BVBank aims to control the bad debt ratio below 3% in 2025. However, by mid-year, this ratio had exceeded 3.83%, the highest in the past 4 years. Meanwhile, group 5 debt - debt with the possibility of losing capital increased sharply by 20.3%, accounting for 2.18% of total outstanding debt and more than 56% of total bad debt.

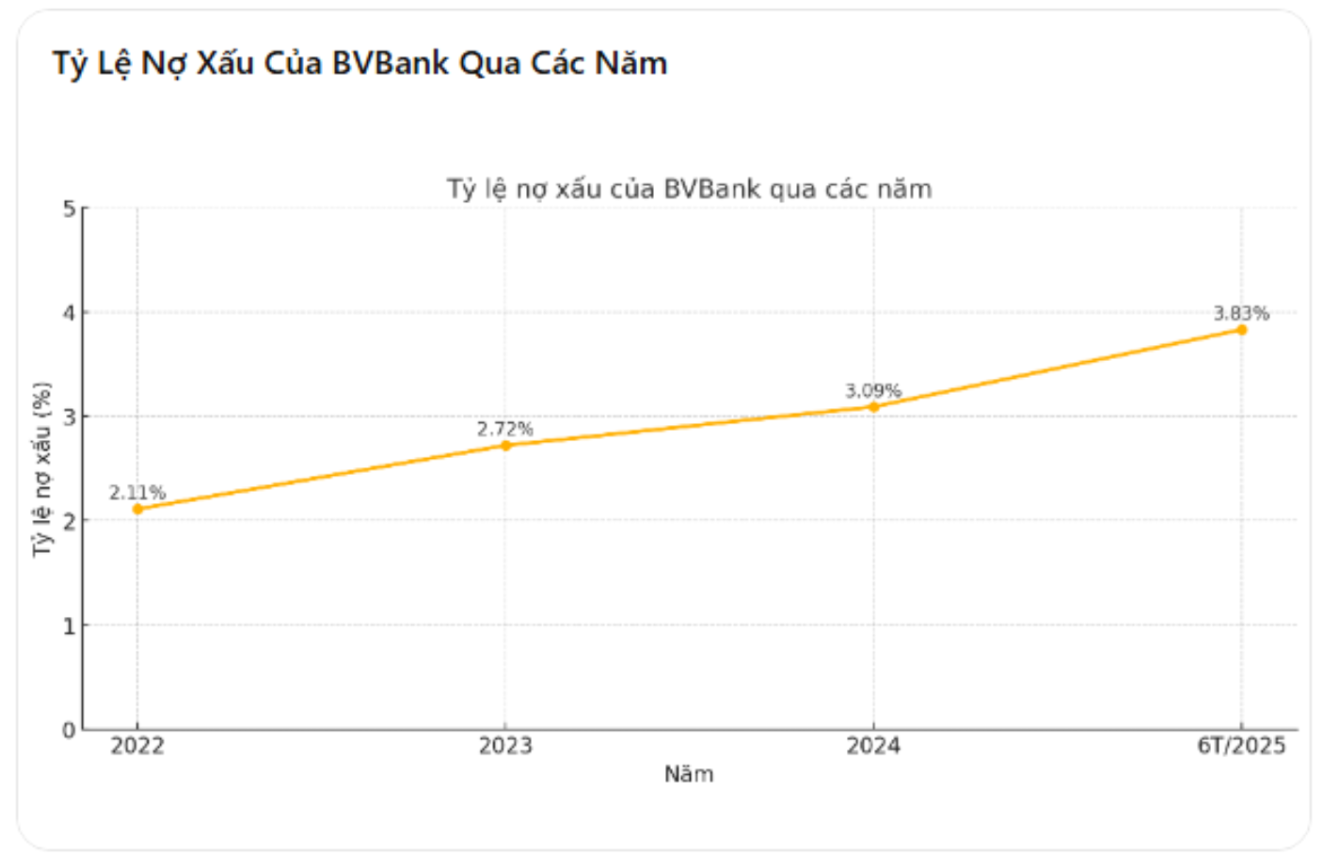

Bad debt ratio increased from 3.09% to 3.83%, the highest in 4 years

According to the consolidated interim financial report, BVBank's total outstanding customer loans as of June 30, 2025 reached VND 72,601 billion, an increase of 6.5% compared to the end of 2024. However, the total value of bad debt (groups 3, 4 and 5) skyrocketed from VND 2,103 billion to VND 2,783 billion, equivalent to an increase of 32.3%. The bad debt ratio accordingly increased from 3.09% to 3.83%.

At the 2025 Annual General Meeting of Shareholders, BVBank's Board of Directors announced that it would control bad debt below 3% to ensure credit safety and maintain a healthy index in the system. However, after only 6 months, the actual figure has far exceeded the control threshold, reflecting the increasing risk pressure in lending activities.

Notably, this is the fourth consecutive year that BVBank's bad debt ratio has increased: from 2.11% in 2022 to 2.72% in 2023, continuing to 3.09% in 2024 and currently reaching 3.83%. The steady increase over the years shows that the trend of credit deterioration is no longer temporary but has become deeply ingrained in the bank's operational structure.

Group 5 debt increased by more than 20%, second quarter profit decreased to 10.3 billion VND

Of the VND2,783 billion of bad debt at the end of the second quarter of 2025, group 5 debt - that is, debt with the potential for capital loss - accounted for VND1,579.8 billion, an increase of 20.3% compared to VND1,313.5 billion at the end of 2024. This figure is equivalent to 2.18% of total outstanding loans and accounts for more than 56% of the bank's total bad debt. The rapid increase in the highest-risk debt group shows that many loans are no longer recoverable, forcing banks to make full provisions, thereby directly affecting profits.

Along with the increase in bad debt, BVBank's business results also clearly showed a decline. In the second quarter of 2025, profit after tax reached only VND 10.3 billion, a sharp decrease of 84.4% compared to the same period in 2024. Accumulated for 6 months, profit after tax reached VND 74.4 billion, a decrease of 38.7% compared to the same period of VND 121.5 billion. This is the deepest decline in the past 4 years and clearly reflects the negative impact of provisioning costs and operating costs on the bank's financial performance.

BVBank's credit structure is also focusing on high-risk segments. By the end of the second quarter, outstanding loans to individual customers reached VND47,440 billion, accounting for about 65.4% of total outstanding loans. Outstanding loans to joint stock companies increased sharply from VND10,705 billion to VND14,633 billion, equivalent to an increase of 36.7% in just 6 months. In addition, the bank is focusing credit on high-risk sectors such as wholesale and retail (accounting for 39% of total outstanding loans), real estate (18%) and personal consumption (12.5%).

Although bank leaders have affirmed that they will promote digital transformation, improve risk management and restructure loan portfolios to keep bad debt under control, reality shows that these measures have not brought about clear results in the first half of 2025.

Source: https://baolamdong.vn/duoi-thoi-chu-tich-le-anh-tai-ty-le-no-xau-cua-bvbank-vuot-3-8-no-xau-nhom-5-tang-vot-20-3-386550.html

![[Photo] Discover the "wonder" under the sea of Gia Lai](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/8/6/befd4a58bb1245419e86ebe353525f97)

![[Photo] Nghe An: Provincial Road 543D seriously eroded due to floods](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/8/5/5759d3837c26428799f6d929fa274493)

Comment (0)