|

Banks dominate the bond market

According to the Vietnam Bond Market Association, as of June 13, 2025, there were 13 corporate bond issuances recorded in June 2025 with a total value of VND 15,109 billion. Of which, bonds issued by joint stock commercial banks alone were VND 13,889 billion, accounting for nearly 92% of the total issuance value of the entire bond market.

The total value of corporate bonds issued since the beginning of the year has been recorded at VND157,536 billion, up 71% over the same period last year. Of which, bank bonds dominate. From the beginning of the year to mid-June 2025, the total value of bank bonds issued was about VND114,000 billion, 2.2 times higher than the same period last year.

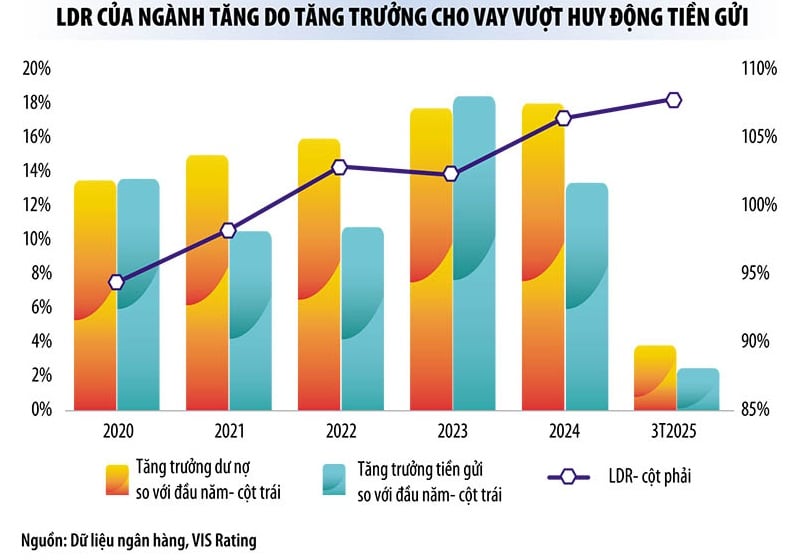

Mr. Nguyen Dinh Duy, Director and senior analyst at VIS Rating, said that credit growth higher than mobilization is the reason why banks have sharply increased bond issuance since the beginning of the year.

The latest statistics from the State Bank show that by the end of May 2025, credit in the entire economy increased by 6.52%. The State Bank has not updated the deposit growth rate up to this point, but according to experts' estimates, credit is growing at a rate 2-3 times higher than the capital mobilization growth rate.

According to the latest data just announced by the State Bank, by the end of March 2025, deposits of individual customers and economic organizations increased by 1.8% compared to the previous month, while outstanding credit increased by nearly 3.93%. Thus, by the end of March 2025, capital mobilization of credit institutions "lacked" about 1.3 million billion VND compared to credit growth. The gap between credit and capital mobilization will certainly increase sharply up to this point.

Currently, commercial banks have not yet announced their financial reports for the second quarter of 2025, but their financial reports for the first quarter of 2025 show signs of decline in capital and liquidity. Specifically, in the first quarter of this year, the ratio of demand deposits (CASA) to total outstanding loans in the entire industry decreased by 2 percentage points compared to the previous quarter, due to businesses withdrawing deposits from some banks.

In particular, the industry's loan-to-deposit ratio (LDR) is rising to a five-year high, reaching 108% at the end of the first quarter of 2025. Liquidity pressure is more evident at some small and medium-sized banks.

Although the banking system's liquidity is still abundant, liquidity pressure will gradually increase because the peak disbursement period usually falls at the end of the year.

“In the context of low interest rates, banks are increasing bond issuance to support strong credit growth as well as improve financial safety indicators, such as capital adequacy ratio and limit the use of short-term capital for medium- and long-term loans,” said Mr. Nguyen Quang Thuan, General Director of FiinRatings.

The bank will mobilize about 200,000 billion VND.

According to analysts, not only in the first half of the year, but from now until the end of the year, banks will still be the dominant issuers in the bond market.

“With loan growth much higher than deposit growth, we believe that banks will increase long-term bond issuance to meet capital needs. Accordingly, banks will continue to lead new issuance in the second half of 2025, with a total issuance plan of nearly VND200,000 billion in 2025,” said Mr. Nguyen Dinh Duy.

Recently, the Military Commercial Joint Stock Bank announced a plan to issue 30,000 billion VND in bonds. Asia Commercial Joint Stock Bank (ACB ) announced that it will issue 20,000 billion VND in bonds. Many other commercial joint stock banks also plan to mobilize thousands of billions of VND through the bond channel.

In addition, according to experts, from July 1, 2025, the Law amending and supplementing a number of articles of the Enterprise Law, which has just been passed by the National Assembly , will take effect. Accordingly, non-public companies wishing to issue individual bonds must have liabilities not exceeding 5 times their equity. This will tighten the issuance of individual corporate bonds. Banks will have an even greater advantage in this playing field.

According to economist Hoang Van Cuong, tightening the conditions for issuing individual bonds is necessary to eliminate risky businesses, protect investors’ interests and help the bond market become healthy. However, this also makes it more difficult for non-bank corporate bonds to be issued.

Ms. Trinh Quynh Giao, General Director of PVI Asset Management, said that the structure of the bond market is unreasonable. “Previously, in the structure of corporate bond issuance in the market, real estate usually accounted for 1/3, banks accounted for 1/3, and the rest were other components. But currently, 77% of bonds issued in the market belong to the banking group,” Ms. Giao said.

To prevent banks from being "alone" in the bond market, experts say it is necessary to boldly have mechanisms to attract investment capital from funds (especially insurance funds) and from banks investing in bonds.

In addition, on July 1, 2024, the State Bank of Vietnam stipulated that commercial banks are not allowed to participate in managing collateral for bond issuance packages, making it difficult for banks to invest in bonds, reducing market liquidity. This is also the reason why banks almost take on the role of both buyers and sellers in the current bond market.

Source: https://baodautu.vn/tin-dung-tang-nhanh-ngan-hang-ram-ro-phat-hanh-trai-phieu-d309867.html

![[Photo] Prime Minister Pham Minh Chinh launched a peak emulation campaign to achieve achievements in celebration of the 14th National Party Congress](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/10/5/8869ec5cdbc740f58fbf2ae73f065076)

![[Photo] Bustling Mid-Autumn Festival at the Museum of Ethnology](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/10/4/da8d5927734d4ca58e3eced14bc435a3)

![[VIDEO] Summary of Petrovietnam's 50th Anniversary Ceremony](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/10/4/abe133bdb8114793a16d4fe3e5bd0f12)

![[VIDEO] GENERAL SECRETARY TO LAM AWARDS PETROVIETNAM 8 GOLDEN WORDS: "PIONEER - EXCELLENT - SUSTAINABLE - GLOBAL"](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/7/23/c2fdb48863e846cfa9fb8e6ea9cf44e7)

Comment (0)