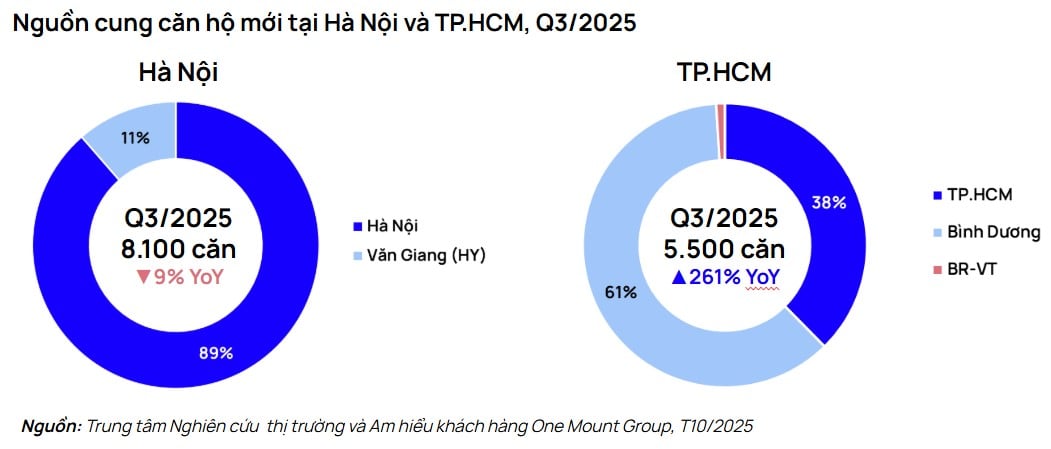

The third quarter 2025 report of One Mount Group's Center for Market Research and Customer Insights noted that the Hanoi real estate market continues to be vibrant, with the supply of newly opened apartments reaching 8,100 units, a slight decrease of 9% compared to the same period last year, but still higher than the average for the period 2023 - 2025.

Hanoi's new supply is mainly concentrated in the East and West, notably Van Giang ( Hung Yen ), accounting for 11% of the total sales volume, along with large-scale projects such as Lumiere Prime Hills, Sun Feliza Suites, Kepler Land Mo Lao or Masteri Trinity Square... The West still plays a leading role thanks to its complete infrastructure and abundant land fund, accounting for about 36% of new supply.

Meanwhile, Ho Chi Minh City after the merger witnessed a strong breakthrough, with 5,500 units, an increase of 261% compared to the same period in 2024, marking the highest recovery in the past 3 years. The driving force comes from the new legal regulations starting to take effect, helping the supply gradually improve, although the distribution is still uneven. More than 60% of the sales volume comes from Binh Duong area, while the center of Ho Chi Minh City is still scarce in new projects due to prolonged legal progress.

The average apartment price in the two major cities continued to increase sharply, both over 20% compared to the same period last year. Specifically, in Hanoi, the average price reached 85.6 million VND/m², up 23%, while in Ho Chi Minh City it was 95.4 million VND/m², up 21% over the same period. Newly opened projects in the third quarter of 2025 approached 108 - 131 million VND/m², clearly reflecting the trend in the high-end product group.

The price structure shows that more than 50% of new supply in both markets is over 100 million VND/m². Especially in the West of Hanoi, the first projects launched for sale have prices from 104 million VND/m². In Ho Chi Minh City after the merger, the price range is wider, from 30 - 200 million VND/m², but mid-range apartments are mainly located in Binh Duong; the central area still records the highest price level in the market.

In addition, despite high selling prices, the absorption rate of projects launched in the third quarter of 2025 is still impressive. Many projects in Hanoi and Ho Chi Minh City recorded "sold out" status on the opening day, showing that real demand and investment cash flow remain stable, especially for projects with favorable locations and transparent legal status.

One Mount Group forecasts that in 2025, the primary supply in Hanoi will reach about 31,000 units, the highest in 3 years, while Ho Chi Minh City is expected to reach 28,000 units. In 2026, the supply will remain at 32,000 units in Hanoi and 23,000 units in Ho Chi Minh City. Notably, Binh Duong accounts for about 65% of the supply in the southern region in 2025 and will maintain a rate of about 50% next year, affirming the trend of expanding to the outskirts of the Ho Chi Minh City market after the merger.

Mr. Tran Minh Tien shared: “In the first 9 months of 2025, both markets witnessed a significant increase in selling prices, with some central projects exceeding the 100 million VND/m² mark. However, the average absorption rate remained above 80%, with many projects sold out in just a few days. This reflects the sustainable appeal of real estate in large cities, where real demand for housing and investment remains high. It is forecasted that in 2026, the market will continue to recover strongly, with more abundant supply helping to stabilize selling prices in the medium term.”

Source: https://baotintuc.vn/kinh-te/thi-truong-bat-dong-san-soi-dong-gia-ban-neo-cao-nhung-luc-cau-van-manh-20251006170207801.htm

Comment (0)