|

Credit rebounds, banks begin to increase savings interest rates

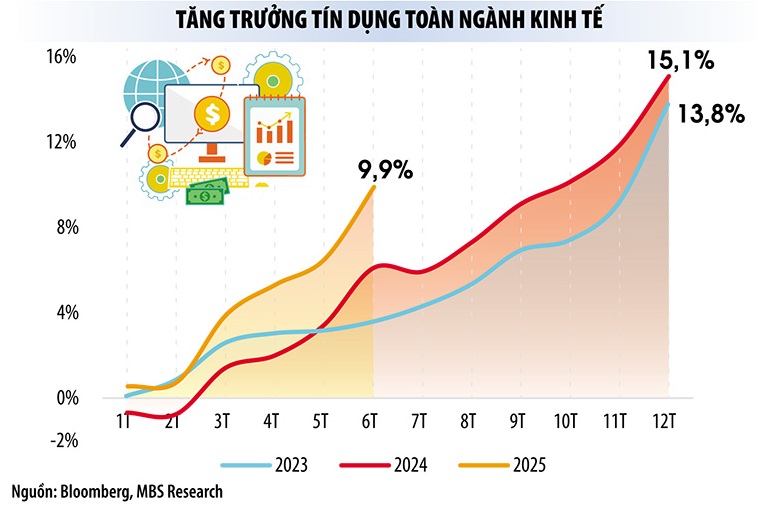

The government has adjusted the GDP growth target this year to 8.3-8.5% to create a foundation for achieving double-digit growth in the coming period. To achieve this target, according to experts' calculations, credit will have to increase by 17-18%. A report by the State Bank of Vietnam (SBV) shows that credit in the first 6 months of the year increased by nearly 10% - the highest level since 2022. Thus, the possibility of credit growth of 16-17% this year is completely feasible.

According to the business results report for the first half of this year, many banks have very strong credit growth rates, such as LPBank increased by 11.2%, KienLongBank increased by 13.2%, VietinBank increased by 10%, Vietcombank increased by over 11%, NCB increased by 22%, TPBank increased by 11.7%, NamABank increased by 14.7%... Capital mobilization of banks also increased very strongly, such as NCB increased by nearly 20%, KienLongBank increased by 15.2%, NamABank increased by more than 22%...

Many bank leaders said that the growth rate of capital mobilization in the first half of this year increased 5-6 times compared to the same period last year. Banks are stepping up capital mobilization not only to serve the credit growth demand in the first half of the year, but also to prepare capital sources to serve the high capital demand in the second half of the year.

Economists warn that if credit increases by 18%, banks will pump an additional VND3 trillion into the economy this year. This figure will not cause an asset bubble, nor put pressure on interest rates and inflation, if capital flows into priority sectors. On the contrary, if credit flows into speculative sectors such as stocks, real estate, etc., an asset bubble may form.

According to statistics from the Vietnam Banking Association, since the beginning of July 2025, many banks have increased savings interest rates. A survey by Dau Tu Newspaper also shows that recently, many banks such as VPBank, VCBNeo, Techcombank, SeABank, LPBank, etc. have increased deposit interest rates for many terms. With online deposits, the preferential interest rate that customers receive can be up to 1% higher than the normal interest rate.

Currently, the interest rate for 6-month savings at many banks is up to over 6%/year. Deposits worth thousands of billions of VND can be paid interest rates of up to over 9%/year.

In the interbank market, overnight lending rates remained above 5%, at times soaring to nearly 7%/year at the end of June 2025 when liquidity demand increased. Last week, the SBV net injected more than VND58,400 billion into the system.

According to experts, in the second half of 2025, cash flow will shift from defense to investment, and risky investment channels will take the lead. Outstanding loans to securities companies by the end of the second quarter of 2025 are estimated at VND300,000 billion - a record high - demonstrating the shift in cash flow. In this context, although it is difficult for interest rates to increase sharply under the guidance of the Government and the State Bank, experts believe that interest rates will face a lot of pressure.

Credit demand increases: Banks are happy and worried

High credit growth has led to improved bank profits. However, the issue of risk and growth still worries the State Bank and commercial banks.

According to Mr. Luu Trung Thai, Chairman of the Board of Directors of MB Bank, in order for credit to grow in the right direction and target, the Government needs to have solutions to promote public investment to spread to the private economic sector; solve problems in the real estate market; restructure the corporate bond market. In addition, the State Bank must adhere to the goal of stabilizing the macro economy and controlling inflation; increasing credit supply and maintaining low lending interest rates...

If capital flows into priority sectors, this year's credit only needs to increase by about 17% to meet the GDP growth demand of 8.3 - 8.5%. However, when credit flows into speculative sectors such as securities, real estate, etc., credit must increase by over 20% to achieve the above GDP growth target.

If capital flows into priority sectors, this year's credit only needs to increase by about 17% to meet the GDP growth demand of 8.3 - 8.5%. However, when credit flows into speculative sectors such as securities, real estate, etc., credit must increase by over 20% to achieve the above GDP growth target.

- Associate Professor, Dr. Nguyen Huu Huan (Ho Chi Minh City University of Economics)

Meanwhile, Mr. Phan Duc Tu, Chairman of BIDV Board of Directors, said that the Government and ministries and sectors need to continue to direct the development of a more synchronous and balanced financial market and capital market. This is to increase the ability to supply capital to the economy and create conditions for credit institutions to focus on providing short-term capital and performing banking services. At the same time, continue to strengthen the capacity and safety supervision of banks.

According to the State Bank of Vietnam, by the end of 2024, Vietnam's credit balance/GDP ratio will be 134%, among the highest in the world, showing that the economy is overly dependent on credit. This year's credit growth target is 16%, but the State Bank of Vietnam is ready to flexibly adjust it in an upward direction if inflation is under control. However, the agency believes that prolonged dependence on credit poses systemic risks and warns commercial banks to pay attention to liquidity in the second half of the year.

“In the last 6 months of the year, credit demand often increases, so banks need to focus on liquidity management, ensuring liquidity and ensuring payment in all situations. The State Bank is ready to stand side by side with the banking system to ensure liquidity supply in the system,” Deputy Governor of the State Bank Pham Thanh Ha pledged.

According to economic experts, in the context of the banking system having to increase capital injection into the economy to support growth, the possibility of further interest rate reduction in the second half of this year is very difficult, especially when interest rates and exchange rates are both under great pressure.

With inflation under control as it is now, the possibility of stabilizing interest rates despite credit growth of 17-18% is feasible. However, many uncertain external factors such as tariff policies, the US Federal Reserve's (Fed) interest rate policy, exchange rates, oil prices, geopolitical tensions, etc. will make inflation in the second half of the year unpredictable. Therefore, the monetary easing of the State Bank in the coming time depends not only on the domestic situation, but also on developments in the global financial market.

In the short term, credit will have to shoulder the heavy responsibility of supporting growth. However, in the long term, experts recommend that Vietnam needs to shift to growth models that rely more on productivity and technology rather than capital. Regarding capital, there must be effective strategies and solutions to develop the capital market and reduce dependence on credit.

Source: https://baodautu.vn/ngan-hang-tang-toc-bom-von-lai-suat-huy-dong-chiu-suc-ep-d338231.html

Comment (0)