Banks and the "color change" of gold after Decree 24

After Decree 24/2012 of the Government on management of gold trading activities was issued, the picture of gold trading in the banking system has changed fundamentally, almost "changing color" compared to the previous period.

If in the past gold was a popular channel for mobilization and lending, even somewhat "free" in the banking system, since Decree 24 took effect, this activity has been strongly tightened, creating a major turning point in terms of management and business thinking of banks.

Before the issuance of Decree 24, many commercial banks were deeply involved in the gold market with a variety of products, from mobilizing capital in gold, lending gold to opening gold accounts, and trading gold accounts domestically and internationally.

This excitement entails a series of risks for the financial and banking system: fluctuations in gold prices cause large differences, differences between the demand for converting gold to Vietnamese currency, risk of loss of liquidity, legal risks and even potential manipulation, speculation and fraud in the gold market.

When Decree 24 was issued, the State monopolized the import and export of gold, allowing only a few qualified credit institutions and enterprises to trade in gold bars. Banks were no longer allowed to mobilize and lend in gold, and had to stop activities related to gold accounts or gold derivatives.

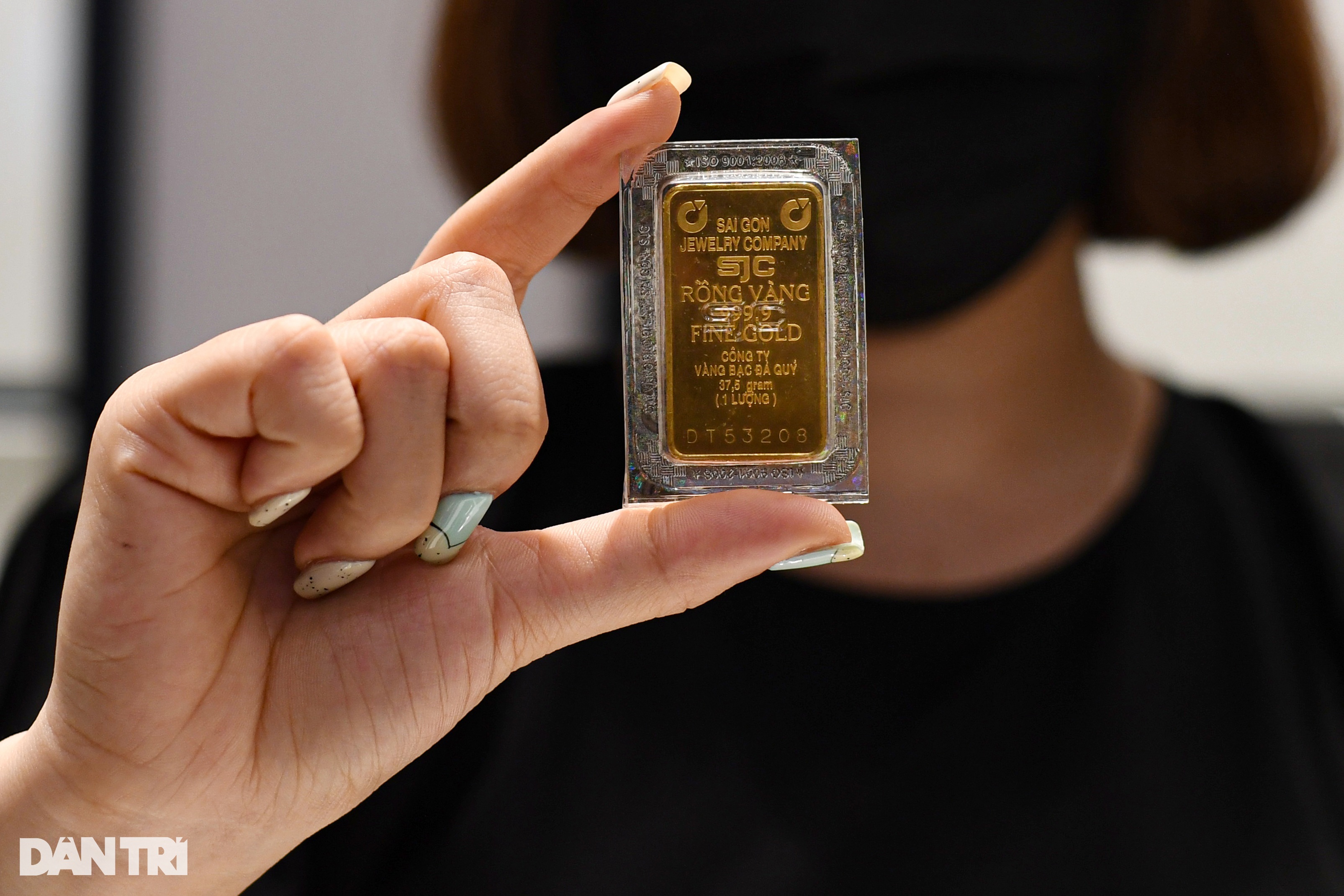

Decree 24 establishes a strict legal corridor for the gold market (Photo: Manh Quan).

