Risk reserves were once considered a "safety cushion" and an important savings for banks. However, when many deferred and deferred debts in the previous period have been handled, many banks have chosen to reduce their provisions to create room to promote growth in the new period.

Many banks' risk buffers continue to shrink

The financial reports for the second quarter of 2025 show that banks' profits have grown strongly, with about 85% of listed banks reporting positive profits and more than half recording double-digit growth. Some banks such asSHB , PGBank, Sacombank, VietinBank, SeABank... recorded profit increases of 30% to 80%, reflecting a positive recovery after a period of stagnation.

However, behind the impressive profit figures is the fact that many banks have had to loosen their financial safety buffers, through reducing risk provisions. This is a key factor in maintaining profit growth in the context of high capital costs and credit pressure that has not decreased.

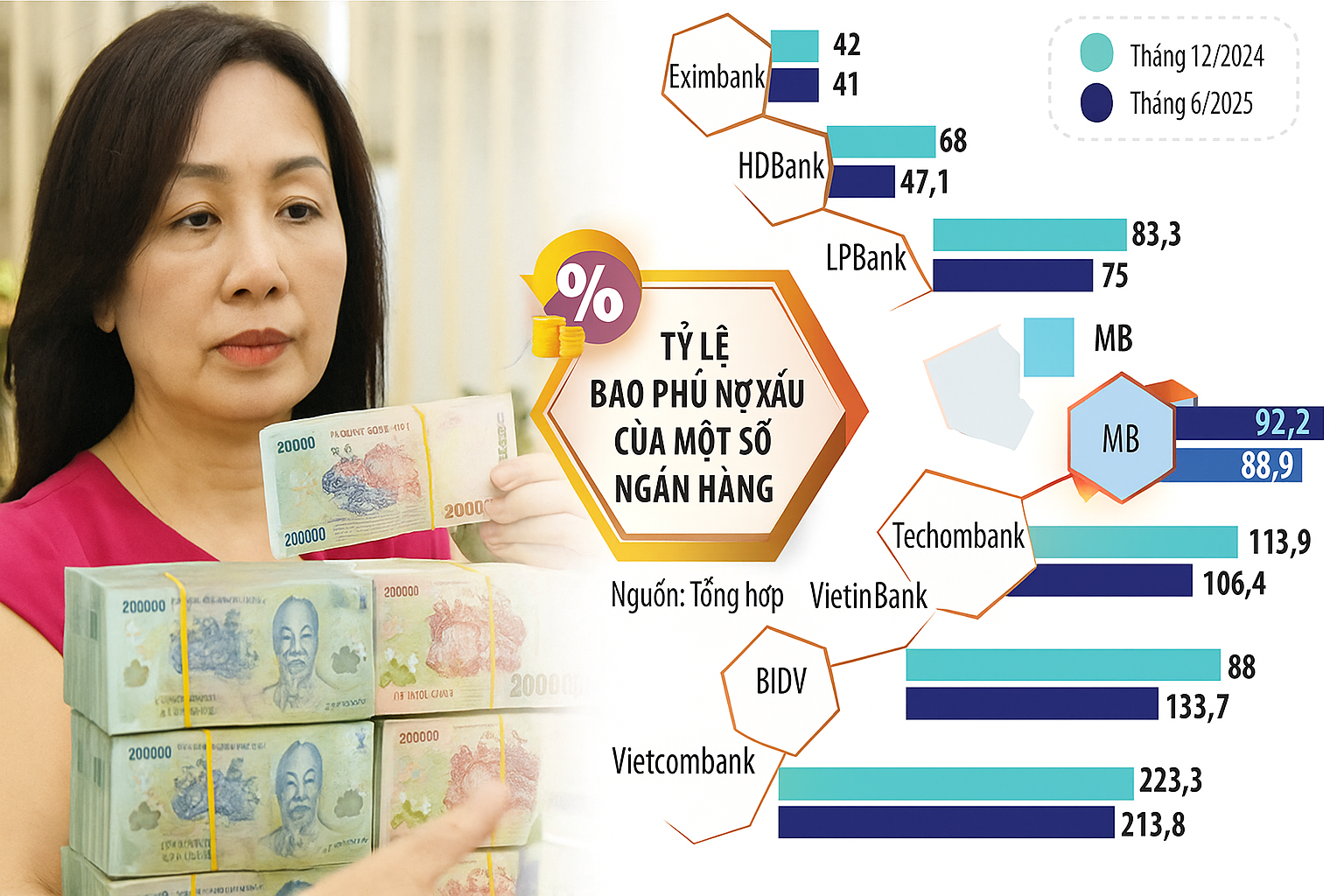

Among the group of state-owned commercial banks, only Agribank increased its bad debt coverage ratio in the first half of the year. As of the end of June 2025, Agribank's bad debt coverage ratio reached 148.6%, an increase of 16.8 percentage points compared to the beginning of the year.

