|

| As long as the market lacks alternative options within the official asset system, any reforms to the gold market will only address the symptoms, not the root cause. |

Ask the right questions when amending Decree 24/2012/ND-CP.

According to the State Bank of Vietnam's explanation, "the goal of amending and supplementing Decree 24/2012/ND-CP is to address difficulties and shortcomings arising in practice; and to improve the efficiency of gold market management." However, this is a one-way technical approach, often leading to temporary solutions such as increasing gold supply, intervening in prices, and inspecting the market.

In reality, while technical solutions are necessary, they are insufficient and leave us constantly lagging behind the market. The correct question at the national strategic level should be: "How can we create multiple asset classes that inspire confidence so that people don't have to choose gold as their only option?"

The current widespread disparity between domestic and international gold prices, which is causing public concern, is not the cause but rather a symptom, reflecting weak confidence in other assets such as stocks, bonds, real estate, or the global banking system and macroeconomic environment .

The asset market in Vietnam is too thin and polarized, lacking intermediate asset classes such as gold certificates, digital gold, or inflation-sheltered interest-bearing savings accounts. Gold quietly reflects this lack of alternative options.

The draft amendments to Decree 24/2012/ND-CP and proposals from the Ministry of Public Security , the Ministry of Finance, and the State Bank of Vietnam all revolve around "control," "transparency," or "stabilization" of the market. However, there's a deeper issue that needs clarification: Why do people still turn to gold, even though the financial system already has stocks, bonds, and banks? The answer isn't difficult to see: Because it's the only asset people can "see," "hold," and "exit at any time."

As long as the market lacks options within the formal asset system, any reforms to gold will only address the symptoms, not the root cause. It's time for a different way of thinking. Accordingly, gold shouldn't be the issue to be managed, but rather the asset to be trusted – we need to build trust in legitimate asset classes.

With that premise, the central question we need to ask is: How can we ensure that people not only choose gold but also trust other legitimate asset classes? The following section will focus solely on the asset class within the gold ecosystem. People don't necessarily demand lower gold prices; they demand a reasonable, transparent price difference that can be explained by policy objectives.

When the difference between the price of SJC gold and the international gold price exceeds 20-30 million VND/ounce without a clear explanation, it becomes a gap between policy and trust.

The operating structure of the "exchange rate battery"

Given that monetary policy is limited to controlling inflation, there are also reasons why the State Bank cannot allocate its foreign exchange reserves to intervene whenever the gold market experiences significant fluctuations.

Firstly, for decades, our USD reserves have consistently been low (equivalent to about 3 months of imports - close to the safety threshold).

Secondly, the gold and foreign exchange markets "smell" of psychological instability, rather than being driven by actual supply and demand.

Thirdly, shortcomings in other asset markets such as stocks and bonds have led to widespread defensive sentiment: people are not withdrawing money en masse, but are quietly shifting their savings to gold and USD, thereby creating constant pressure on exchange rates and gold prices.

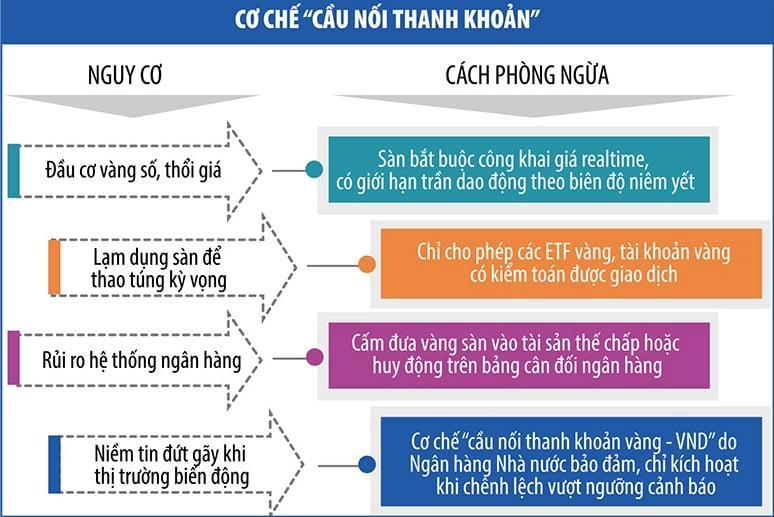

This reality leads us to the opposite thinking: instead of using USD to support gold, we should create a mechanism to turn gold into a "psychological battery" that can recharge confidence when the VND is under suspicion, without spending foreign currency. When it is not possible to "generate electricity" with USD, the Government needs to recharge confidence through gold as a buffer to absorb anxiety. This can be done through a "exchange rate battery" mechanism (see table).

