This is the information recorded at the online event "Real estate market overview in the third quarter of 2025" with the theme "The rhythm" organized by Batdongsan.com.vn on the morning of October 7. The event attracted the attention of many experts, investors and businesses operating in the real estate sector.

The recovery platform from the macro economy

According to Mr. Nguyen Quoc Anh - Deputy General Director of Batdongsan.com.vn, Vietnam's economy in the third quarter continued to maintain a positive growth momentum, creating favorable conditions for the real estate market. GDP in the third quarter increased by 8.23% - the highest level in the same period since 2011 (except for the recovery in 2022 after the COVID-19 pandemic). In the first 9 months, GDP increased by 7.85% over the same period, approaching the target of 8% or more for the whole year.

Public spending reached VND440 trillion, up 37% over the same period and becoming the main driving force for economic growth. A series of key infrastructure projects are entering the intense construction phase such as Gia Binh International Airport, Ngoc Hoi Bridge connecting Hanoi - Hung Yen, North - South Expressway, Long Thanh Airport... contributing to expanding development space for suburban markets - Mr. Quoc Anh cited.

In addition, foreign direct investment (FDI) continues to flow strongly into real estate – one of the three leading sectors attracting FDI. Economic indicators such as PMI recover, domestic production and consumption grow steadily. However, the rising inflation trend and expansionary monetary policy with reduced interest rates also pose some challenges to the market.

Experts say that the real estate market in the third quarter of 2025 will see a clear differentiation between the buying and selling channels. After the second quarter with many macro fluctuations, the level of interest in real estate for sale quickly recovered, in which apartments played a leading role, while townhouses and private houses also began to show signs of improvement. Many areas recorded an increase in interest of 11-22% compared to the beginning of the year.

In contrast, the rental segment declined after the Ghost Month (the 7th lunar month), especially the rental room and boarding house segment. The interest level in September 2025 recorded a decrease of 8-24% depending on the type compared to the previous month.

Real estate shows good resilience in terms of absorption of new supply and market sentiment. However, the brokerage survey in the third quarter of 2025 by Batdongsan.com.vn shows that absorption of new supply is still positive, with nearly 90% of respondents rating it as average to good, of which 4% said it was “very good” and 25% said it was “good”. Only 12% said absorption was not optimistic.

Regarding the market outlook for the fourth quarter, 60% of brokers believe the market will continue to grow, of which 17% expect strong growth. About a third believe the market will remain stable, and only 6% expressed concern about the possibility of a decline.

Notably, the apartment segment is still rated highest in terms of growth potential in the next 6 months with 36% of choices, followed by private houses (29%) and land plots (24%). Other types such as townhouses, resort real estate or villas only account for a small proportion, reflecting the concentration of cash flow on products that meet real housing needs and high liquidity.

Repositioning investment channels

Experts from Batdongsan.com.vn believe that 2025 will mark a major shift in the correlation of investment rates between asset channels. It is worth noting that in the period 2015-2025, investment channels in Vietnam have been strongly differentiated and 2025 will become a milestone of "major change" in the correlation of rates between asset channels.

Gold took the lead with a 3.57-fold increase compared to 2015, followed by land with a 3.12-fold increase, reflecting a strong cash flow into real assets associated with infrastructure expectations and long-term accumulation. Although apartments did not make the strongest breakthrough, they also accelerated, gradually catching up with land thanks to both meeting real housing needs and having investment potential. Securities followed closely with a 2.78-fold increase, affirming their role as an attractive investment channel in the context of economic recovery and global fluctuations. In contrast, savings deposits and USD became less competitive, increasing only 67% and 24%, respectively.

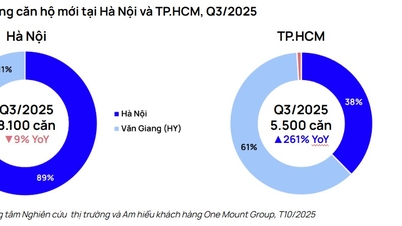

One of the prominent trends of the third quarter is the shift of cash flow from central cities to suburban areas - where there is still much development potential and is strongly supported by inter-regional connectivity infrastructure.

Ms. Nguyen Thi Ngoc Thuong - Director of Batdongsan.com.vn's Hai Phong branch shared that instead of focusing on central cities, cash flow and real estate demand are shifting strongly to the suburbs - where there is still much room for growth and inter-regional infrastructure is increasingly complete.

Interest in both central cities in the third quarter showed signs of slowing down. In Hanoi, interest decreased by 22% compared to the same period in 2024, while in Ho Chi Minh City it was almost flat or decreased slightly by 1% in the new area. In contrast, neighboring provinces emerged as "bright spots". The suburbs of Hanoi grew by 11%. Outside of Hanoi, interest was concentrated in the areas of Hai Phong, Hoa Binh (old), and Bac Giang (old).

The real estate picture in the North in the third quarter shows a clear trend of shifting out of Hanoi. The areas of Hai Phong, Hung Yen, Hoa Binh (old) and Bac Giang (old) became the "center of attention" when accounting for 80% of the total interest in the whole region. In which, Hai Phong holds the number one position with an index of 100, Hung Yen is second (62) and Bac Ninh (35) is third - Ms. Thuong informed.

In terms of growth rate compared to the beginning of the year, Hoa Binh (old) leads with 65%, followed by Bac Giang (old) 61%, Hai Phong 50% and Bac Ninh 48%). Other localities such as Quang Ninh, Hung Yen, Vinh Phuc (old) also maintained growth momentum of 26-42%. This boom reflects the trend of capital shifting to satellite cities around Hanoi - where prices are competitive, infrastructure connections are convenient and there is long-term potential for expansion.

Source: https://baotintuc.vn/kinh-te/suc-bat-thi-truong-bat-dong-san-tu-nhip-dankinh-te-va-dong-tien-dich-chuyen-20251007141259025.htm

![[Photo] Super harvest moon shines brightly on Mid-Autumn Festival night around the world](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/10/07/1759816565798_1759814567021-jpg.webp)

Comment (0)