Close-up of the newly discovered "sacred road" at My Son Sanctuary](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F13%2F1765587881240_ndo_br_ms5-jpg.webp&w=3840&q=75)

Comment (0)