|

The operating principle of the "exchange rate battery" is as follows: When the market experiences significant volatility (inflation, exchange rate tension), people tend to switch to USD or gold -> [Insecurity] -> [Switch to a legal gold exchange] -> [Standardized transactions – expectations are guided] -> [Confidence is "relieved" → Exchange rate does not need "support"] -> [Sentiment stabilizes] -> [Gold price spread narrows].

Thus, exchange rate stability is no longer a major and constant concern when managing the gold market; instead, it's a battle to regulate expectations. If the State Bank of Vietnam is unwilling/unable to sell USD, it directs anxiety towards a controlled environment. The "exchange rate battery" is the regulator of the market's "nervous system."

The mechanism for protecting the "exchange rate battery"

Whenever the market fluctuates, the State Bank of Vietnam can deploy a "liquidity bridge" mechanism. This tool allows people to convert gold to VND (and vice versa) through controlled institutions (commercial banks, gold stabilization funds, designated gold production and trading institutions) without disrupting the physical gold market or putting pressure on the exchange rate (see table).

|

Gold is not just a piece of gold, but a node in a network of digital assets.

While the world is moving towards tokenizing assets, using gold as collateral for stablecoins or legally recognized digital assets, we are still struggling with physical gold.

The proposal to establish a digital asset exchange is currently being studied by the Government. If implemented and integrated with digital gold, we would see a digitized gold system, backed by physical gold and controlled by the State. People could buy, sell, mortgage, and transfer gold in a digital environment, but without the risks of current crypto; the State would maintain control while creating an asset market with higher trust than banks, but more flexible than physical gold.

In the digital asset era, gold tokenization – transforming physical gold into a tradable digital asset – is emerging as a global trend. With Tether's XAUT, Paxos' PAXG, and the Australian Government's PMGT, the world has witnessed a wave of "precious metal digitization" aimed at creating a stable, divisible, and easily tradable asset class that retains its physical roots.

Specifically, PAXG is backed by real gold held in Brink's vault, supervised by the New York financial authority. XAUT also claims to have real gold reserves, although it has been questioned about its transparency. PMGT, issued by the Perth Mint, has publicly available physical gold certification.

It is crucial that these countries have clear laws, independent auditing systems, and the ability to resolve disputes through the courts. If we only view digital gold and gold trading platforms as a technological issue, without a clear legal framework, then digital gold could become a tool for speculation that spreads rapidly through social media, driving domestic gold prices beyond control; creating a "legal loophole" when traded across borders, avoiding financial oversight; and undermining the role of the traditional banking system if people treat gold tokens as interest-bearing deposits.

For now, during the pilot phase and while refining the legal framework, we may not need to rush into tokenizing gold, but we could start by developing domestic gold ETFs (exchange-traded funds listed on the stock exchange, designed to track the price of gold or gold-related assets); creating a pilot sandbox for "digital gold accounts" at some banks with good governance systems, risk insurance, and independent audits; and building a legal framework for digital assets backed by real assets, starting with products with low systemic risk, then progressing to testing with gold.

Conclude

The framework and proposals in this article aim to demonstrate that the price difference in gold does not lie within gold itself, but in the gap between assets, between policy and belief. Market reforms are not aimed at price management, but at reforming the structure of the gold market. Without a belief ecosystem, people will rely on the only thing they understand: gold. Solving the gold problem means creating a context where people no longer need to ask so many questions about gold.

Source: https://baodautu.vn/cach-nhin-moi-trong-tu-duy-cai-cach-thi-truong-vang-d335305.html

![[Photo] Delegation attending the 14th Congress of the Vietnam Trade Union visits the Mausoleum of President Ho Chi Minh.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/06/03/1780451842301_ndo_br_img-3824-jpg.webp)

Comment (0)