Be careful with profit taking rhythm

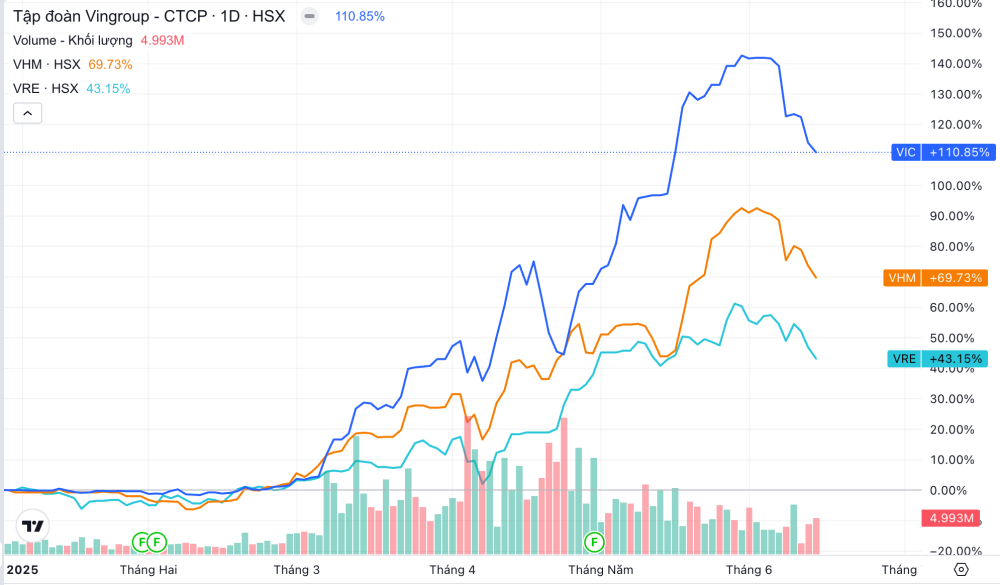

Trading performance in the first 5 months of the year was significantly affected by the election of US President Donald Trump, when the market continuously fluctuated due to decrees and statements affecting allies, trade partners as well as economic rivals of the US. In particular, the Vietnamese market quickly established a new base in April and accelerated in May, bringing the VN-Index to close at 1,332.6 points (+8.67% compared to the previous month and +5.2% compared to the beginning of the year), after recording a sharp decline earlier due to the tariff shock.

However, the recovery momentum among industry groups is quite divergent, even within stocks in the same industry. Notably, if we exclude the sudden increase of Vingroup stocks, the total capitalization value of VN-Index actually increased by only 2% compared to the beginning of the year, compared to the current increase of 9.49% (including the additional capitalization from newly listed stocks on HOSE).

This raises short-term concerns about profit-taking by individual investors to realize profits, after the impressive surge of about 100% in just two months of Vingroup stocks (VIC, VHM, VRE). This could push the above stocks into a re-accumulation state to establish higher price equilibrium zones, before continuing the medium- and long-term uptrend.

|

| Vingroup stocks have increased dramatically in recent times. |

According to Mirae Asset Securities Company's expert assessment, from a general perspective, the lack of adequate growth drivers in the short term is considered a relatively present risk for the general market, especially when groups of stocks with significant capitalization such as Banking, Technology, Retail, Securities and Steel have not yet fully recovered to the price range at the end of the first quarter of 2025, except for a few banking stocks with their own unique stories.

Expectations of cash flow spillover

Entering the second half of 2025, Mirae Asset expects the Vietnamese stock market to continue its growth momentum, with the Real Estate group expected to lead the short-term increase when supported by changes in the legal framework and a gradually stabilizing market context.

However, the medium- to long-term uptrend will require a spillover of cash flows from large-cap and leading sectors such as Banking, Technology, and Retail. This outlook is shaped by a combination of strong domestic growth drivers and significant uncertainties from external factors, especially the outlook for the outcome of trade negotiations with the United States.

Behind Vietnam’s economic expectations are domestic growth drivers to achieve the GDP growth target of 8% by 2025. The government has implemented a “strategic quartet” consisting of Resolutions 57, 59, 66 and 68, followed by a series of directives and implementing documents to promote the development of the private economic sector, streamline the legal framework, and create a favorable environment for businesses.

These resolutions also contribute to promoting the overall growth target, including promoting consumption activities, unblocking capital sources through credit growth targets and resolutely disbursing all capital allocated for public investment. Thereby, shaping Vietnam's commitments to economic recovery and growth with strong ambitions and aspirations in the context of global trade activities facing many challenges due to tariffs and geopolitical instability.

Real estate is expected to benefit from the above factors, in addition to changes in the legal framework, including amendments to the Law on Planning and the legalization of Resolution 42.

Specifically, Resolution 42 provides mechanisms to resolve bad debts and restructure troubled projects, increase leverage and facilitate capital sources for both real estate developers and credit institutions. Thereby, it helps improve the capital mobilization environment and facilitate access to land for new projects, while supporting banks through improving asset quality, when non-performing loans related to real estate will be handled.

In general, the overall picture of the business activities of leading enterprises currently reflects signs of stability and gradual recovery after the real estate and corporate bond crisis in the period of 2022 - 2023 with the trend of the value of new overdue bonds slowing down each month since the beginning of 2024 while the ratio of overdue principal/interest bonds to total outstanding bonds is trending sideways as of June 2025, according to statistics from VIS Ratings.

However, the recovery prospects of the real estate industry still depend on the ability to mobilize capital and land funds to increase the number of new projects while at the same time needing to be balanced with the recovery of consumer spending and investment activities in the coming time.

Despite the solid internal foundation, the outcome of trade negotiations with the United States remains a big unknown. Overall, Mirae Asset maintains a cautiously optimistic view with the short-term growth momentum being led by the Real Estate group, but the prospect of sustainable growth in the medium and long term will require the spread of cash flow to help the VN-Index conquer the 1,400 point mark.

Source: https://baodautu.vn/ky-vong-vao-dong-tien-tren-thi-truong-chung-khoan-nua-cuoi-nam-2025-d304990.html

![[Photo] Prime Minister Pham Minh Chinh chairs national online conference on new rural construction and poverty reduction](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/6/23/0d239726be21479db1ea6d8d77691a6d)

![[Photo] Prime Minister Pham Minh Chinh chairs conference to accelerate disbursement of public investment capital, deploy key projects and eliminate temporary and dilapidated houses](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/6/23/fcb205e3ca19432eac326f55123308f4)

![[Photo] Party Congress of the Central Internal Affairs Commission for the 2025-2030 term](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/6/23/5bf03821e6dd461d9ba2fd0c9a08037b)

![[Photo] Conference to disseminate the implementation of the Plan to promote digital transformation to meet the requirements of restructuring the political system's apparatus](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/6/23/4744403cccd144b79086799e2ceb686e)

Comment (0)