Under Chairman Dao Manh Khang, the bad debt ratio of An Binh Commercial Joint Stock Bank (ABBank, Hose: ABB) according to Circular 11/2021/TT-NHNN has been quietly climbing year by year. In addition, group 5 debt, the group with the possibility of losing capital, has just peaked at VND 2,278 billion, raising more questions about the real credit situation at this bank.

ABB's bad debt ratio has skyrocketed for 5 consecutive years under Chairman Dao Manh Khang

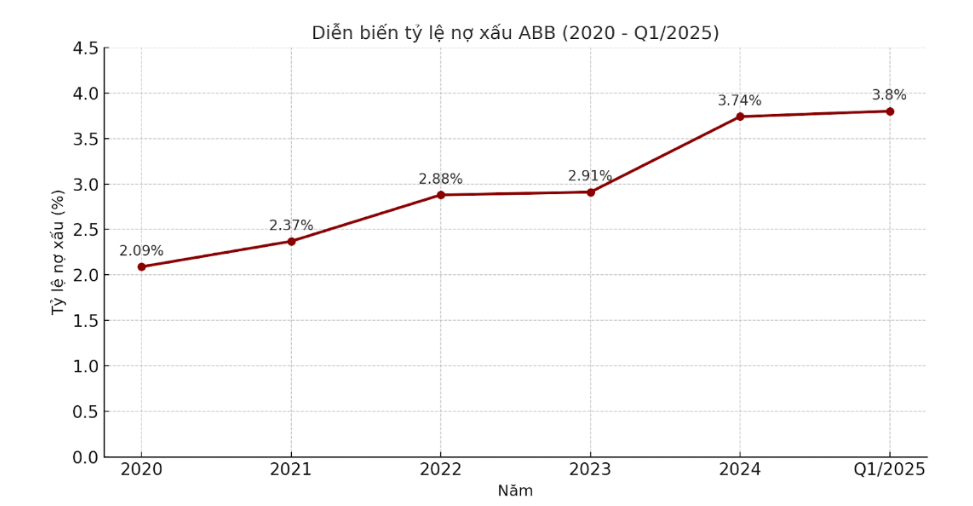

Since Mr. Dao Manh Khang took over as Chairman of ABBank's Board of Directors in April 2018, the bank's bad debt situation has begun to show signs of escalation. Based on data calculated according to Circular 11/2021/TT-NHNN - that is, taking the total outstanding debt of groups 3, 4, 5 divided by the total outstanding loan balance to customers, ABB's bad debt ratio has increased steadily over the years.

Specifically, in 2020, this rate was at 2.09%, increasing to 2.37% in 2021, then continuing to 2.88% in 2022 and 2.91% in 2023.

Notably, by 2024, the bad debt ratio had jumped to 3.74%, exceeding the 3% control threshold that the State Bank often recommends. In the first quarter of 2025, this figure continued to increase to 3.80%, reaching its highest peak in at least a decade.

This increase comes not only from the overall ratio but also reflects the bad debt structure when group 5 debt - the debt group with the highest risk of losing capital - is increasingly expanding. From more than 621 billion VND in 2020, this debt group increased to 864 billion VND in 2021, 1,404 billion VND in 2022 and continued to reach 2,107 billion VND by the end of 2024.

By the first quarter of 2025, group 5 debt had jumped to VND2,278 billion, accounting for a large proportion of ABBank's total bad debt, reflecting the increasingly fragile ability to recover capital.

Big question mark about bad debt situation at ABBank?

In its annual reports and documents sent to shareholders, ABBank under Mr. Dao Manh Khang always announced a low bad debt ratio. According to the official figures announced by ABB, the bad debt ratio in 2020 was only 1.44%, in 2021 it was 1.45%, in 2022 it was 2.19%, in 2023 it was 2.17% and by 2024 it would only stop at 2.48%.

These ratios appear to be rosy, in significant contrast to the actual NPL ratio according to Circular 11/2021 of the State Bank (when calculated based on total outstanding customer loans) ranging from 2.09% in 2020 to 3.74% in 2024, and up to 3.80% in early 2025.

Notably, at the recent shareholders' meeting, Mr. Khang continuously set the goal of controlling bad debt below 3%, even striving to bring it down to 2% in 2025.

However, with the bad debt ratio exceeding 3% since the first quarter, the question inevitably arises: how "ambiguous" is the current bad debt situation at ABBank, and do the published figures fully reflect the bank's actual credit risk?

Putting aside the debate about the bad debt ratio, it must be emphasized that ABBank has just set a new peak in group 5 debt - debt with the potential to lose capital, reaching VND 2,278 billion after only the first quarter of 2025. This is truly a worrying signal for the financial health of this bank in the coming reporting periods.

Source: https://baolamdong.vn/no-nhom-5-lap-dinh-2-200-ty-thuc-trang-no-xau-tai-abb-dang-ra-sao-381730.html

![[Photo] National Assembly Chairman attends the seminar "Building and operating an international financial center and recommendations for Vietnam"](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/7/28/76393436936e457db31ec84433289f72)

Comment (0)