Illustration photo.

The market next week may be negatively affected by international factors, however the probability of an increase is still there when domestic sentiment and factors support it.

Excited psychology, VN-Index increased beyond record

Global stock markets were divided during the week of October 6-10. While the US market was under strong pressure from the Fed's concerns about inflation, especially the resurgence of tariff tensions between the US and China, the Dow Jones index corrected sharply in the final session and for the week as a whole, it fell -0.9% compared to the previous week; meanwhile, the S&P 500 increased insignificantly.

While the stock markets in Asia and the region are divided. Many markets such as Korea, China, Japan... all increased well, some other markets decreased such as Hong Kong (China), Philippines, Malaysia, Thailand...

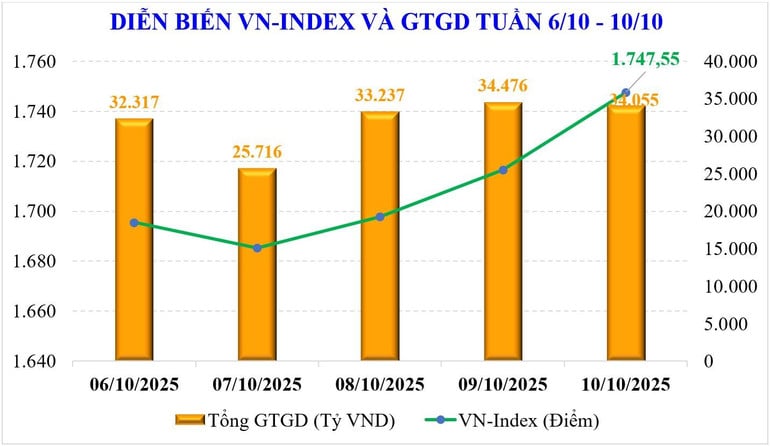

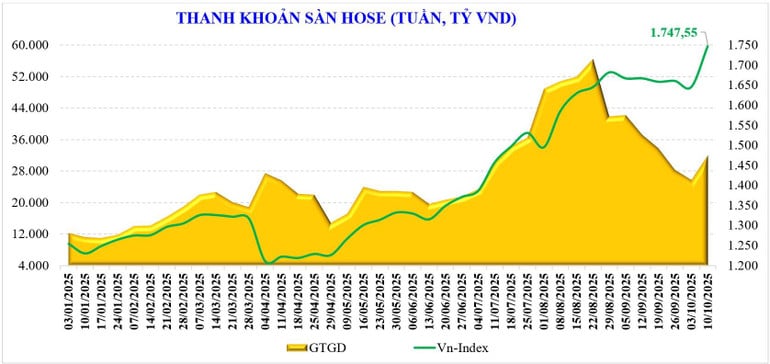

The domestic stock market had a strong week of growth thanks to positive macro information and especially the announcement of FTSE Russell upgrading from frontier market to secondary emerging market. VN-Index surpassed the 1,700 point threshold. At the end of the week, the market stopped at 1,747.55 points, up +101.75 points (+6.18%) compared to the previous week, marking the strongest week of growth since the first week of December 2022.

Bluechip stocks increased strongly, helping the VN30 index increase by +6.51%; the Midcap group also increased by +4.95% - marking the first week of increase after 5 consecutive weeks of decrease; while the Smallcap group only had a slightly higher increase of +1.89%.

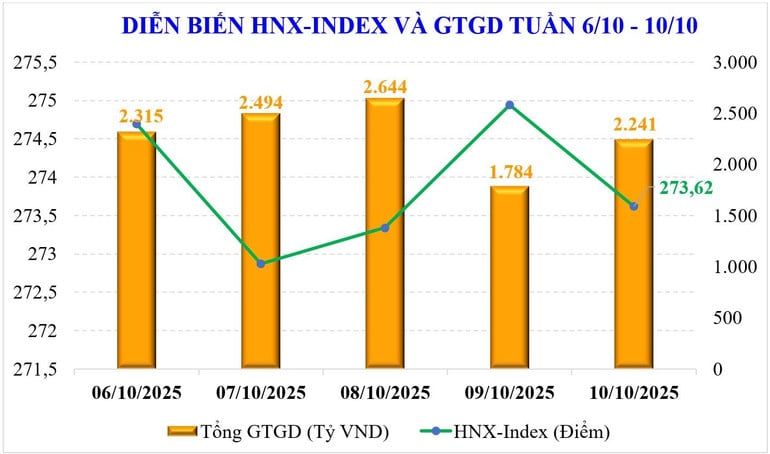

On the Hanoi Stock Exchange, the two main indices also increased quite strongly. Specifically, the VN-Index increased by 2.96%, reaching 273.62 points; and the UPCoM-Index also increased by 2.38%, reaching 111.61 points.

