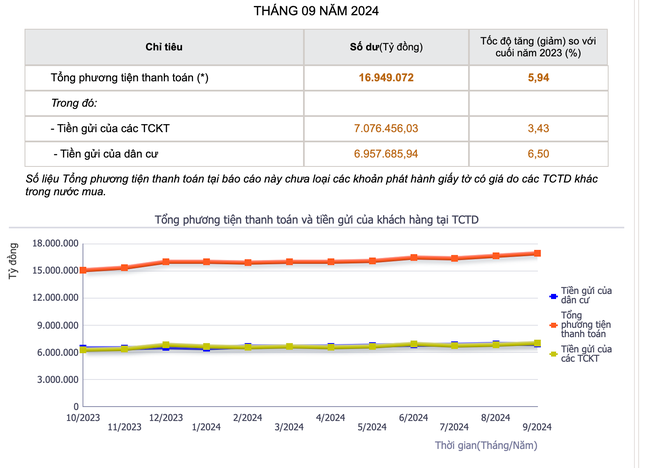

On November 2, the State Bank announced the latest data on customer deposits at credit institutions up to September 2024.

Accordingly, by the end of September, deposits of economic organizations reached more than 7.07 million billion VND, up 3.43%; deposits of residents reached more than 6.95 million billion VND, up 6.5% compared to the end of last year.

Compared to the end of last month, deposits of economic organizations increased by more than VND238,000 billion while deposits of residents increased by more than VND32,700 billion.

|

| People's and organizations' deposits in banks have increased continuously from 2023 to present (photo: Ngoc Mai). |

In general, in September alone, on average, more than 9,000 billion VND of idle money flowed into the banking system every day.

Thus, idle money from residents and businesses flows into the banking system in the context of recently rising interest rates.

In fact, the amount of savings of people and businesses deposited in banks has increased over the past 2 years, even though the mobilization interest rate over the past year has been at a record low, at times averaging only 3% - 4%/year.

Regarding the deposit interest rate developments in the market applied at the beginning of December, some banks with small market shares increased slightly by 0.1 - 0.2%/year, depending on the term, compared to the previous month. Currently, the average mobilization interest rate is about 6%/year for long terms of 12 months or more. Short-term savings interest rates also increased to 4 - 5%.

According to economic expert Dinh The Hien, savings will still be a safe "shelter" for cash flow at present when looking at the amount of money deposited in banks.

This is an investment channel for everyone and you can sleep soundly because in any situation, your deposits are always guaranteed to be safe in the banking system. On the other hand, a series of banks are also adjusting their savings interest rates to increase in many terms to attract deposits after a long period of keeping them at low levels.

Although it is the most promising investment channel, interest rates are not the only competitive factor. In addition to interest rates, banks compete with safe and convenient services, optimizing customer experience, and personalizing for each customer group. At the same time, they actively apply modern technologies to digitize products and services, diversify deposit products flexibly, and integrate many other accompanying services, only then can they retain cash flow with the bank.

Economist Dinh Trong Thinh commented that for many people, deposits are still considered a "stable" investment channel, with low interest rates but relatively safe, while in other investment channels, some require expertise and analytical ability such as stocks, while others require large investment rates such as real estate.

According to Mr. Thinh, with a 12-month term interest rate of 5-6%/year, investors are still guaranteed not to suffer too much.

With the current situation of increasing deposits from the population flowing into the banking system, outstanding credit balances at some banks are gradually becoming active again, and savings interest rates are forecast to increase slightly in the coming time.

Previously, Deputy Governor of the State Bank Dao Minh Tu said that people's and organizations' deposits in banks are all converted into credit for the economy, and there is no such thing as money being left idle in banks.

Source: https://baodaknong.vn/moi-ngay-nguoi-dan-gui-9-000-ty-dong-vao-ngan-hang-235956.html

![[Maritime News] More than 80% of global container shipping capacity is in the hands of MSC and major shipping alliances](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/7/16/6b4d586c984b4cbf8c5680352b9eaeb0)

Comment (0)