This change forced banks to shift their focus to traditional services such as gold custody or payment services, instead of engaging in high-risk gold trading activities as before.

More importantly, the above decree has established a strict legal corridor, tightened the right to trade gold in the banking system, gradually sanitized the gold market, significantly reduced speculation, manipulation and turned gold into an uncontrolled investment channel. This also helps limit the “goldenization” of the economy , protect the value of the domestic currency, and increase transparency and safety for both banks and people.

Since the decree took effect, commercial banks have had to adjust their entire gold-related management processes, strengthen risk control, comply with the law, and shift to less risky products and services. If gold used to be an attractive but risky “pie”, after Decree 24, the Vietnamese banking system has been forced to enter a new orbit - much more cautious, transparent, and safer in gold management and trading.

What makes banks no longer interested in gold?

Currently, gold trading activities of commercial banks in Vietnam take place within a very strict legal framework and are limited to certain operations. After Decree 24/2012, most banks have withdrawn from high-risk activities, only maintaining some forms of gold trading in the following main forms:

The first is the gold custody service for customers. This is the most traditional and safest service when the bank only acts as a place to store assets, ensuring security and convenience for customers without participating in gold trading, speculation or lending. This service is still maintained at some large banks with reputation, wide network and strong brand in asset safety.

The second is trading gold bars according to regulations. Some qualified banks licensed by the State Bank still buy and sell SJC gold bars, mainly as agents or distributors. However, this activity takes place on a small scale, often concentrated in large cities, and is subject to very strict control over origin, quantity, and transaction process.

Third is the service of payment and gold transfer for customers. Some banks take advantage of their transaction network to provide intermediary services for gold transfer between individuals and organizations upon legal request, but only act as intermediaries and do not directly trade on their own accounts.

Fourth is providing information and advice related to gold. Some banks play a role in providing reference information on gold prices and advising customers on related products and services, but do not directly participate in buying, selling, and investing in gold as before.

Although there are many commercial banks licensed to trade in gold bars, in reality, not all banks really focus on developing this area. There are several reasons to explain this situation:

First of all, the profit margin from gold trading activities is no longer as attractive as before Decree 24. The State's strict control over gold supply, the designation of the SJC brand as the national gold bar, and strict regulations on transactions and management have narrowed the business space and reduced the opportunity to make big profits from price differences.

Second, the potential risks from gold price fluctuations and strict regulations on handling violations make many banks hesitant and unwilling to "engage" in a sensitive field that is difficult to control risks such as gold. In the context of great competitive pressure from traditional business segments such as credit, capital mobilization, and digital banking services, many banks prioritize resources for segments that generate more sustainable and stable profits.

The risk of price fluctuations is one of the reasons why banks are more "cautious" with gold (Photo: Son Tung).

In addition, to maintain gold bar trading in accordance with regulations, banks must invest heavily in treasury security, monitoring technology, training specialized personnel, as well as meeting regular inspection and reporting requirements from the State Bank. Meanwhile, the demand for gold bar trading from individual customers is increasingly dispersed to traditional gold shops or non-bank organizations, making banks' competitive advantage in this field not really prominent.

Therefore, in reality, major banks currently mainly maintain gold trading as an additional service, meeting the needs of safekeeping and buying and selling gold bars at a moderate level to serve traditional customers, rather than taking it as a business spearhead. The gold market in banks is no longer as "hot" as in the previous period, but has shifted to a stable, tightly controlled state, contributing to ensuring the safety of the financial system and complying with the State's macro-management orientation.

Removing monopoly, paving the way for national gold exchange

If we approach the problem from the direction of amending Decree 24, eliminating the monopoly on gold trading, and at the same time developing a national gold exchange, we can envision a completely new gold management strategy for Vietnam - both modern, internationally integrated, and maximizing the people's gold resources for socio-economic development.

In fact, the model of monopoly gold management over the past decade has contributed to stabilizing the financial system, but at the same time it has also left many consequences, notably the gap between domestic and world gold prices has always been stretched to an unusually high level, sometimes even tens of millions of VND per tael.

This monopoly makes the gold market uncompetitive, transaction costs are pushed up, and the rights of people and businesses are not fully guaranteed. Furthermore, a large amount of gold in people's safes is still "dead" and has not been mobilized into the economy, causing a huge waste of resources.

Therefore, amending Decree 24 in the direction of removing the monopoly on gold trading, allowing many qualified financial institutions to participate in gold bar and gold account trading activities, will create a more transparent, healthy and competitive playing field.

When more commercial banks and large enterprises join the market, competition will help reduce the difference between buying and selling prices, increase people's access to legal gold, and promote gold trading activities to take place publicly through the official system, contributing to reducing risks and "black market" activities.

At the same time, developing a modern national gold exchange, operating according to international standards, transparent in transactions, listed prices and controlling capital flows, is a fundamental solution to narrow the gap between domestic and international gold prices. The national gold exchange will play a central role connecting banks, businesses and individuals with each other and with the international market, both increasing gold liquidity and making the entire transaction flow transparent.