On the contrary, BIDV has a significant decrease when the bad debt coverage ratio is only 88%, significantly lower than 133.7% at the end of 2024 and 96.8% in the first quarter of 2025. BIDV's total bad debt in the first 6 months of the year increased by 49%, reaching VND 43,140 billion, while the provision only increased slightly by 9.5%, causing the risk buffer to be significantly eroded.

Vietcombank is still the bank with the highest bad debt coverage ratio in the system, reaching 213.8%. However, this figure has decreased slightly compared to 223.3% at the end of last year. At VietinBank, the coverage ratio also decreased to 134.8%, instead of 170.7% as at the end of 2024.

The private joint stock commercial bank group also recorded a similar trend. At MB, the bad debt coverage ratio as of the end of June 2025 was only 88.9%, a slight decrease compared to 92.3% at the end of last year.

HDBank saw a deeper decline, with its bad debt coverage ratio falling to just 47.1%, much lower than the previous nearly 68%. SHB fell from nearly 64% to 58%. LPBank was no exception, with its risk buffer falling from 83.3% at the end of last year to 75% at the end of the second quarter.

Some other banks recorded worryingly low bad debt coverage ratios such as VIB at 37.16%, NamABank at about 39%, Eximbank at 41% and MSB at 55.5%.

In the whole system, the bad debt coverage ratio has tended to decrease sharply in the past three years. If in the third quarter of 2022, this ratio was still at 143.2%, by the third quarter of 2023 it had dropped below the threshold of 100%. By the end of the first quarter of 2025, the whole system will only maintain about 80%.

Reducing provisions in the context of increasing bad debt and an economy with many potential variables not only weakens the resistance of the banking system, but also raises questions about the sustainability of profits in the medium and long term.

The buffer cannot be loose.

It is understandable that many commercial banks are reducing their provisioning to prioritize growth in the current context, especially when the pressure on shareholders' profits is increasing. In addition, the economic situation is also different from the pandemic period, making the reduction in provisioning a trend.

In the period 2020-2022, when Covid-19 caused bad debt to swell, many banks were forced to restructure, extend, and postpone debts for customers. Since then, risk provisions have been boosted to create a safe "cushion". Now, when the debts that were extended have been processed, especially at the Big 4 group, the need to maintain a high bad debt coverage ratio is no longer as urgent as before.

However, when Resolution 42 on bad debt settlement expired, many banks were concerned about the possibility of recovering collateral if customers deliberately delayed and did not cooperate, so they still maintained strong provisions. Recently, with the passage of the Law on Credit Institutions (amended), the right to seize assets has been legalized, helping to reduce that concern.

Although the bad debt coverage ratio tends to decrease, this is not necessarily a big risk, because risk provisions are not only a preventive tool, but also a strategic "reserve", playing an important role in bank profits.

In the first half of this year, many banks unexpectedly recorded large profits from debt recovery that had been handled with provisions. For example, Agribank's net profit from other activities reached nearly VND6,000 billion, second only to the credit segment, up more than 91%.

At Techcombank, while the main business segments declined, profits from other activities increased more than three times, with more than 66% coming from risk-treated debt. ACB, LPBank... also recorded a 2-3 times increase from this source of revenue.

In the context of the Vietnamese banking system still having thin capital, the capital safety ratio is still low compared to the rapidly growing credit sector and the State Bank has just loosened the "room" for many banks, maintaining and improving reserve capacity becomes even more necessary.

This is not only a defensive barrier, but also a factor that strengthens market confidence and ensures sustainable growth for the entire system.

Source: https://baolamdong.vn/khi-ngan-hang-khong-con-giu-chat-cua-de-danh-386441.html

Comment (0)