China's economy surpassing the US is no longer a certain and completely agreed-upon prediction among experts.

Since this year, China has lifted anti-epidemic lockdown measures, facilitating economic growth. However, the country has not yet escaped long-term concerns about growth prospects, according to the Economist.

China’s population is shrinking. The real estate boom is over. Tech companies are subject to tighter regulations. Foreign investors are wary, looking to relocate or diversify their supply chains. The US wants to limit China’s access to some “foundational technologies.” Globally, the win-win trend is overshadowed by geopolitics .

All of this has led many analysts to revise down their long-term growth forecasts for China, even as they raise their projections for 2023. Some wonder how much longer China’s economy can continue to outpace the U.S. The answer will affect not just factory orders or personal incomes but also the future shape of the world order.

Previously, there was a consensus among Chinese and international experts that the Chinese economy would soon surpass the US, replacing it as the world's most powerful country. To date, this prediction remains the majority. Yao Yang, an economist at Peking University, believes that China's GDP could surpass that of the US by 2029.

Others, however, believe that China’s economic dominance over its rivals has reached a limit. Hal Brands and Michael Beckley, two American political scientists, argue that China’s rise is slowing. They say that “peak China” is not as lofty as once thought.

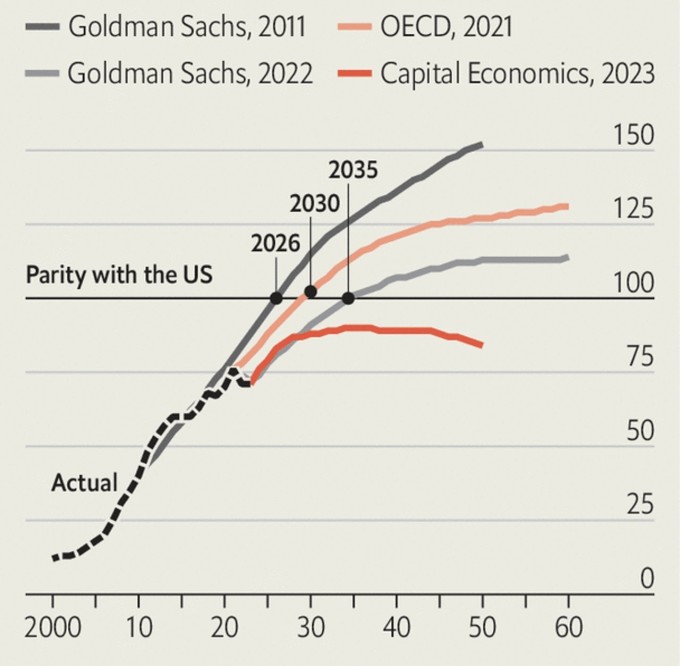

In 2011, Goldman Sachs predicted that China’s GDP would surpass that of the United States by 2026 and be 50% larger by mid-century. No peak was in sight. But late last year, the bank revised its projections, saying that China’s economy would not surpass that of the United States until 2035 and would be only 14% larger at its peak.

A similar forecast was made last year by Roland Rajah and Alyssa Leng of the Lowy Institute in Australia. Others are even more bearish about China’s peak. Research firm Capital Economics says China’s economy will never be number one. It will reach 90% of the size of the US by 2035 and then lose momentum.

Projections of China's GDP size relative to US GDP by 2060. Graphic: The Economist

Why are expectations for China's economy not as high as they once were? The answer depends on three variables: population, productivity, and prices.

As for population, China’s labor force has peaked, according to official statistics. The country has 4.5 times as many people aged 15 to 64 as the United States. The United Nations projects that the gap will be just 3.4 times by mid-century. By the end of the century, it will be 1.7 times.

China’s demographic outlook has not changed much over the past decade, even as economic growth forecasts have shrunk. In fact, new projections from Goldman Sachs suggest that China’s labor force decline will be slower than previously thought, as improvements in health can keep older workers working longer. They believe that China’s labor supply will shrink by about 7% between 2025 and 2050.

The biggest change is not about population, but about productivity. In 2011, Goldman Sachs predicted that productivity would grow by an average of 4.8% a year over the next 20 years. It now thinks it will grow by just 3%. Mark Williams, chief Asia economist at Capital Economics, has a similar view. He believes that China will “move away from being an Asian powerhouse and become a major emerging economy.”

There are reasons to worry about China’s productivity. As the population ages, more economic resources will be devoted to caring for the elderly, leaving less money to invest in new technology and capabilities. Moreover, after decades of rapid capital accumulation, the returns on new investments are diminishing. A new high-speed rail line through the mountains of Tibet, for example, is less profitable and more expensive than connecting Beijing and Shanghai.

China’s leaders are trying to tighten discipline on local governments when it comes to infrastructure spending. And they’re also tightening the reins on private companies. The return on assets for Chinese companies will gradually shrink as they grow, according to Capital Economics. That’s because they not only need to meet customer demands but also face tougher government oversight.

China’s ability to take off is constrained not only by domestic policy but also by the US government. In October 2022, the US imposed controls on the sale of advanced computer chips to China, which will hurt Chinese companies that make products such as mobile phones, medical devices and cars.

Goldman Sachs has not factored this damage into its long-term forecast, but estimates that China's GDP by the end of this decade could be about 2% smaller than it would have been without US intervention.

The tech war could go further. Diego Cerdeiro, an economist at the IMF, and a team of experts studied a hypothetical scenario in which the US restricted technology trade with China and successfully persuaded other OECD members to do the same.

Under this extreme scenario, China’s economy could be about 9% smaller in 10 years than it would have been without intervention. So it’s not hard to see why China’s productivity growth could be as low as 3% instead of 5%.

Of course, any forecast must be treated with caution. Forecasts are often wrong. Small differences in productivity or population growth, when combined and accumulated over many years, can lead to dramatically different outcomes.

Forecasts are also sensitive to prices, especially the relative prices of currencies. Unexpected changes in exchange rates can distort predictions of economic strength. Currently, a basket of goods and services that costs $100 in the United States costs about $60 in China. That suggests the yuan is undervalued.

Capital Economics believes this low valuation will persist, while Goldman Sachs believes valuations will narrow, possibly due to a stronger yuan or faster appreciation in China compared to the US. In Goldman Sachs’ view, this process will add about 20% to China’s GDP by mid-century.

If China's prices or exchange rate do not rise as Goldman Sachs predicts, China's GDP may never surpass that of the United States. If China's labor productivity grows just half a percentage point slower than Goldman Sachs predicts, China's GDP, all else equal, will never surpass that of the United States.

The same would happen if the US grew half a percentage point faster. If China’s fertility rate continues to decline (it will reach 0.85 children per woman by mid-century), China could take the lead in the 2030s and lose that position in the 2050s.

Even if China’s economy becomes the world’s largest, the gap with the second-largest economy is likely to be small. China is unlikely to build a lead over the US that is comparable to the 40% lead the US has over China, according to Rajah and Leng.

So a safe bet is that China and the US will remain near parities for decades to come. In Goldman Sachs’s scenario, China maintains a small but steady advantage over the US for more than 40 years. Capital Economics predicts that China’s GDP will still exceed 80% of US GDP by the end of 2050. China will continue to be a formidable rival to the world’s current leading superpower.

Phien An ( according to The Economist )

Source link

![[Maritime News] Container shipping faces overcapacity that will last until 2028](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/7/30/6d35cbc6b0f643fd97f8aa2e9bc87aea)

Comment (0)