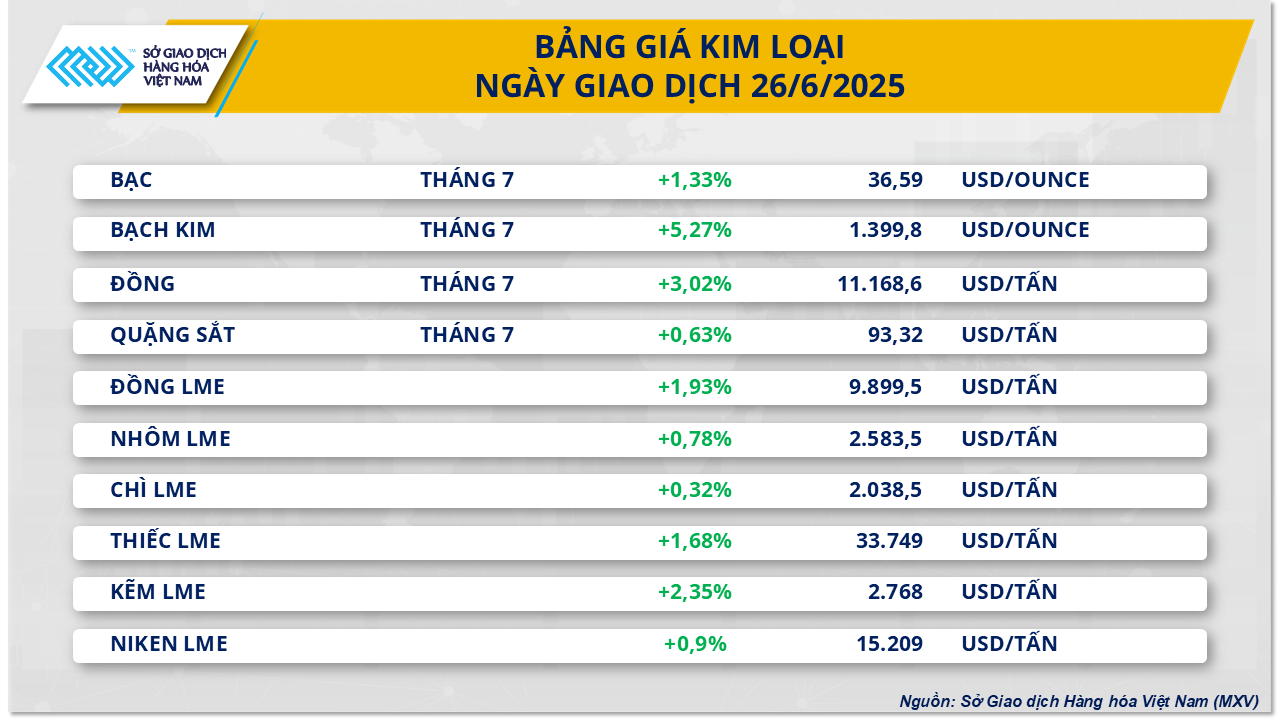

In the metal market, at the end of yesterday's trading session, the metal market was up across the board. Silver prices continued to increase by 1.33% to $36.59/ounce, while iron ore prices also recovered by 0.63% to $93.32/ton.

The US dollar index continued to fall to 97.15 points in yesterday's trading session, marking the fifth consecutive session of decline. The depreciation of the greenback has made USD-denominated metals more attractive to international investors, thereby triggering strong buying pressure in the precious metals market.

Concerns about Trump’s tariffs are back in investors’ minds as the 90-day moratorium on reciprocal tariffs expires on July 9. In a report released on June 25, JPMorgan Chase warned that tariffs would slow US economic growth and accelerate inflation, leading to a 40% risk of recession. The dollar has also weakened on growing expectations that the Federal Reserve will cut interest rates further this year.

Silver prices are also supported by a persistent deficit. The silver market is estimated to be short by 117.6 million ounces this year. The shortage in the silver market is becoming more difficult to improve after Mexico, the world's largest silver producer, announced that it would not issue new mining licenses. At the same time, the government will review all existing environmental impact assessment licenses, which could lead to restrictions on mining activities at many existing mines. According to the World Silver Institute, Mexico will produce 185.7 million ounces of silver in 2024, equivalent to 23% of global mining output.

While supply continues to tighten, demand for silver from the electrical and electronics sector continues to grow, perpetuating the supply-demand imbalance in the market. Demand from this sector is expected to increase by 1% this year, following a 4% increase last year, to 465.6 million ounces, driven by expansion in auto production, investment in the power grid, and consumer electronics.

In the base metals market, iron ore prices were supported by concerns about disruptions to the steel supply chain in southern China. Guangdong and Guangxi provinces, which account for about 9% of the country’s crude steel output, are currently affected by prolonged rainstorms, which threaten to disrupt production at steel mills. However, the rally in iron ore prices is unlikely to sustain as the overall market picture remains bearish.

In fact, iron ore demand remains under pressure from multiple fronts, including Beijing’s continued plan to restructure its steel industry through production cuts, which was reaffirmed by a Chinese government report in early May. There is widespread speculation that Beijing could cut as much as 50 million tonnes of crude steel this year, equivalent to nearly 5% of the country’s annual output. Against this backdrop, consumption of raw materials such as iron ore is unlikely to recover strongly.

