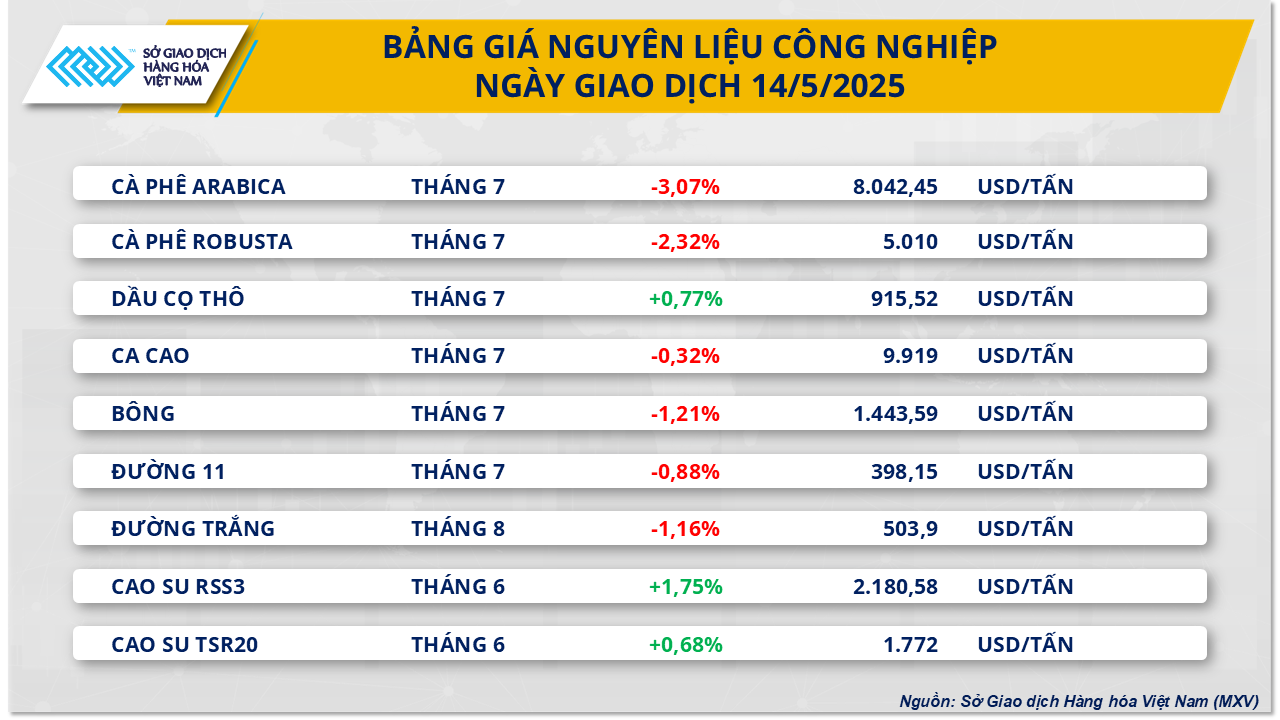

Regarding the industrial raw material group, according to MXV, red dominated the industrial raw material market in yesterday's trading session. In particular, the price of Arabica coffee for July contract on the ICE US exchange decreased by 3.07% to 8,042 USD/ton; the price of Robusta coffee for the same term on the ICE EU exchange decreased by 2.32% to 5,010 USD/ton.

The decline was largely driven by a series of forecasts for rising global supplies, with Conab raising its forecast for Brazil’s 2025-26 coffee production to 55.7 million bags, up 2.7% from the previous year – a record high for a year in the low-production cycle. At the same time, the US Department of Agriculture (USDA) also forecast a 2.6% increase in coffee exports from Honduras and Uganda, while El Salvador recorded a slight increase, prompting the market to reconsider its supply outlook in the coming period.

In addition, coffee inventories continued to increase sharply, becoming a direct factor putting pressure on prices. According to ICE, Robusta inventories reached 4,626 lots - the highest level in 7.5 months, Arabica inventories reached 844,473 bags (60kg), the highest level in nearly 3 months. Of which, 91.4% of Arabica is stored in Europe, mostly Brazilian coffee, and the amount of coffee awaiting classification also continued to increase, reflecting abundant supply in the market.

On the weather front, the World Weather Service said Brazil’s coffee-growing regions are experiencing warm weather with limited rainfall, a trend that is expected to continue into next week. While not completely dry, the scattered rains are considered too brief and light to offset evaporation, while conditions in Colombia and Venezuela remain favorable thanks to steady rains. Brazil’s arabica harvest has just begun, and despite being a low season in the biennial cycle, the outlook is more positive than at the start of the year.

Another notable development in the industrial raw material market was that the July cotton futures contract lost its upward momentum after the surge at the beginning of the week on Monday, when news of the suspension of retaliatory tariffs between the US and China for 90 days. Accordingly, the July cotton contract on the ICE US exchange continued to fall by another 1.21%, to $1,443/ton.

USDA’s latest Supply-Demand Report released Monday shows the U.S. cotton stocks-to-use ratio in 2025-26 at 36.6%, down slightly from 37.5% last season but still significantly above the five-year average of 28.0%, reflecting ample cotton supplies. Brazil’s cotton production is forecast at 18.25 million bales, up from 17 million bales in 2024-25.

In the United States, cotton planting is behind average, especially in the Delta region, due to persistent heavy rains. Texas is expected to remain dry for much of the next two weeks, allowing planting to pick up as the soil dries out, according to the World Weather Service. In West Texas, recent rains have improved planting conditions, but dry farming areas in the southwest still need more water.

