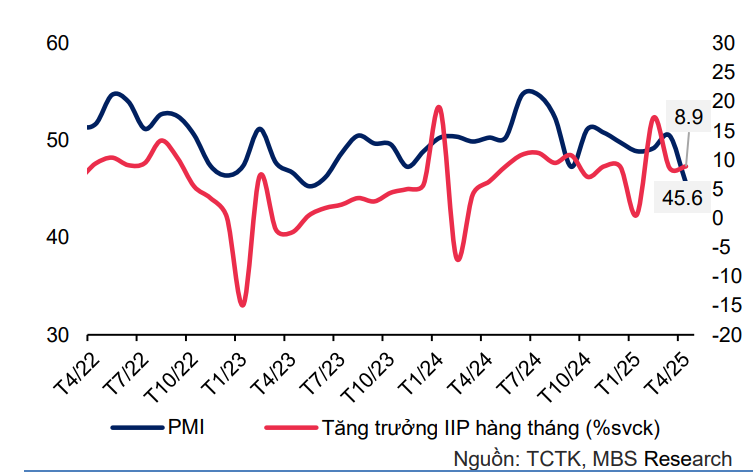

Tariff uncertainty causes manufacturing to decline sharply

MBS's report pointed out that the increase in new orders in March helped manufacturing activities continue to maintain growth in April. The industrial production index (IIP) in April increased by 1.4% compared to the previous month and increased by 8.9% y-o-y, with a large contribution coming from the 10.8% y-o-y growth of the processing and manufacturing industry.

In particular, key industries recorded strong growth in production activities in the month including: Production of coke, refined petroleum products (+47.2% yoy), production of motor vehicles (+27.6% yoy), production of rubber & plastic products (+18.6% yoy). In 4M2025, the production index of the entire industry is estimated to increase by 8.4% yoy. In particular, the processing and manufacturing industry achieved a growth rate of 9.5%, much higher than the 6.3% of the same period in 2024.

However, MBS said that the growth momentum of industrial production is likely to be hampered in the coming time as the new US tariffs caused the number of new orders in April to shrink at the fastest and sharpest rate in nearly two years. After the US announced the reciprocal tariffs, output, new orders, employment and purchasing activity all fell sharply.

In particular, new export orders continued to contract for the sixth consecutive month, with the sharpest decline since June 2023, pointing to challenges for export activities in the coming months. Accordingly, the Vietnam Manufacturing PMI in April hit a two-year low of 45.6 points, down from 50.5 points in March, signaling a significant deterioration in the state of the industry. In addition, the possibility of further disruption to the manufacturing sector due to tariffs pushed business confidence to a 44-month low.