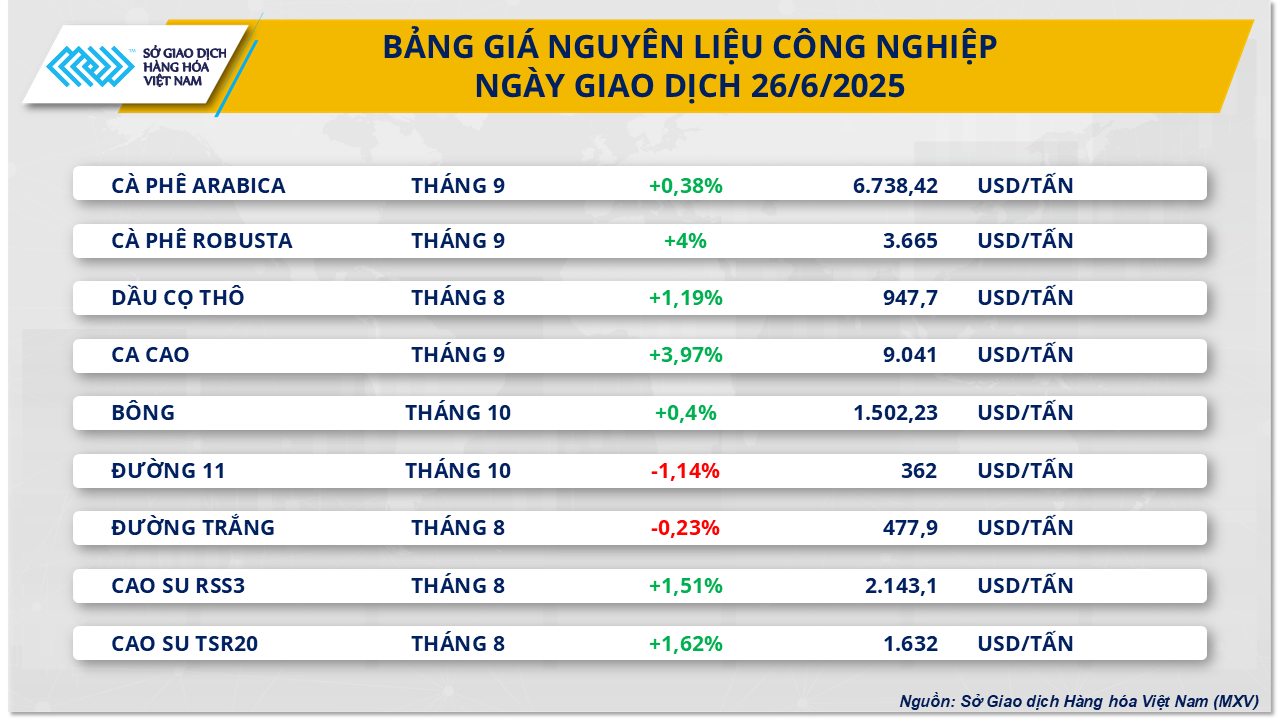

Regarding the industrial raw material group, according to MXV, the industrial raw material market also recorded positive buying power in yesterday's session. Notably, two sugar products in the same group weakened under pressure from the surplus of supply and demand. Specifically, the price of sugar 11 has decreased in 9 out of the last 11 sessions, currently trading at 362 USD/ton, equivalent to a decrease of about 1.1%. In addition, the white sugar contract also decreased slightly by 0.23%, down to 478 USD/ton.

The global sugar surplus has continued to weigh on sugar prices over the past three months. According to the latest forecast from the US Department of Agriculture (USDA), global sugar production in the 2025-26 crop year is expected to increase by 4.7% from the previous season to 189.3 million tonnes. The global surplus is estimated at around 41.2 million tonnes, up 7.5% from the previous year.

In Brazil, the sugarcane harvest is underway at a rapid pace. Mills in the central-south region crushed 47.84 million tonnes of sugarcane in the second half of May, up 5.5% from the same period in the 2024-2025 crop year. The market is also witnessing fierce competition between sugar and hydrous ethanol production, as the price gap between the two products is narrowing. Some mills in the central-south region have prioritized switching to ethanol production. Ethanol's appeal is expected to increase sharply after Brazil announced the implementation of the E30 program, increasing the ethanol blending ratio in gasoline to 30%, thereby boosting domestic ethanol consumption.

In the United States, concerns about sugar demand were reflected in the USDA’s June Sweeteners Market Report (SMD), which showed that sugar deliveries for consumption in April fell 6% year-over-year, following a slight increase of 1.8% in March. Total sugar deliveries from October to April were down 3.1% year-over-year. The SMD figures also suggest that USDA is likely to further lower its forecast for full-year WASDE shipments, after cutting 115,000 short tons in the past two months.

Source: https://baodaknong.vn/thi-truong-hang-hoa-27-6-sac-xanh-quay-lai-chiem-ap-dao-tren-thi-truong-256990.html

Comment (0)