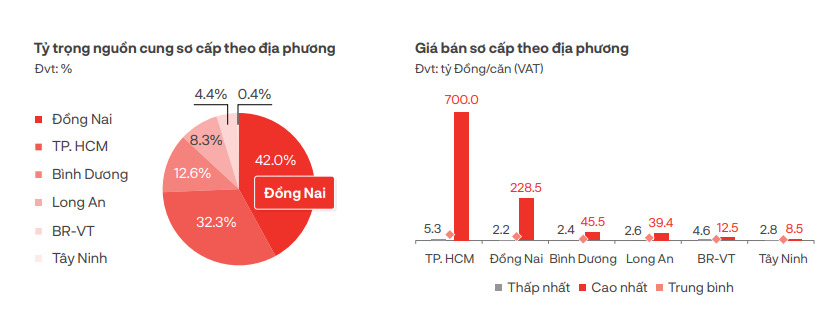

Dong Nai accounts for the majority of the supply of villas and townhouses.

The Ho Chi Minh City and surrounding area market report recently published by DKRA shows that in the third quarter of 2024, the supply and primary consumption of villas and townhouses increased by 16% and 6.8 times respectively compared to the same period last year.

Compared to the same period last year, new supply and consumption have many positive changes, reaching an increase of 4.1 times and 7.6 times respectively. Of which, Dong Nai accounts for 55% of supply and 47% of new consumption in the quarter. In addition, the overall demand of the market also recorded positive signs of increase compared to the same period last year. However, consumption remains low, with a rate of only about 11% of the total supply.

Dong Nai is accounting for a high proportion of supply, with the second highest selling price in the regional market.

The primary price level has not changed much compared to the beginning of the year, the most expensive product still belongs to the Ho Chi Minh City market at 700 billion VND/unit, down about 6.6% compared to the previous quarter. Ranked second is the Dong Nai market with the highest selling price maintained at 228.5 billion VND/unit. Discount policies, opening day incentives, bank support, etc. are widely applied to increase liquidity.

The secondary market price of this type also increased by about 4% compared to the previous quarter, market transactions improved compared to the same period last year, however, there are unlikely to be any sudden changes in liquidity in the short term.

Consumption of villas and townhouses in the last quarter showed positive signs of this type in the year-end period.

Forecasting the market in the fourth quarter of 2024, DKRA believes that new supply will continue to increase slightly compared to the previous quarter, reaching about 550 - 650 units, mainly concentrated in familiar localities such as Ho Chi Minh City, Binh Duong , Dong Nai, Long An, ...

Market liquidity in the next quarter will improve compared to the same period in 2023, with transactions mainly distributed in projects that ensure construction progress and legal safety. Meanwhile, the primary price level may increase slightly compared to the beginning of the year due to the impact of input costs. In the secondary market, prices will continue to increase following the trend of the previous quarter, with projects that have handed over houses, diverse utilities, convenient regional connections, etc. being the main drivers of market liquidity.

With forecasts of positive economic growth, a complete legal system, low real estate loan interest rates, etc., these are factors expected to create a foundation for market recovery in the coming time.

Land prices continue to stay high and remain stable compared to the beginning of the year.

Regarding land, primary supply recorded in the third quarter of 2024 increased by about 11% compared to the same period last year. However, new supply remained scarce, accounting for only about 3% of the total primary supply and increasing slightly by 2%.

Binh Duong province leads the new market with supply and consumption reaching 52% and 78% respectively. Market liquidity recorded positive signals, consumption was 2.8 times higher than the same period last year, but still remained at a low level compared to the period from 2019 and earlier.

Transactions are concentrated locally in the group of products with completed infrastructure and legal documents with an average price of under VND50 million/m2 in Ho Chi Minh City or under VND22 million/m2 in the surrounding areas. However, the primary price level maintains a sideways trend compared to the beginning of the year and remains high due to the impact of input costs. The secondary market recorded a slight increase of about 3% compared to the previous quarter, market liquidity recovered positively but there are unlikely to be any breakthroughs in the short term.

The land market also recorded a recovery in both supply and consumption rate.

It is forecasted that in the fourth quarter of 2024, the new supply of the market will maintain the positive recovery trend of the third quarter of 2024, but will still remain at a low level compared to the period before 2019, expected to reach about 350 - 450 products.

Neighboring localities such as Binh Duong, Long An, Dong Nai, etc. are expected to lead market liquidity in the final months of the year. Primary prices are expected to increase slightly compared to the beginning of the year due to the impact of input costs, along with stimulus policies applied by investors to increase liquidity.

The secondary market has changed positively compared to the same period, the product group in urban areas with synchronous planning, completed infrastructure, and legal status has improved a lot in terms of selling price and attracted market liquidity. 3 The Real Estate Law takes effect in early August 2024, along with the impact of economic factors and market policies, which are expected to bring positive impacts in the coming time.

Source: https://www.congluan.vn/biet-thu-nha-pho-tai-thi-truong-tp-hcm-va-tinh-lan-can-ghi-nhan-luong-tieu-thu-tang-gan-7-lan-post316656.html

Comment (0)