ANTD.VN - The risk coefficient that banks apply to loans for social housing purchases and housing purchases under government support programs and projects may be reduced by half compared to the current level.

The State Bank is seeking comments on the draft Circular amending and supplementing a number of articles of Circular No. 41/2016/TT-NHNN dated December 30, 2016 of the Governor of the State Bank of Vietnam regulating the capital safety ratio for banks and foreign bank branches.

One of the notable amendments is that the State Bank wants to allow credit institutions to reduce the risk coefficient applied to loans for purchasing social housing and housing under Government support programs and projects. The reduction is 50% compared to current regulations.

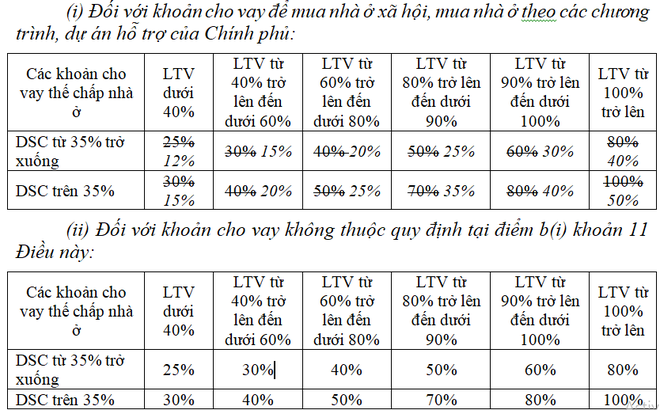

Specifically, for the above loans, mortgaged with housing with an income ratio (Total balance to be repaid in the year/Total annual income of the customer - abbreviated: DSC) of 35% or less, the risk coefficient will be reduced from 25% - 80% (depending on the guarantee ratio - LTV) to 12% - 40%.

Similarly, for loans with a DSC ratio above 35%, the risk coefficient will range from 15% - 50% (compared to the current level of 30% - 100%).

Details as follows:

|

The risk coefficient applied to loans for social housing purchases is reduced by half compared to current regulations. |

The State Bank believes that reducing the risk coefficient for the above loans is to encourage lending to social housing projects and housing projects under the Government's support programs and projects, and is in accordance with the provisions of Circular 22/2019/TT-NHNN and the Government's direction in Resolution No. 33/NQ-CP dated March 11, 2023 on a number of solutions to remove obstacles and promote the safe, healthy and sustainable development of the real estate market.

According to the provisions of Circular 22/2019/TT-NHNN, the risk coefficient of 50% is applied to receivables fully secured by housing (including future housing), land use rights, construction works attached to the borrower's land use rights and when meeting one of the following conditions:

Is a loan to serve business activities according to the regulations of the State Bank regulating lending activities of credit institutions and foreign bank branches;

Is a personal loan for customers to buy social housing, buy housing under Government support programs and projects;

This is a personal loan for customers to buy a house with the agreed loan amount/loan level in the credit contract under 1.5 billion VND. Each customer is only allowed to apply this risk coefficient for 1 loan).

In addition, the draft circular maintains the risk coefficient for other real estate loans.

In particular, banks must apply the highest credit risk coefficient of up to 200% for assets that are credit loans to finance real estate business projects. In the case of assets that are credit loans to finance industrial park real estate business projects, the credit risk coefficient is 160%.

The risk coefficient of 150% is applied to receivables secured by real estate for which banks and foreign bank branches do not have information on the security ratio...

Previously, many experts recommended that the State Bank should consider reducing the risk ratio for some real estate segments to reduce pressure on banks.

Experts say that the risk coefficient greatly affects the capital safety ratio of banks. Accordingly, loans with high risk coefficients require banks to have a high amount of "corresponding" equity capital to ensure the capital safety ratio.

Dr. Can Van Luc - Member of the National Financial and Monetary Policy Advisory Council said that the Ministry of Construction should classify real estate into groups with different levels of risk. Based on the classification of the Ministry of Construction, the State Bank will adjust the risk coefficient accordingly.

Source

![[Photo] Prime Minister Pham Minh Chinh chairs the national online conference on combating smuggling, production and trade of counterfeit goods.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/6/23/4a682a11bb5c47d5ba84d8c5037df029)

![[Photo] Prime Minister Pham Minh Chinh holds meeting to launch exhibition of national achievements to celebrate 80th National Day](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/6/23/0c0c37481bc64a9ab31b887dcff81e40)

![[Photo] Party Congress of the Central Internal Affairs Commission for the 2025-2030 term](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/6/23/5bf03821e6dd461d9ba2fd0c9a08037b)

Comment (0)