In the Delta, soil conditions remain moist and planting may be disrupted by fresh rains over the next 10 days. In Xinjiang, China, the region will benefit from additional rains to support crops. Meanwhile, in northern India and Pakistan, early cotton planting is progressing smoothly as recent rains have cooled temperatures and improved field conditions.

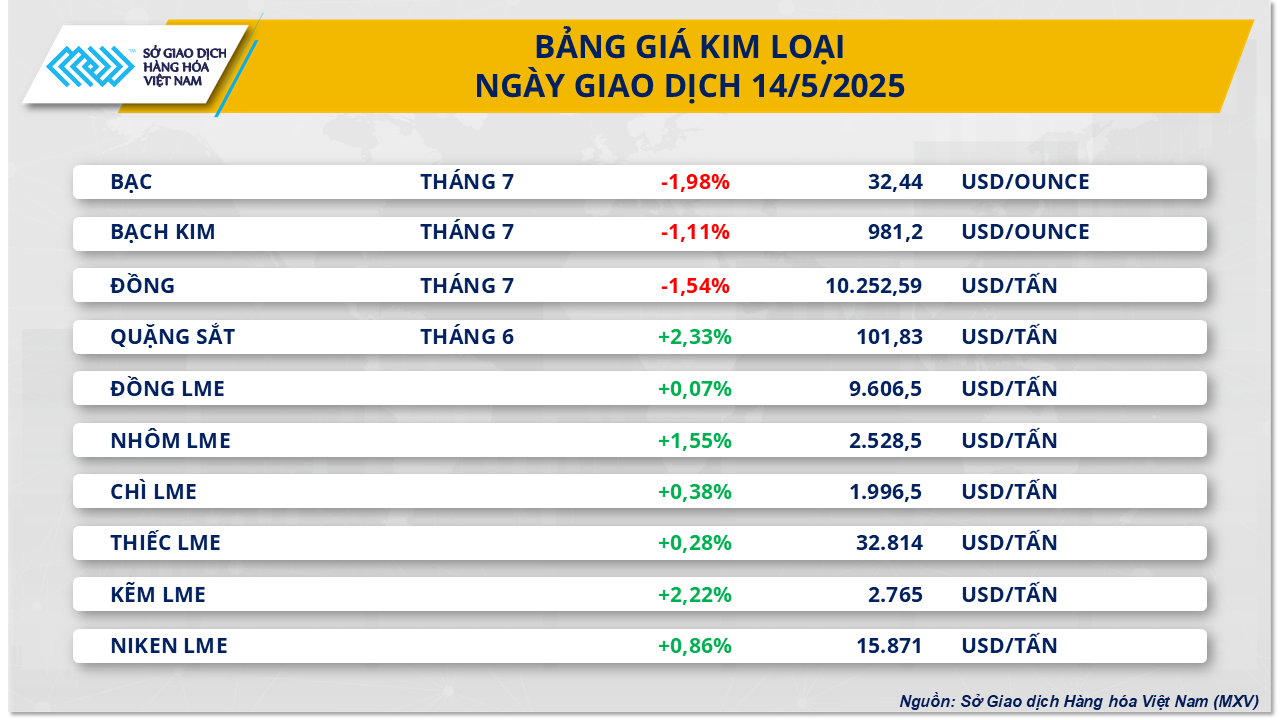

In the metal market, yesterday's trading session recorded a clear differentiation in the metal market. Improved market sentiment thanks to the positive US economic outlook caused a decline in demand for shelter, causing the prices of both precious metals to close in the red. On the contrary, the base metal group was under pressure when concerns about supply began to appear, affecting price movements during the session.

At the end of the session, silver price fell 1.98% to 32.44 USD/ounce, platinum price lost 1.11% to 981.2 USD/ounce.

Following the US-China tariff truce, a number of major investment banks have revised down their forecasts for the US recession. Goldman Sachs lowered the probability of a US recession from 45% to 35% and raised its 2025 GDP growth forecast by 0.5 percentage points to 1%. JP Morgan assessed the risk of a recession to below 50% and raised its growth forecast for China to 4.8%. Barclays even removed the risk of a recession from its forecast scenario altogether. This cooled the sentiment towards safe-haven assets and shifted money to other assets, thereby weakening the price of silver.

In the base metals group, COMEX copper prices fell sharply by 1.54% to $10,252/ton amid cautious market sentiment. In addition, positive supply signals also contributed to the decline in copper prices. The Cobre Panama mine is likely to restart after more than 18 months of shutdown for maintenance. The President of Panama recently said that the government is considering cooperation options to bring this large-scale mine back into operation. Cobre Panamá is the largest open-pit copper mine in Central America and was to produce more than 330,000 tons of copper in 2023.

Source: https://baodaknong.vn/thi-truong-hang-hoa-15-5-luc-ban-da-quay-tro-lai-chiem-uu-the-tren-thi-truong-252601.html

![[Photo] Prime Minister Pham Minh Chinh and Prime Minister of the Kingdom of Thailand Paetongtarn Shinawatra attend the Vietnam-Thailand Business Forum 2025](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/16/1cdfce54d25c48a68ae6fb9204f2171a)

![[Photo] President Luong Cuong receives Prime Minister of the Kingdom of Thailand Paetongtarn Shinawatra](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/16/52c73b27198a4e12bd6a903d1c218846)

Comment (0)