Market breadth recorded a week of broad-based increases, with many stock groups seeing strong increases such as: Vingroup (+14.7%), retail (+6.9%), securities (+6.8%), real estate (+6.4%), construction and building materials (+6.4%)...

Market liquidity increased quite strongly last week. On all three exchanges, the average trading value reached VND34,849 billion/session, up +24% compared to the previous week, in which the matched liquidity also jumped +26% to VND32,065 billion/session.

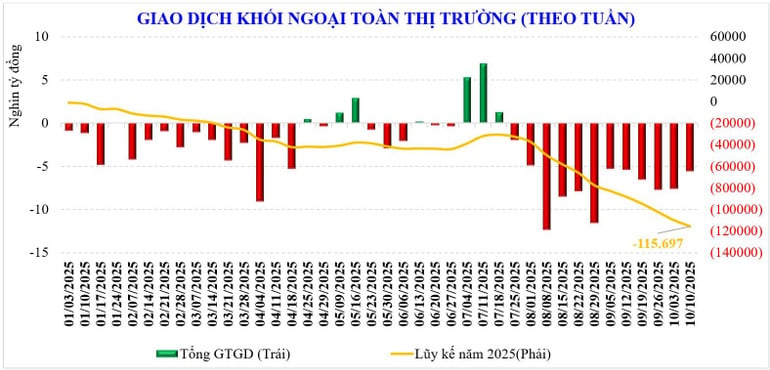

Meanwhile, foreign investors still sold net -5,543 billion VND, and this is the 12th consecutive week of net selling, with a cumulative net sale of -115,697 billion VND since the beginning of the year. Last week, foreign investors net bought: HPG (+817 billion VND), GEX (+506 billion VND), VIC (+359 billion VND); while net selling: VRE (-895 billion VND), MBB (-696 billion VND), MSN (-645 billion VND)...

While foreign investors were net sellers, last week, securities companies' self-trading net bought stocks such as:FPT (+247 billion VND), HDB (+118 billion VND), VPB (+87 billion VND)...; while net selling other stocks such as: HPG (-235 billion VND), VHM (-209 billion VND), GEX (-185 billion VND).

The uptrend may be sustained but slowing down

The domestic stock market had an explosive week. The increase of more than 100 points/week is a new record set since the end of 2022. This also helped the VN-Index reach a historical milestone and is currently the highest level since the market was born.

The market’s rally last week was fueled by strong optimism. At the beginning of the week, the third quarter and nine-month macroeconomic news were released. And more importantly, the market was supported by the upgrade news.

In the new week, the market may see some variables that can affect the market. On the foreign side, although somewhat calm, the tariff tension between the US and China can also affect the cautious sentiment of investors. On the domestic side, the VN30 futures contract expiration session may also be of interest to investors.

However, the market still has positive factors. The market has just ended an exciting week after 1.5 months of sideways trading in the range of 1,600-1,700 points. The cautious sentiment of the past month has been lifted, liquidity has increased again (threshold of 35,000 billion VND), reaching the highest level in the past 3 weeks.

According to statistics, liquidity since the beginning of October increased by +75.5% compared to the same period but decreased by -17% compared to September, to VND 31,178 billion. Accumulated from the beginning of the year, total market liquidity reached VND 28,990 billion, up +37.5% compared to the average level in 2024, and up +31.4% compared to the same period.

Along with that, market breadth shows that stocks have increased across the board but cash flow is strong in the VN30 and Midcap groups, which is also a characteristic of markets starting to enter emerging markets - cash flow focuses on Bluechips instead of penny stocks.

Technically, the VN-Index has successfully broken out of the sideways range (1,600-1,700 points) that has lasted for more than a month with increased liquidity and a leading stock flow, confirming an extended uptrend, heading towards new peaks for the VN-Index. With an increase of +38% since the beginning of the year, technical indicators are very positive, supporting the continued uptrend.

MBS experts believe that, in the base scenario, the market will maintain its upward momentum based on the cash flow directed to Bluechip stocks in the third quarter business results reporting season that is gradually being announced, with the recent GDP growth results, the impact from business results in large stocks is expected to be the leading factor. However, the upward momentum will slow down when the market enters the 1,780 point area.

LONG AN

Source: https://nhandan.vn/thi-truong-chung-khoan-tuan-moi-vn-index-vuot-dinh-sau-nang-hang-co-hoi-tang-van-con-post914944.html

![[Photo] Solemn opening of the 1st Government Party Congress](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/10/13/1760337945186_ndo_br_img-0787-jpg.webp)

![[Photo] General Secretary To Lam attends the opening of the 1st Government Party Congress](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/10/13/1760321055249_ndo_br_cover-9284-jpg.webp)

Comment (0)