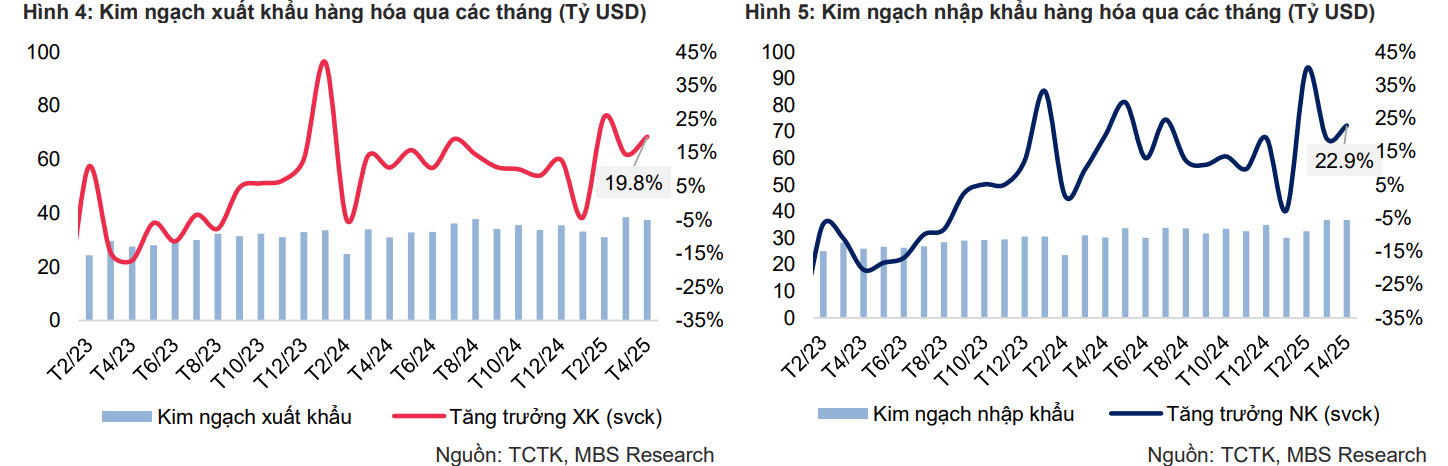

Trade activity was buoyant in April, but challenges lie ahead

Export turnover in April reached 38.51 billion USD (+19.8% yoy), driven by a number of high growth items such as: Toys, sports equipment and parts (+110.3% yoy); textile fibers and yarns (+99% yoy); electronics, computers and components (+58.7% yoy). However, compared to the previous month, export turnover decreased by 2.8%, partly reflecting the initial impact of the reciprocal tax on the supply chain and the decrease in international customer demand after boosting purchasing activities in previous months to build up reserves before the reciprocal tax rate was announced.

In the first 4 months of 2025, the export turnover reached 140.34 billion USD (+13% yoy), with many items having high growth rates such as: Toys, sports equipment and parts (+83.6% yoy); coffee (+51.8% yoy); electronics, computers and components (+36.2% yoy). On the contrary, some items recorded large negative growth rates such as: iron and steel (-23.1% yoy); cameras, camcorders and components (-19% yoy); plastic raw materials (-16.3% yoy). In terms of export markets, the United States is Vietnam's largest market with an estimated turnover of 43.4 billion USD (+25.1% yoy). Exports to the EU increased by 12.8% yoy, reaching 18.5 billion USD, while exports to China reached 18.1 billion USD (+2.1% yoy).

On the other hand, import turnover remained almost unchanged compared to the previous month with an estimated value of 36.87 billion USD (+22.9% yoy) in April, and the accumulated value in the first 4 months of the year reached 136.55 billion USD (+18.6% yoy). Of which, China is our country's largest import market with an estimated turnover of 53.2 billion USD (+26.5% yoy). In the first 4 months of 2025, there were 2 imported items with a value of over 5 billion USD (accounting for 44.3% of total import turnover) including: Electronics, computers and components; machinery, equipment, tools and other spare parts.

In the context of the global economic situation facing many fluctuations revolving around unpredictable tariff policies from the US as well as the US-China trade tensions, Vietnam's export activities will certainly be affected to some extent as a highly open economy. However, the extent of the impact is still unclear as there is no information about the final tax rate applied to Vietnamese goods this year. Therefore, MBS experts are still monitoring developments in the content of negotiations in the coming time to adjust growth prospects accordingly.

Exchange rate pressure persists despite sharp decline in DXY index

Although the DXY index has fallen sharply by 9.7% from its peak in 2025, the interbank USD/VND exchange rate remained high in April. The high exchange rate is partly due to the following factors: First, in April, the State Treasury continued to buy USD from commercial banks with a total value of 110 million USD, which also tightened the foreign currency supply. Second, in the context of the trade situation facing many uncertainties related to unpredictable tariff policies from the US, businesses' demand for foreign currency tends to increase. Finally, the sharp drop in interbank interest rates to a 13-month low at the end of the month caused the VND-USD interest rate gap to reverse to the negative level at the highest level since the beginning of the year.

The above factors have put significant pressure on the exchange rate. Accordingly, the interbank exchange rate increased by 1.4% compared to the end of March to 25,994 VND/USD (+2.1% compared to the beginning of the year). The exchange rate on the free market increased to 26,470 VND/USD, while the central exchange rate was listed at 24,956 VND/USD, corresponding to increases of 2.8% and 2.5% respectively compared to the beginning of 2025.

MBS expects the exchange rate to fluctuate in the range of VND25,500 – 26,000/USD in 2025 as the new administration’s fiscal easing plans, combined with tighter immigration policies, along with high interest rates and relatively high protectionism in the US, are expected to support the increase in the value of the USD in 2025. In addition, unpredictable tariff policies from the US are expected to create many challenges for Vietnam’s export activities and FDI attraction in the coming time and may put pressure on Vietnam’s already modest foreign exchange reserves after having to sell more than US$9 billion last year.

However, so far, internal factors are still recording positive results such as: trade surplus (~3.79 billion USD in 4M2025), disbursed FDI capital (6.74 billion USD, +7.3% yoy) and recovery of international tourist arrivals (+23.8% yoy in 4M2025). Accordingly, this is expected to continue to support the VND.

Amidst increasing exchange rate pressure, the State Bank of Vietnam (SBV) returned to net liquidity withdrawal in April with an estimated value of nearly VND22.2 trillion. Specifically, the SBV injected about VND220.3 trillion through the OMO channel, with an interest rate of 4% and a term of 7 to 91 days. However, the total amount of capital maturing in the month amounted to more than VND242.4 trillion.

