Stock market outlook for the week of March 25-30: Short-term investors may consider taking profits.

In terms of momentum, the money flow could continue to push the market past the short-term peak of 1,280 points. This is also the point where FOMO (fear of missing out) money flows are expected to reach a high level.

The stock market moved within a wide range last week, accompanied by a sharp increase in liquidity, with the VN-Index approaching the strong resistance level around 1,280 points.

Despite experiencing a volatile start to the week, falling nearly 50 points from 1,270 to 1,220, the VN-Index then recovered to 1,240 with record-high trading volume of nearly 48,000 billion VND. In the remaining trading sessions, the VN-Index rebounded strongly, surpassing the 2023 peaks of 1,245 and 1,255 points, and exceeding the highest price of two weeks prior around 1,275 points.

At the end of the week, the VN-Index rose 1.43% to 1,281.80 points and began to approach the price level around 1,295 points, corresponding to the highest price in August 2022.

During the week, liquidity on the HoSE reached VND 151,877.51 billion, a sharp increase of 20.4% compared to the previous week. This was a record-breaking trading week in terms of liquidity, averaging over VND 30,000 billion per session, with a trading volume of over 1.1 billion shares per session, only slightly lower than the highest trading week in history on November 19, 2021.

Foreign investors significantly increased their net selling on the HoSE, with a value of VND 3,177.47 billion; while they made net purchases on the HNX, with a value of VND 90.65 billion.

Positive sentiment spread across most sectors. Particularly, banking, real estate, and steel/galvanized sheet metal all saw good gains. More specifically, banks were the driving force behind the market's recovery after a sharp decline, surpassing their 2023 peaks, with strong liquidity, notably TCB (+8.45%),VIB (+7.56%), MBB (+5.25%), BID (+3.83%)..., while NAB (-2.13%), ABB (-1.22%), SSB (-1.11%)...

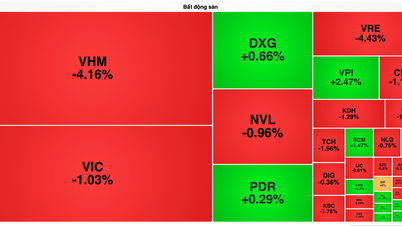

Real estate stocks were also a major driving force last week, with many stocks experiencing strong price increases, surpassing their recent peaks, and trading volume surging. Notable examples include HPX (+37.18%), DIG (+12.11%), PDR (+12.10%), TCH (+12.03%), DXG (+8.47%)..., while some stocks faced downward pressure such as VRC (-12.33%), IJC (-3.98%), KOS (-3.78%), HD6 (-3.17%)... Industrial real estate and rubber stocks showed more divergence; besides D2D (+17.50%), KBC (+6.25%), PHR (+4.40%)... which saw positive price increases, most experienced significant downward pressure after a period of strong gains outperforming the overall market, such as DTD (-5.48%), TIP (-4.63%), GVR (-3.90%), SZC (-3.78%)...

The market received several important pieces of news this week, including: the US Federal Reserve (Fed) keeping interest rates unchanged at 5.25%-5.5%, with three planned cuts of 0.25% this year; the Bank of England deciding to keep interest rates at 5.25%; the Bank of Japan raising interest rates for the first time since 2007, ending the world's only negative interest rate policy; and the Swiss Central Bank deciding to cut interest rates. This is the first major central bank in the world to cut interest rates in nine years.

Domestic news, (1) State Bank of Vietnam continues to withdraw a net 15,000 billion VND through treasury bills in the March 21st session, raising the total size to 145,000 billion VND, (2) BIDV and Vietcombank offer private placement of shares to foreign investors.

