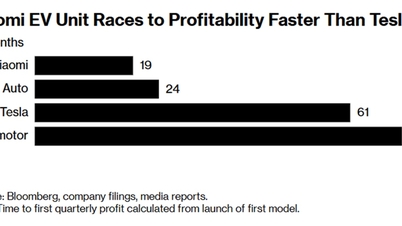

Xiaomi recorded 700 million yuan ($98 million) in profit from its electric vehicle and artificial intelligence divisions in the third quarter ended September 30, it said on November 18. The milestone came just 19 months after the launch of its SU7 electric sedan, faster than Tesla, Li Auto and Leapmotor by comparable benchmarks.

- 19 months to make a profit in the electric vehicle segment, earlier than Li Auto (24 months), Tesla (61 months) and Leapmotor (71 months).

- Integrated ecosystem strategy, strong brand and existing user base help keep customer acquisition costs low.

- YU7 expands product range; over 289,000 orders in just a few hours.

- Risks: tax incentives narrow from next year, October sales fall, cashback up to 15,000 yuan narrows profit margin; 2026 gross margin expected to decline.

- Plans to sell cars in Europe from 2027; domestic competitive pressure increases.

Cars with an electronic mindset: create demand first, optimize break-even point

According to Bill Russo (Automobility, Shanghai), Xiaomi entered the market with a structural advantage that most EV startups lack: a huge user base, a trusted brand, and an integrated ecosystem. Its software-centric approach helps expand revenue beyond the car. The company implemented a strategy of treating the SU7 as a “consumer electronics product” launched at scale – prioritizing demand generation, designing for quick break-even.

Xiaomi started with one model, a tightly managed supply chain, and a software-centric architecture. This shortened the time to profitability compared to many competitors, who had to burn through multiple product lines before reaching a large enough sales scale.

Time to Profit: Xiaomi Beats the Market

| Company | Quarterly profit milestone | Note |

|---|---|---|

| Xiaomi | 19 months | After the launch of SU7 |

| Li Auto | 24 months | Mainly selling EREV cars |

| Tesla | 61 months | Roadster distribution since 2008; first quarter profit 2013 |

| Leapmotor | 71 months | According to the comparison benchmark stated |

| Xpeng, Nio | Not yet profitable | Target break-even by 2025, about 8 years after launch |

Scale thanks to a maturing electric vehicle supply chain

According to Bill Russo, China’s mature EV supply chain allows startups to scale without large capital investments, unlike early adopters who had to build much of their own supply chain. With a software-centric architecture, Xiaomi has room to exploit the ecosystem to increase usage value and revenue over the lifecycle.

YU7 portfolio expansion: initial market signal

In June, Xiaomi launched its second model – the YU7. The company said it received over 289,000 pre-orders within hours. The move showed immediate demand for the brand and its ability to leverage its existing user base to move into the automotive segment.

Pressures ahead: tax incentives, profit margins and demand

Tax breaks for electric and hybrid vehicles in China will be scaled back next year; it’s unclear whether trade-in subsidies will be extended. Sales of electric vehicles fell in October compared to a year earlier. To offset the tax incentives, Xiaomi is offering cashbacks of up to 15,000 yuan for customers who order before the end of November and receive their cars in 2026, but this will cut into profit margins.

During an earnings call on November 18, Chairman Lu Weibing warned that EV gross margins are expected to decline by 2026. Domestic competition will intensify as demand growth slows, highlighting a challenging outlook for the industry, according to analysts Joanna Chen and Jason Zhao of Bloomberg Intelligence. Manufacturers may increasingly rely on exports to sustain production and profit growth.

The problem of markets outside China

Xiaomi aims to start selling electric vehicles in Europe in 2027. While companies like BYD, Geely, Xpeng and Leapmotor are leading the way in exports, Xiaomi’s failure to expand overseas before 2027 casts doubt on its business outlook next year.

Conclusion: Ecosystem advantage, sustainable profit challenge

The rapid growth in profitability suggests that Xiaomi’s ecosystem-integrated, software-centric, user-centric model is working in its early stages. However, changing incentives, slowing domestic demand, and gross margin pressure are significant tests in the expansion phase, especially with overseas expansion plans only starting in 2027. With an expanding portfolio and domestic supply chain advantages, there is still room for growth, but cost discipline and pricing strategy will determine the sustainability of profits.

Source: https://baonghean.vn/xiaomi-su7yu7-loi-nhuan-som-nho-he-sinh-thai-tich-hop-10311920.html

![[Photo] The Standing Committee of the Organizing Subcommittee serving the 14th National Party Congress meets on information and propaganda work for the Congress.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/19/1763531906775_tieu-ban-phuc-vu-dh-19-11-9302-614-jpg.webp)

![[Photo] Prime Minister Pham Minh Chinh and his wife meet the Vietnamese community in Algeria](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/19/1763510299099_1763510015166-jpg.webp)

![[Photo] General Secretary To Lam receives Slovakian Deputy Prime Minister and Minister of Defense Robert Kalinak](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/18/1763467091441_a1-bnd-8261-6981-jpg.webp)

Comment (0)