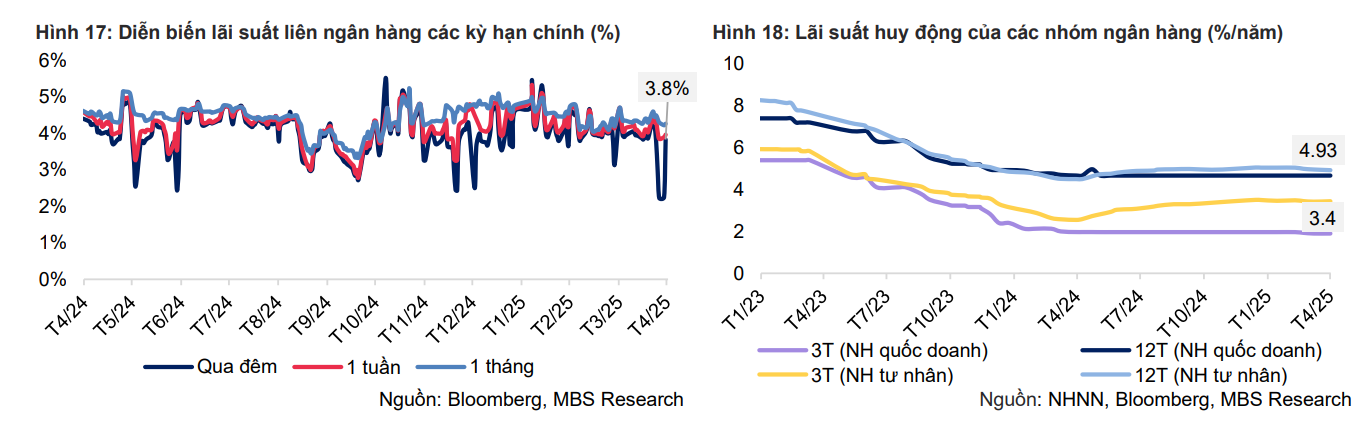

Despite the net absorption moves of the Operator, the overnight interbank interest rate, after remaining around 4% - 4.4% in the first half of April, fell sharply to a 13-month low of 2.2% on April 25 - showing excess liquidity in the system. Accordingly, it has significantly affected the VND-USD interest rate gap and exchange rate pressure. If from the beginning of the year to the first half of April, the USD overnight interest rate was 0.2% - 1.2% higher than the VND, then near the end of the month, this difference increased sharply to 2.1% / year - the highest level since the beginning of the year. By the end of the month, the overnight interest rate was at 3.8%, while interest rates for terms from 1 week to 1 month fluctuated around 3.9% - 4.1%.

Deposit interest rates remain on the decline but the pace has slowed in April

After a series of banks reduced interest rates in the past two months, the average deposit interest rate continued to maintain a downward trend but has slowed down. In April, nearly 10 banks reduced interest rates by 0.1% - 0.5%/year for many terms. On the contrary, the market also recorded a few small and medium-sized private banks increasing input interest rates in the context of positive signs of credit demand recovery.

According to the State Bank of Vietnam, by the end of the first quarter, credit growth of the entire system reached 3.93% - nearly 3 times higher than the same period last year. However, in general, the number of banks reducing interest rates is still dominant. By the end of April, the average 12-month term interest rate of the group of commercial banks had decreased by 12 basis points to 4.93%, while the interest rate of the group of state-owned commercial banks remained at 4.7%.

MBS forecasts input interest rates to fluctuate at 5.5% - 6% in 2025 Although deposit interest rates have been on a downward trend recently, we believe that input interest rates will gradually increase towards the end of the year with the expectation that the economy will grow positively and credit growth will reach or even exceed the set target of 16%. As of the end of March, outstanding credit of the whole system increased by 3.93% compared to the end of 2024 - 2.5 times higher than the increase of 1.42% in Q3/2024, showing that capital demand is gradually recovering.

However, credit growth this year is still forecast to reach 17-18%, driven by the recovery of domestic production and consumption, and the acceleration of public investment disbursement. MBS also forecasts that 12-month deposit interest rates of major commercial banks will fluctuate around 5.5% - 6% in 2025.

Source: https://baodaknong.vn/tang-truong-kinh-te-doi-mat-nhieu-thach-thuc-252728.html

![[Maritime News] More than 80% of global container shipping capacity is in the hands of MSC and major shipping alliances](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/7/16/6b4d586c984b4cbf8c5680352b9eaeb0)

Comment (0)