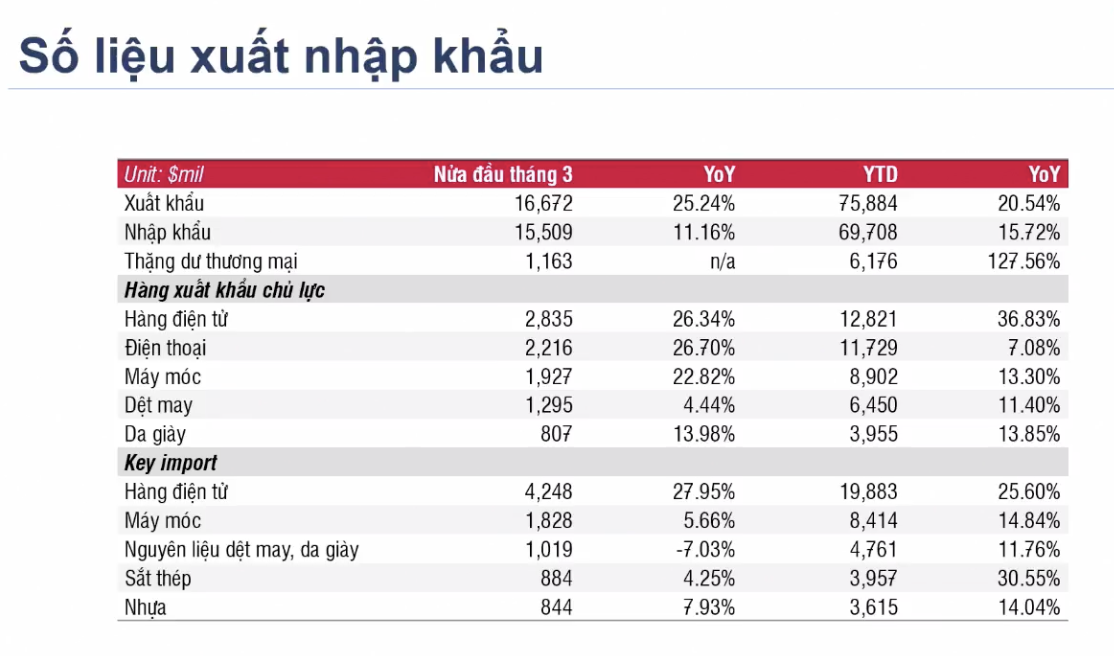

Notable figures from the past week include the recovery of import and export activities in the first half of March 2024 across many sectors, and the cumulative figures for the first half of the year also recorded double-digit growth.

|

The State Securities Commission is seeking opinions from units, organizations, and individuals on the draft amendments and additions to several articles of Circular No. 120/2020/TT-BTC dated December 31, 2020; the State Securities Commission has also consulted its members on the regulation allowing foreign institutional investors to trade without depositing 100% of the funds. If approved and implemented in the near future, this regulation will remove one of the two bottlenecks in the market upgrade process according to FTSE regulations: the pre-trading requirement and the foreign ownership limit (room). Along with the recent trial run of the KRX system by HoSE, it can be seen that regulatory agencies are very active in addressing issues aimed at upgrading the market by 2025, as targeted by the Government.

Looking back at market developments next week, it is highly likely that the market will experience some volatility before continuing its upward trend.

From a technical analysis perspective, DSC Securities Company believes that, in the short term, the general index has broken out of its consolidation box with a candlestick pattern of indecision. However, looking at the breadth of the market, it can be seen that the market still has room for short-term gains as many stock groups are converging to break short-term highs. After successfully overcoming the 1,280-point resistance level, market liquidity is expected to continue to increase sharply . Groups with a high beta relative to the market and good liquidity buffers in recent sessions are preferred for short-term trading (real estate group).

At the end of the week, a large-amplitude pullback candlestick pattern indicates a proactive move to shake out short-term positions, with short-term money flow showing a clear advantage, and the market is expected to continue its short-term upward trend.

The recent upward movement is relatively surprising, given that the trading session two weeks prior saw six major distribution sessions. In terms of momentum, the money flow could continue to push the index past the short-term peak of 1,280 points. This is also the point where FOMO (fear of missing out) is expected to reach a high level. And with a trading base previously assessed as having formed a distribution phase, a bull-trap scenario is entirely possible. DSC maintains that its current upward trend is somewhat unbalanced; the index can rise quickly but can also fall just as quickly.

In conclusion, the sustained short-term cash flow allows investors to resume short-term trading (10-15 sessions). However, there is insufficient basis to assess whether the index has overcome distribution pressure, nor is there sufficient basis to assess the previous technical divergence signals. Investors should prioritize maintaining an average portfolio weighting or actively engaging in short-term trading as recommended.

Experts suggest that short-term investors may consider taking partial profits on stocks that have yielded good returns, while also restructuring their portfolios to focus on stocks in positive upward trends (for example, the securities sector, focusing on large-cap, leading stocks).

For investors with a high cash ratio, they can consider exploratory investments in steel and real estate stocks, prioritizing those that haven't risen much and have good buying zones such as HDG (29-29.4), HPG (29-30)...

Source

![[Photo] Delegation attending the 14th Congress of the Vietnam Trade Union visits the Mausoleum of President Ho Chi Minh.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/06/03/1780451842301_ndo_br_img-3824-jpg.webp)

Comment (0)