Thanks to that, gold price “fever”, speculative activities, price manipulation… will hardly have a chance to break out like before. This system will also support effective management of gold capital, helping authorities control the flow of gold in the economy.

In particular, if gold-based financial products - such as gold credits, gold certificates, or gold savings products with interest - are allowed to be issued, this will be a breakthrough step in mobilizing idle gold from the people into the banking system, contributing to expanding capital sources for socio-economic development.

The early establishment of a gold exchange contributed to eliminating the "bleeding" of gold from the official system (Photo: Hai Long).

When people can deposit gold in banks, receive interest or trade gold through accounts, or even use gold as collateral for loans, gold will no longer be a “dead” asset, but will become a dynamic and effective capital channel. The gold market will then no longer simply be a place to trade physical goods, but will operate according to a modern financial mechanism, which is both safe and promotes economic growth.

It can be said that amending Decree 24 with an open mind, developing a national gold exchange and gold-based financial products is an inevitable step if Vietnam wants to build a transparent, integrated gold market and truly contribute to the country's economic development.

More importantly, this will contribute to eliminating the "bleeding" of gold from the official system, gradually narrowing the price gap with the world, ensuring the common interests of the State, businesses and people.

Learn from India and China to "awaken" gold in the people

When considering international lessons on gold market management, we can look at countries with similar characteristics to Vietnam such as India and China. People in both countries have a long tradition of gold hoarding. The gold markets in both countries are strong, gold plays a role as a reserve asset for the people, and at the same time, they have faced the situation of domestic and international price differences, gold smuggling, goldization of the economy, and pressure to mobilize gold resources for economic development.

The case of India is a typical lesson. India used to apply very strict control policies on gold imports, impose high taxes, and even at one time monopolized the gold business belonging to state-owned enterprises. As a result, the "black market" gold market developed strongly, the source of smuggled gold increased, and the gap between domestic and international prices widened.

Faced with this situation, the Indian Government has shifted direction, gradually liberalizing and modernizing the gold market: opening up for commercial banks and non-bank financial institutions to participate in gold import and trading, building a centralized and transparent gold trading system, and issuing gold-based financial products (Gold Monetization Scheme, Sovereign Gold Bond...).

In particular, the program of mobilizing gold from the people in the form of depositing gold for interest, converting physical gold into credits or gold bonds receiving interest, has helped absorb the amount of "dead" gold from the people into the financial system, reduce gold smuggling, narrow the price gap, and at the same time supplement resources for the economy.

China also had a period of managing the gold market according to the State monopoly model, but since 2002, the country has boldly opened up, establishing the Shanghai Gold Exchange (SGE) as a centralized gold trading center, connecting the domestic market with the international market.

SGE allows commercial banks, businesses, organizations and individuals to trade gold in a transparent and public manner, gold prices are closely linked to world prices, minimizing speculation and price manipulation. At the same time, China also develops financial products based on gold such as gold savings accounts, futures contracts, gold credits, etc., thereby promoting gold mobilization among the people, serving production development and stabilizing the macro economy.

Developing financial products also helps promote gold mobilization among people (Photo: Hai Long).

Lessons learned from India and China show that a transparent, competitive gold market with broad participation from major financial institutions and managed through a centralized exchange is the key to solving the inherent problems that Vietnam is facing: price differences, underground markets, goldification of the economy, and waste of gold resources among the people.

Equally important, effective gold mobilization policies need to be accompanied by mechanisms to protect the rights of gold depositors, provide transparent information and diversify financial products, so that gold can truly become a safe and modern capital channel serving the country's development.

If Vietnam boldly learns and applies this experience into practice, while ensuring risk control and financial system safety, the Vietnamese gold market can completely transform itself, contributing positively to economic growth, minimizing instability and maximizing the potential of gold resources among the people.

Source: https://dantri.com.vn/kinh-doanh/vang-het-la-mo-kim-cuong-cua-ngan-hang-hien-ke-danh-thuc-vang-trong-dan-20250606030010989.htm

![[Photo] Binh Khanh Bridge Ho Chi Minh City is ready to reach the finish line](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/8/14/b0dcfb8ba9374bd9bc29f26e6814cee2)

![[Photo] Prime Minister Pham Minh Chinh talks on the phone with Cambodian Prime Minister Hun Manet](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/8/15/72d3838db8154bafabdadc0a5165677f)

![[Photo] Prime Minister Pham Minh Chinh attends a special art program called "Hanoi - From the historic autumn of 1945"](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/8/15/c1c42655275c40d1be461fee0fd132f3)

![[Photo] Firmly marching under the military flag: Ready for the big festival](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/8/15/86df2fb3199343e0b16b178d53f841ec)

![[Photo] The special solidarity relationship between Vietnam and Cuba](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/8/15/5f06c789ab1647c384ccb78b222ad18e)

![[Photo] President Luong Cuong receives Finnish Ambassador to Vietnam Keijo Norvanto](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/8/15/9787f940853c45d39e9d26b6d6827710)

Comment (0)