With the prospect of Vietnam's stock market being upgraded to frontier emerging market status by FTSE Russell on October 8, positive Q3 business results and loose global monetary policy, opportunities are opening up for capital flows to return, laying the foundation for a more sustainable recovery.

Accumulate waiting for capital flow

According to the October 2025 report of Dragon Capital Securities Company (VDSC), the liquidity of the entire market in September decreased by more than 30%, reflecting the waiting mentality of investors after the hot growth period since the beginning of the year. However, this development is assessed by VDSC as positive and healthy, as the market is in the process of rebalancing valuations and waiting for positive signals after FTSE Russell upgraded the Vietnamese stock market.

Experts believe that the Vietnamese market is in its best position in many years. Mr. Huynh Anh Huy, Director of KAFI Securities Industry Analysis, commented: “Vietnam’s macro economy has shown outstanding resilience, with GDP remaining among the leading groups in the region, inflation being controlled and domestic consumption recovering clearly. This is an important foundation to help foreign capital flow return soon.”

Sharing the same perspective, Mr. Tran Thai Binh , Senior Director of OCBS Securities Analysis, said that Vietnam's GDP in 2025 could reach 7-8% thanks to strong growth in electronics, textile and international tourism exports, while public investment and infrastructure continue to be the main support.

Meanwhile, VDSC assessed that VN-Index is accumulating in the range of 1,489 - 1,758 points, corresponding to a target P/E of 13.3 - 14.7 times, an attractive level compared to the 10-year average. At the same time, the yield difference between stocks and 10-year government bonds is only 2.9%, lower than the 5-year average, showing that stock valuations are entering an attractive zone for medium-term cash flow.

Dr. Jochen Schmitmann, Chief Representative of the International Monetary Fund (IMF) in Vietnam, Cambodia and Laos, also expressed his impression of Vietnam's reform pace over the past year. Economic growth in the first 9 months of 2025 reached 7.8%, also the highest level since 2011. This momentum comes from many diverse factors such as: Strong growth of the manufacturing - export sector despite tariffs, FDI capital flows maintained at a high level, recovery of domestic demand, tourism and the boost from public spending on administrative reform.

In addition, monetary and fiscal policies have also supported growth. Specifically, the State Bank of Vietnam (SBV) has maintained relatively appropriate interest rates, with credit growth expected to reach 18-20% this year. In addition, the Government's institutional reforms such as merging ministries, reducing local government levels, reducing the number of provinces and the target of streamlining 100,000 public employees are highly appreciated.

The global context is also creating favorable conditions. Specifically, the Fed is likely to continue to cut interest rates by another 25 basis points in October, and even more aggressively by the end of the year. As the USD weakens and US bond yields cool, international investment funds tend to shift capital to more stable emerging markets, in which Vietnam stands out thanks to its positive trade balance and clear upgrading process.

According to Mr. Huy, the market is in a state of compression, a necessary accumulation before an explosion, and emphasized the highest probability (50%) that the VN-Index will exceed 1,700 points after the market is announced to be upgraded by FTSE Russel.

Opportunity differentiation - portfolio selection time

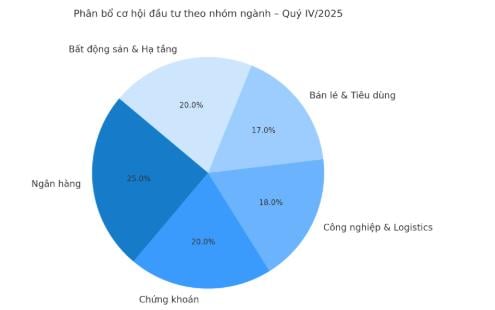

With the above factors, smart money has begun to pivot, prioritizing industry groups with clear prospects and solid fundamentals. According to VDSC's report, 18/22 industry groups had double-digit growth in Q3 profits, led by residential real estate (+424%), fertilizer and seaports (+90-300%), along with steel and retail, industries that are demonstrating strong resilience after a period of stagnation.

“The market is strongly differentiated and this is a period of selection instead of spreading. Accordingly, investors should focus on leading enterprises with financial advantages and real profit growth,” Mr. Tran Thai Binh (OCBS) noted.

In the short term, banks continue to play a pivotal role as they benefit from low interest rates and steady growth in credit demand, while the securities group benefits directly if the market is upgraded and margins are expanded.

In addition, the industrial, logistics and export manufacturing groups, especially enterprises with orders from the US and Europe, are forecast to maintain growth momentum as international trade cools down and transportation costs decrease. The retail and consumer goods sectors are also bright spots, thanks to improved domestic purchasing power and lower input material prices, helping to expand profit margins in the last quarter of the year.

Mr. Huynh Anh Huy (KAFI) recommends that the current investment strategy is flexible but disciplined: “Investors should disburse at reasonable prices, keeping a cash ratio of 20-30% to proactively restructure. Margin can be used at a controlled level, prioritizing leading stocks with stable cash flow. This is the time to accumulate, not to withdraw.”

HSBC estimates that after the market is upgraded, Vietnam could account for about 0.6% of the FTSE Asia index and 0.5% of the FTSE Emerging Markets index, potentially attracting about $1.5 billion from passive funds. In a more optimistic scenario, capital flows from passive funds could reach $3 billion, along with $1.9 - $7.4 billion from active funds.

BSC Research forecasts that Vietnam could attract between $0.76 billion and $1.34 billion in net capital from global ETFs and open-end funds, especially funds that reference the FTSE Emerging Markets All Cap Index. The new cash flow will focus on stocks that meet the criteria of capitalization, liquidity, and importantly, have foreign "room".

However, investors should note that foreign capital will not flow in immediately as the transition process takes time. According to FTSE Russell, the announcement to upgrade Vietnam from a frontier market to a secondary emerging market, with an official effective date of 21 September 2026, is subject to an intermediate review in March 2026 to determine whether there has been sufficient progress in facilitating access for global brokers. Therefore, the upgrade will be implemented in several phases, with details of the implementation plan to be announced in the March 2026 announcement.

According to the base case scenario of VDSC and OCBS, VN-Index can maintain the fluctuation range of 1,600 - 1,750 points in October, with a 50% probability of surpassing 1,700 after Vietnam is upgraded. Experts agree that the long-term outlook for Vietnam's stock market remains solid thanks to a stable macro environment, improved corporate profits and the early return of foreign capital in the new cycle.

Source: https://baotintuc.vn/thi-truong-tien-te/thi-truong-chung-khoan-co-bung-no-sau-thong-tin-duoc-nang-hang-20251007170941902.htm

![[Photo] President Luong Cuong attends the 50th Anniversary of Laos National Day](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F11%2F27%2F1764225638930_ndo_br_1-jpg.webp&w=3840&q=75)

![[Photo] Prime Minister Pham Minh Chinh chairs the 15th meeting of the Central Emulation and Reward Council](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F11%2F27%2F1764245150205_dsc-1922-jpg.webp&w=3840&q=75)

![[Infographic] Vietnam's stock market exceeds 11 million trading accounts](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/11/09/1762677474332_chungkhoanhomnay0-17599399693831269195438.jpeg)

Comment (0)